Milk tea isn’t just a drink. It is a social signal. Samgyupsal isn’t just a meal — it has become a weekend ritual.

Few food trends have achieved what these did: mass appeal across socioeconomic classes, viral traction across platforms, and real estate-level impact in malls and high streets nationwide. Their success offers a blueprint for how food fads evolve into full-fledged consumer movements in the Philippines, driven by youth culture, social validation, and the pursuit of immersive, shareable experiences.

With over half the population under 30, Filipino consumers aren’t just early adopters; they’re active trendsetters. Food isn’t simply nourishment; it’s identity, entertainment, and currency for connection. Whether it’s a TikTok-worthy bite or a heritage dish reimagined for a new generation, the choices Filipinos make at the table are deeply intertwined with how they see themselves and the world.

For F&B brands operating in this space, understanding what drives these choices means tapping into a uniquely layered market – one where Western influences blend with local pride, and novelty only sticks when it aligns with culture, context, and community.

Fusion Finds Its Filipino Soul

Restaurants across Metro Manila are rewriting the rulebook for Filipino cuisine. A new wave of chefs is blending local comfort food with global influences – turning kare-kare into curry bowls, transforming adobo into bao buns, and giving sinigang a Japanese ramen twist. These aren’t gimmicks; they’re calculated plays to tap into the Filipino craving for novelty without abandoning familiarity.

This approach appeals to a generation raised on K-pop and content algorithms. Diners want flavour, but they also want narrative – a dish that photographs well and tells a story. Fusion provides both. Sinigang is reinvented with beef short rib and watermelon at spots like Manam Comfort Filipino, offering a playful yet rooted take on the classic. Sarsa Kitchen + Bar builds on Negrense traditions but packages them with a contemporary edge, perfect for the urban millennial crowd.

F&B groups are taking notice. Mid-scale franchises are testing bolder menus inspired by these high-concept eateries, hoping to scale trend-led items before they hit saturation. With younger diners using food discovery as entertainment, fusion isn’t fringe – it’s a fast-moving commercial opportunity.

The Rise of Regional Ingredients

The mainstream Filipino menu is undergoing a quiet revolution – and it’s being led by ingredients once considered too obscure, too rural, or too slow to scale. Diners are now seeking depth: flavours that feel earned, ingredients that come with provenance, and dishes that tell regional stories.

Items like batuan, pili nuts, tabon-tabon, and taba ng talangka are moving from weekend palengke hauls to chef specials and curated tasting menus. Adlai, once a heritage grain, now appears in health-forward bowls and upscale rice alternatives. These ingredients aren’t just rich in flavour; they’re signalling exclusivity, craftsmanship, and cultural pride.

Restaurants like Toyo Eatery and Locavore have championed this movement by reintroducing ancestral ingredients to urban diners and building menus that are proudly Filipino but globally competitive. For F&B groups, this opens a path to elevating brand storytelling – whether through seasonal LTOs (limited-time offers), regionally inspired menu capsules, or direct sourcing partnerships with local farmers.

The shift isn’t about going backwards – it’s about building forward with authenticity. As Filipino consumers increasingly equate food choices with values, using regional and artisanal ingredients is a culinary and commercial advantage.

Plant-Based and Flexitarian

Meat may still dominate the Filipino plate, but the momentum behind plant-forward eating is growing – not as a fringe lifestyle but as a mainstream shift among millennials and Gen Z. This shift isn’t driven by ideology alone; it’s about wellness, affordability, and the increasing accessibility of meat alternatives in urban centres.

Traditional dishes are being reformatted for a new generation: laing without bagoong, kare-kare with jackfruit, sisig with tofu and mushrooms. Homegrown spots like Green Bar in Makati and The Wholesome Table in BGC have found success by blending comfort food aesthetics with health-forward menus. Their dishes don’t preach – they sell through flavor, familiarity, and lifestyle branding.

There’s a gap in the casual dining space for restaurant groups where plant-based menus are still treated as secondary. Introducing flexitarian lines – not full vegan menus, but deliberate plant-forward heroes – is a low-risk, high-upside way to meet the rising demand. It also signals alignment with values like sustainability, something younger consumers are rewarding with loyalty and spending.

What once felt like a niche segment is now a whitespace for innovation. And in a country where vegetables have always been part of the table, rethinking them for modern preferences is a return, not a departure.

Street Food 2.0 – Elevated and Instagrammable

Filipino street food has always been bold, flavorful, and accessible, but it’s never been this photogenic. What used to be served from pushcarts and roadside grills is now being reimagined for curated food halls, food parks, and Gen Z-focused dining places.

Think kwek-kwek with truffle aioli, isaw glazed in honey sriracha, or balut turned into a small-plate delicacy with sinamak foam. Brands like Boy Isaw and Mang Larry’s Isawan have helped normalise street food in structured retail settings, while new concepts like IhawJuan lean into design-forward booths, premium packaging, and consistent flavour control.

This trend thrives on nostalgia wrapped in novelty. It appeals to Filipino diners’ emotional connection to childhood and street culture while meeting modern expectations for hygiene, branding, and presentation. On TikTok and Instagram, street food with a twist is shareable gold.

For restaurant groups, the opportunity lies in format innovation: bite-sized, affordable, customizable items that fit both dine-in and grab-and-go formats. It’s also a chance to localise at scale, with regional street food variants offering ready-made menu expansion paths across the country.

Ancestral Filipino Cooking Techniques with A Modern Flair

Filipino chefs are reaching into the past not to replicate it but to reinterpret it. Slow, regional methods like pinaupong manok, pinais, kinilaw, tinapa, and kulawo are being reintroduced in refined forms, framed less as throwbacks and more as culinary heritage elevated for today’s palate.

At restaurants like Balay Dako in Tagaytay and Café Juanita in Pasig, long-held techniques are presented with care, often paired with storytelling that links each dish to family tradition or regional history. The appeal isn’t just authenticity – it’s depth. For consumers burned out by over-engineered food fads, these dishes offer a sense of grounding and meaning.

What was once seen as slow and provincial now feels premium. The tactile nature of these cooking methods – from banana-leaf wrapping to open-fire grilling – offers rich sensory experiences, ideal for diners seeking more than just taste.

For restaurant groups, this movement is an opportunity to differentiate themselves. Ancestral techniques lend themselves to seasonal menus, chef’s specials, and content-rich brand narratives. They also create space for regional partnerships and experiential formats, such as heritage dining nights or interactive prep counters. Tradition isn’t the opposite of innovation – it’s becoming its most compelling form in the Filipino market.

Filipino dining is not just about what’s on the plate – it’s a statement of identity, intent, and influence. As tastes evolve and boundaries blur between tradition and trend, the winning brands will move beyond imitation and lean into insight, capturing the cultural undercurrent driving the next wave of consumption.

Market research is your edge if you’re looking to tap into the next wave of Filipino food trends with confidence. From concept testing and menu optimisation to understanding shifting consumer behaviours across regions and generations, our team delivers the insights you need to make bold, informed decisions. Let’s uncover what’s next – together.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

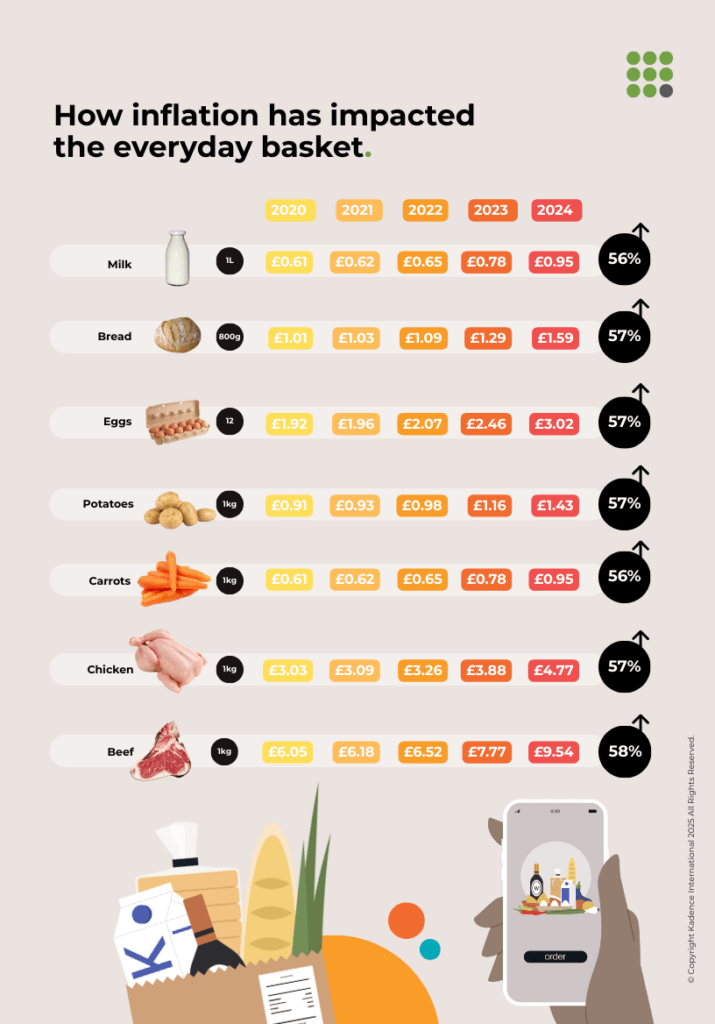

The fastest way to read the economy might be through a grocery receipt.

In the United States, a staple as simple as frozen pizza has become a financial strategy, signalling how households manage cost, comfort, and consistency.

And the US isn’t alone. Across markets, pantry staples are doubling as economic sensors. In the UK, a jump in baked bean and private-label ready meal sales mirrors cost-of-living anxiety. In Japan, instant noodles remain resilient despite price hikes, especially premium options. In China, frozen dumplings are no longer seasonal but weekday staples. Each reflects how consumers behave when their budgets are under pressure.

For brands, these patterns aren’t background noise. They’re forecasting tools. The staples consumers cling to during disruption are often early indicators of more profound shifts in sentiment and strategy.

The psychology behind food choices

When financial stress sets in, consumers don’t just look for cheaper options; they look for control. Food becomes a tool to reclaim routine, reduce effort, and preserve small pleasures. In inflationary periods, what matters isn’t just price. It’s perceived value.

Today’s shoppers are making what behavioural economists call satisfying decisions: good-enough choices that balance budget, emotion, and effort. That explains the rise of “premiumised basics.” In Japan, consumers choose upscale instant ramen precisely because inflation makes dining out less accessible, and these products offer the comfort and experience of a restaurant meal at home. A frozen pizza or store-brand ready meal isn’t just a shortcut; it’s a psychological release valve.

Aggregated across millions of carts, these choices offer powerful signals. Brands that can spot the patterns early and build for them gain an edge.

Frozen pizza and the power of low-effort indulgence

In the US, frozen pizza has moved from the edge of the freezer to the centre of the meal plan. Sales reached $7.0 billion in 2024, reflecting growing demand for foods that balance indulgence and utility.

The pandemic normalised at-home dining, and inflation extended the habit. Frozen pizza delivers more than calories: it’s familiar, flexible, and low-friction. It substitutes for takeout, satisfies a group, and feels like a treat without requiring cooking skills. Consumers aren’t just trading down; they’re trading differently.

That shift has created space for brands like Screamin’ Sicilian and California Pizza Kitchen to position frozen products as restaurant-quality. Clear packaging, upscale branding, and perceived authenticity all signal that compromise isn’t necessary.

Evaluate your portfolio by the effort-to-satisfaction ratio. Consumers gravitate toward products that offer fast prep, emotional payoff, and cost consistency. Frozen pizza’s success shows how categories that meet these criteria outperform even in volatile markets.

UK shoppers trade brands for value

Baked beans have long been a UK staple, but recent sales data tells a deeper story.

In 2023, total baked bean sales rose 2.5%, but Heinz saw a 5.1% decline. Private labels surged, with Euroshopper and others gaining share. The shift is primarily driven by price sensitivity. As grocery bills rise, shoppers increasingly trade down to store-brand or value-tier options that offer similar taste and portion sizes at significantly lower prices. Loyalty to the category remains, but brand allegiance weakens when meaningful differentiation doesn’t match premium pricing.

The same is playing out in chilled ready meals. Tesco and Sainsbury’s expanded their value lines, and consumers responded. These aren’t subpar options as packaging, taste, and positioning have all improved. The new trade-down doesn’t feel like a sacrifice.

Legacy brands need to reassess elasticity. When brand loyalty erodes under pricing pressure, winning back market share means redefining value, not just dropping price. Functional improvements and narrative clarity are now essential to justify a premium.

Japan’s affordable upgrades

According to The Guardian, the price of instant ramen increased 20% over the past two years, but consumption remained high.

In Japan, inflation hasn’t dented demand for instant noodles. Nissin raised prices, yet consumption held steady. More surprising: it’s the premium SKUs that are growing fastest.

Consumers are seeking quality within constrained budgets. The appeal isn’t just cost; it’s comfort and cultural continuity. A bowl of gourmet-style ramen at home replaces an expensive lunch out. The transaction becomes emotional as much as practical.

Affordable premiumization is a long-term play. Consumers will spend a little more if the return feels meaningful. That means elevating basics, through taste, story, or packaging, to deliver a perceived upgrade without a price shock.

China’s modernised tradition

Frozen dumplings have become a year-round staple in Chinese households. Once reserved for holidays or family occasions, they’re now an everyday solution for time-strapped urban consumers. In 2024, the market reached $6.86 billion, with younger buyers, balancing long hours and shrinking leisure time, driving much of the demand.

This isn’t convenience displacing tradition; it’s adapting to new consumption habits. Frozen dumplings retain cultural relevance while offering speed, consistency, and modern formats.

Culturally rooted convenience products can unlock mass-market growth when paired with modern positioning. The key is to evolve the format and accessibility without stripping away the story.

India and the Philippines: Time-saving staples under strain

According to Future Market Insights, the ready-to-mix food market in India reached $440 million in 2023 and is projected to grow to $1.75 billion by 2033. Snacks and mixes form a dual growth engine, as consumers manage rising costs and time poverty.

These products aren’t replacing traditional meals; they’re reshaping them. Dosa batter and spice blends offer cultural authenticity without daily prep. Convenience without compromise is becoming a national default.

In the Philippines, canned sardines serve as both sustenance and security. With inflation averaging 6.1% in 2023 and over 20 tropical storms a year, demand for shelf-stable protein spikes in response to economic and environmental stress. Mega Global, which holds a 30% market share, invested over USD 1.7 million to expand capacity by 20%, betting on continued category growth. The company’s investment in expanded capacity is a bet that pantry-stable proteins will remain a default safety net.

In emerging and climate-vulnerable markets, brands win by delivering reliability. Food products that address economic or environmental uncertainty earn long-term trust. Packaging, shelf stability, and affordability aren’t features. They’re foundations.

Micro-trends as macro signals

The grocery aisle is a real-time indicator of consumer mood. It reveals where people are willing to compromise and where they won’t. In every market, different staples are rising for the same underlying reasons: they feel safe, smart, and familiar.

Country

Food Signal

Behavior Cue

USA

Frozen Pizza

Indulgent efficiency

UK

Baked Beans, Ready Meals

Brand elasticity

Japan

Instant Noodles

Affordable premiumization

China

Frozen Dumplings

Cultural speed

India

Mixes & Snacks

Time-cost optimization

Philippines

Canned Sardines

Resilience stockpiling

That’s not just retail behaviour. It’s brand insight. When inflation hits, when trust dips, when time disappears, the categories that survive aren’t the trendiest – they’re the ones that deliver.

The lesson for brands is clear: resilience lives in the ordinary. When the economic cycle turns again, the brands that stay in the basket will stay in the conversation.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Blueprints and performance specs no longer tell the full story. With buyers and stakeholders demanding greater transparency, industrial tech firms are under increasing pressure to disclose more than just technical capabilities.

Procurement teams across sectors are asking deeper questions – about carbon emissions, labour conditions, and lifecycle impact. European disclosure mandates and US reporting proposals are accelerating the shift. Once confined to consumer brands, transparency expectations are now reaching B2B suppliers of semiconductors, robotics, and industrial machinery.

Buyers Want More Than a Product Sheet

Technical performance remains critical, but it is no longer the only factor in industrial procurement. A 2024 study by Market Expertise found that ESG-related concerns now rank among the top ten decision drivers for global B2B buyers. This highlights a broader shift in evaluation criteria.

Suppliers are increasingly required to provide data on emissions reduction, ethical sourcing, and corporate governance. In sectors such as aerospace, mining equipment, and chemical processing, procurement teams are requesting carbon audits, labour practice disclosures, and diversity metrics alongside traditional technical specifications.

Firms that do not meet these requirements may be excluded from consideration altogether.

New Rules Are Forcing the Issue

Industrial tech firms no longer disclose sustainability data out of goodwill; they’re doing it to comply. In the US and Europe, regulators are making ESG transparency a legal requirement.

In January 2024, the European Union’s Corporate Sustainability Reporting Directive (CSRD) came into effect, requiring thousands of companies – both EU-based and international firms with regional operations – to disclose detailed information on environmental impact, human rights, and governance. For the industrial tech sector, this means publishing previously considered proprietary metrics: carbon intensity, supply chain traceability, and even energy sources.

The pressure is mounting stateside as well. The US Securities and Exchange Commission (SEC) is expected to finalise rules this year mandating climate-related disclosures from publicly traded companies. This includes direct and indirect emissions data, climate risk assessments, and mitigation strategies, pushing firms in manufacturing and engineering to build new reporting infrastructures almost overnight.

The result: what was once optional is quickly becoming standard. And for firms hoping to win contracts in highly regulated markets, compliance isn’t just a checkbox; it’s a competitive edge.

Industrial Giants Begin Opening the Books

Some of the world’s largest industrial tech players are beginning to respond, not just with compliance but with proactive disclosures that mirror the transparency seen in consumer sectors.

Intel’s 2023–24 Corporate Responsibility Report goes beyond carbon emissions to include water usage, chemical management, and workforce diversity – information that was once buried in internal audits. In its 2023/24 ESG report, Lenovo disclosed targets for reducing scope 1 and 2 emissions, supply chain sustainability efforts, and metrics tied to circular economy goals. The company now ranks highest in the IT industry on the Hang Seng Corporate Sustainability Index.

NVIDIA’s 2024 sustainability report outlines how its data centres are optimised for energy efficiency, with scope 3 emissions and supplier climate programs prominently featured. These aren’t one-off updates; they’re becoming annual staples, complete with third-party verification and downloadable datasets.

For an industry known for tight-lipped operations and long procurement cycles, this shift signals more than regulatory compliance. It’s a recalibration of what trust looks like in the industrial age.

Supply Chains Are No Longer Exempt

Industrial tech firms are extending ESG scrutiny beyond their own operations. Suppliers are now under pressure to meet the same standards, sometimes higher. Contracts increasingly require disclosures not just on raw materials or manufacturing timelines but also on carbon intensity, labour conditions, and waste management practices.

Microsoft has already set the tone. In 2024, the company announced it would require key suppliers to use 100% carbon-free energy by 2030. The move came as Microsoft’s emissions rose nearly 30% year-over-year, largely due to expanded AI infrastructure and Scope 3 emissions tied to its supply base. It signals to partners: clean up or lose the business.

In Australia, chemicals and explosives company Orica has installed nitrous oxide abatement technology across multiple sites, reducing emissions by an estimated 15%, roughly equal to the annual output of all other Australian chemical producers combined. This investment wasn’t just about optics; it was about securing long-term contracts with environmentally conscious buyers.

The trend is clear: if your data isn’t clean, your bid may not even make the table.

Reporting Is Messy, Expensive, and Unfinished

For all the momentum, ESG reporting remains a logistical hurdle for many industrial tech firms. Gathering emissions data across sprawling operations, inconsistent supplier systems, and decades-old infrastructure isn’t just difficult; it’s costly and time-consuming.

A major pain point is standardisation. With dozens of frameworks in play—from the Global Reporting Initiative (GRI) to the Sustainability Accounting Standards Board (SASB)—companies struggle to align disclosures that simultaneously satisfy investors, regulators, and buyers. Even firms that publish detailed ESG reports often face scepticism over data quality.

Governments are taking note. In February 2025, the European Commission proposed a 25% reduction in reporting burdens as part of its “Simplification Omnibus,” a move estimated to save businesses across the bloc €40 billion annually. While it won’t eliminate the need for transparency, the shift suggests that complexity may be one of the biggest roadblocks to effective ESG strategy.

The challenge now is not whether to report, but how to report meaningfully, consistently, and at scale.

Transparency Is Becoming a Selling Point

In industrial tech, where margins are tight and products are often commoditised, ESG transparency is emerging as a powerful differentiator. Firms that can clearly communicate their sustainability practices are gaining ground, not just with regulators but also with clients who now see environmental and social metrics as a measure of long-term value.

According to research, B2B buyers are more likely to renew contracts and pay premium prices to suppliers who can prove sustainable practices. This shift is being felt across sectors – from advanced manufacturing to semiconductors – as procurement teams weigh emissions data and ethics policies alongside delivery timelines and service-level agreements.

To meet demand, companies are investing in ESG-focused digital tools, embedding reporting capabilities into enterprise systems, and training frontline teams to speak the language of sustainability. The goal isn’t just compliance; it’s credibility.

For industrial tech firms, the message is clear: transparency isn’t a liability. It’s leverage.

What Was Optional Is Now Expected

The industrial tech sector is no longer immune to the scrutiny once reserved for high-profile consumer brands. Whether building chips, circuit boards, or heavy equipment, companies are being judged not just on what they make, but on how they make it, what they emit, and who they employ.

Procurement has become a proving ground. ESG credentials are now as critical as certifications and specs. The risk isn’t reputational for firms unprepared to meet these expectations – it’s commercial. Buyers are choosing partners who reflect their values, and those values are becoming quantifiable.

As regulatory timelines shorten and client expectations rise, the question isn’t whether to disclose but whether you’re disclosing enough, soon enough.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Protein has slipped out of the gym and into everyday life. It’s no longer the domain of weightlifters or meal-prep obsessives, but something far more ordinary and far more widespread. In Britain, it now turns up in desk drawers, schoolbags, glove compartments, and corner shop fridges. It’s being stirred, shaken, squeezed, and snackified. And, crucially, it’s not being consumed for muscle. It’s for focus. For balance. For the small but satisfying sense of doing something right.

Sales of protein bars, powders, and drinks have climbed 24.2% in the past year, pushing the UK’s sports nutrition market to £1.1 billion. But the term “sports” is misleading. For many, protein isn’t about performance at all. It’s about practicality. Commuters pick up ready-to-drink shakes between trains. Office workers reach for a bar between Zoom calls. Parents hand protein yoghurts to teenagers because they feel vaguely healthier than crisps. Protein, today, is about keeping things ticking over.

That quiet normalisation is most obvious on the high street. Where once there was a dusty corner of the supermarket for “active lifestyles”, now there are prominent displays of high-protein snacks, cereals, bakery items, and even desserts. It’s a word that works across the nutritional spectrum, something that can sit beside indulgence as easily as it can beside restraint.

And British shoppers aren’t short on options. Shelves are filled with chocolate-coated, dairy-free, oat-based, and whey-packed bars, flavoured with everything from peanut butter to salted caramel. The variety says as much about branding as it does about diet. Protein has become shorthand for modern food values: a desire for function, as well as taste, convenience, and, increasingly, identity.

Protein is no longer just a supplement. For many, it reflects small, everyday choices that align with broader intentions—eating well, staying alert, and maintaining balance. In a culture increasingly shaped by wellbeing, high-protein foods offer a quiet reassurance that you’re doing something good for yourself.

What’s Driving the Protein Push

What’s driving protein’s rise isn’t hype, but how effortlessly it fits into everyday routines. Unlike other health trends that require restriction or reinvention, protein works quietly in the background, adding structure, energy, and reassurance. From Gen Z to pensioners, each generation is finding its own reasons to embrace it.

Millennials and Gen Z are leading the shift, but they’re not chasing muscle gains. Recent research revealed that over 60% of UK adults under 35 say they consume high-protein foods to feel energised and manage stress, rather than for fitness. On platforms like TikTok, #highproteinmealprep has surpassed 700 million views, with fridge tours and influencer routines turning protein bars and powders into everyday essentials. These are not supplements. They are lifestyle markers, shared as much for accountability as for aesthetics.

Yet the interest is not confined to the under-40s. In a recent survey, 45% of UK consumers over 55 said they were increasing protein intake to support healthy ageing. This group is not buying protein for trend’s sake, but for muscle preservation and mobility. The shift reflects a broader awareness that protein is not just for the gym. It is a foundation for long-term wellbeing.

One motivation stands out across age groups and lifestyles: functionality. Unlike diets that cut, cleanse, or punish, high-protein choices add something. They help people feel fuller, stay sharper, snack less, and simplify mealtimes. This reflects Britain’s broader wellness economy, where the emphasis is on feeling well rather than performing wellness.

This also helps explain why consumers prefer familiar formats. Bars, shakes, yoghurts, and puddings continue to dominate, not because they are new, but because they are practical. Most shoppers are not looking for lab-designed alternatives. They want recognisable foods that fit their habits and offer clear functional benefits.

The result is not a fleeting trend, but a gradual evolution in how people approach food. Protein is not a disruptor. It is an enabler. It offers small, practical wins that add up over time. In a culture where wellness is no longer niche, that promise holds lasting appeal.

The Brand Strategy Behind the Boom

As the appetite for protein grows, so too has the way it is marketed. In supermarkets and corner shops alike, protein is no longer confined to the health aisle. It appears on endcaps, in meal deals, and even in vending machines. It has been repositioned not as a supplement, but as a shortcut to modern living.

Marketing once focused on performance: leaner, stronger, faster. Now it leans toward everyday credibility. Products no longer ask consumers to train harder. They position themselves as tools to help people keep going. UFIT’s ready-to-drink shakes, for instance, are priced at £1.79 for a grab-and-go bottle, aimed at shoppers who have never set foot in a supplement store. Grenade, one of the UK’s bestselling protein bar brands, leads with indulgence rather than nutrition. Flavours like white chocolate cookie, fudge brownie, and peanut butter make the experience feel more like a treat than a transaction.

Even traditionally masculine brands like Jack Link’s have adapted. The US-born jerky maker now invests in UK campaigns across esports, festivals, and social media. This is no longer protein for the gym. It is protein for gaming, raving, and late-night snacking. The shift is strategic. In Britain, protein has become a lifestyle.

Much of this success comes down to the flexibility of the format. Bars and shakes don’t require a new habit. They fit easily into existing ones. That’s also why brands have doubled down on packaging that communicates quickly, using bold labels like “20g PROTEIN,” simplified ingredient lists, and soft colour palettes borrowed from the wellness world.

And the storytelling doesn’t stop at the shelf. Influencer partnerships, especially with micro-influencers who reflect everyday routines, have helped protein products blend seamlessly into social feeds. Not as a flex, but as a cue. In a world where the line between food and self-image continues to blur, that visibility matters.

In the UK, brands aren’t selling protein as performance. They’re selling it as permission. Permission to snack, to simplify, to opt into health without opting out of pleasure. It is this careful balance between function and familiarity that has propelled protein from niche to necessity.

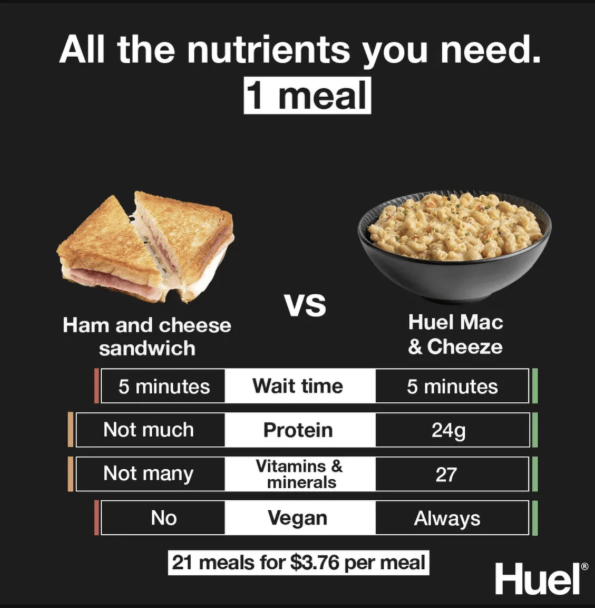

Image credit: Huel

Huel’s success tells a story far bigger than meal replacement. Founded in the UK in 2015, the brand launched with a promise of nutritional completeness and convenience, offering vegan shakes and powders for those too busy to cook but unwilling to compromise on health. It quickly moved from niche to norm, propelled by savvy digital marketing and a cult-like community of professionals, students, and time-pressed urbanites.

What makes Huel notable is how it positioned protein as a practical staple instead of a specialist tool. Its expansion from online-only sales to supermarket shelves brought ready-to-drink shakes and bars into the hands of everyday shoppers. By 2024, Huel’s global footprint had reached 25,650 stores, its UK retail presence strengthened, and its annual sales hit £214 million, an increase of 16 percent year-on-year. The brand’s profitability also grew sharply, with pre-tax profit nearly tripling in the same period.

Huel hasn’t leaned on performance or indulgence. Instead, it has championed efficiency, routine, and nutritional balance, values that resonate with modern British consumers, especially millennials and Gen Z. In doing so, it helped redefine what protein means in everyday life.

How the UK Compares Globally

Britain’s protein habit may feel local, but it is playing out on a global stage. Around the world, consumers are rethinking when and why they reach for protein. Yet the UK stands apart not in volume, but in tone. While other countries frame protein around performance, Britain treats it more like a life skill. It is about balance, ease, and everyday upkeep.

In the United States, the trend has gone maximalist. Protein shows up in ice cream, pancake mix, breakfast cereal, and even candy. Proffee, a mash-up of protein and iced coffee, started as a TikTok trend and quickly moved into cafés and ready-to-drink ranges. Sixty-three percent of Americans actively look for protein in snacks. The line between indulgence and function is all but gone.

In Southeast Asia, the shift looks different. Economic growth has made animal protein more accessible, driving up demand. At the same time, younger consumers in countries like Thailand and Singapore are drawn to plant-based alternatives, which they associate with health, sustainability, and modernity. In Thailand, sixty-seven percent of consumers say they plan to reduce meat consumption. The motivation is not ethical but personal. People want to feel better and live longer.

In Japan, protein trends are shaped by age. An older population is fuelling demand for products that support strength and mobility but are easy to consume. Protein jellies, soft snacks, and drinkable supplements are now common, pitched as daily maintenance rather than athletic fuel.

China is experiencing a boom in online protein sales, up sixty-eight percent yearly in 2023. A mix of fitness aspirations and beauty messaging drives the growth. Protein powders are popular with women and have been promoted as tools for weight management and skin health. Livestream shopping and influencer campaigns sell a lifestyle as much as a product.

In India, the conversation is still emerging. A large percentage of the population remains protein deficient, but a growing middle class is engaging with protein as a marker of wellbeing. Dairy brands like Amul have launched fortified lassi and ice cream, positioning protein as both nutritious and desirable.

Across these regions, protein is rising in relevance. But few markets have made it as ordinary as the UK. Here, it is not aspirational or remedial. It is part of the meal deal, the snack shelf, and the weekday routine. It does not announce itself. It just fits.

The Rise of a Rotational Approach to Protein

Protein may be having its moment, but British shoppers are not choosing sides. The surge in high-protein eating has not sparked a divide between meat and plants. Instead, people are mixing both, often within the same day, and sometimes the same meal.

Part of the shift is pragmatic. Meat remains central to most diets, but plant-based options have gained ground as a way to lighten meals without losing satisfaction. The UK leads Europe in plant-protein innovation, accounting for roughly 18 percent of all new product launches. Supermarket shelves now carry lentil-based pasta, oat-protein shakes, vegan protein bars, and meat-free versions of familiar British dishes.

This is not happening because the nation has gone vegetarian. Most consumers still identify as omnivores or flexitarians. What has changed is the desire for variety and balance. A plant-based lunch does not preclude roast chicken at dinner. It simply reflects a flexible approach to food, guided by mood, values, or convenience.

Protein branding speaks to this shift. On one shelf, whey-based shakes and jerky target muscle and recovery. A few paces away, pea-protein bars promise calm, clarity, and clean ingredients. Both are selling, often to the same household. In The Telegraph’s round-up of the year’s best protein bars, vegan and dairy-based options sit side by side, not as rivals but as parallel answers to different needs.

Taste, convenience, and credibility matter more than protein source. Shoppers want it to work, but they also want it to feel right—nutritionally, culturally, and ethically. The success of the category depends less on what it is made from and more on how well it fits into daily life.

In Britain, this is not about replacement. It is about rotation. And that, more than anything, explains why protein has found a place across such a wide swathe of the population.

What the Protein Economy Means for the Future

Protein may be having its moment, but British shoppers are not choosing sides. The rise of high-protein eating has not triggered a divide between meat and plants. Instead, people are blending both, often within the same day, and sometimes the same meal.

Part of this shift is practical. Meat remains a staple, but plant-based options have gained ground as a way to lighten meals without sacrificing taste. The UK leads Europe in plant-protein innovation, responsible for around 18 percent of all new launches. Supermarkets now stock lentil-based pasta, oat-protein shakes, vegan protein bars from brands like Huel and Tribe, and meat-free versions of familiar dishes.

This is not happening because the country has gone vegetarian. Most consumers still identify as omnivores or flexitarians. What has changed is the desire for variety and balance. A plant-based lunch does not mean skipping chicken at dinner. It simply reflects a flexible, responsive way of eating.

Protein branding follows suit. On one aisle, whey-based shakes and jerky from brands like UFIT and Jack Link’s are positioned for strength and recovery. Nearby, pea-protein bars and oat-based products promise calm, energy, and simplicity. Both types sell, often to the same person.

Taste, convenience, and credibility matter more than the source. Consumers want protein that works, but they also want it to align with their habits, values, and sense of self. Success in this category depends not on whether the protein is animal or plant, but on how well it fits into daily life.

In the UK, this is not about replacement. It is about rotation. And that, more than anything, explains why protein has broad appeal across generations, income brackets, and lifestyles.

Looking to understand the next wave of protein consumers? At Kadence International, we help brands uncover what drives demand, from satiety to sustainability, and how to connect with evolving needs through the right formats, flavours, and messaging. Whether you’re refining recipes, developing new product lines, or targeting new segments, our research gives you the evidence to act confidently. Get in touch to see how we can support your next move.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Marketing history is full of examples where even the most innovative companies misjudged consumer demand. Juicero attracted $120 million in funding for a Wi-Fi-connected juice press—only for the product to be scrapped within two years after consumers showed little interest. ESPN’s mobile phone service failed to take off due to a high price point and limited handset options. And New Coke remains one of the most infamous examples of misjudged brand innovation.

Even Google Glass failed to achieve traction, arguably due to timing, pricing, and lack of consumer readiness.

These cautionary tales underscore why concept testing is so essential. By validating product ideas with your target audience before launch, brands can avoid costly mistakes and build offerings that genuinely connect with consumer needs.

One thing is clear: whatever you launch has to be right. The problem is, “right” isn’t something you get to decide.

Your customers do.

It doesn’t matter if your team loves the idea. It doesn’t matter how clever the name is or how polished the prototype looks. If your target audience doesn’t understand it, want it, or find value in it—it’s not going anywhere.

That’s why the smartest brands don’t leave it to chance. They ask the people who matter most—before it’s too late to change direction. This is where concept testing comes in, delivering early, actionable feedback from your target audience.

What is concept testing?

Concept testing is how brands evaluate and refine ideas before taking them to market. It’s a way to pressure-test new concepts—whether that’s an entirely new product, a rebrand, or a packaging refresh—before major investment.

The concept itself could be a never-before-seen innovation or simply a new twist on something familiar. Either way, it pays to ask the right questions early on:

Does the concept meet real consumer needs? Do people understand it? Does it resonate?

Is the price right? What are people willing to pay? Is the idea commercially viable?

How should it be positioned? Does it fit the brand? How does it stand out from competitors?

What needs to be improved? Are key features missing, confusing, or unnecessary?

Concept testing isn’t a single method. It’s a suite of research tools—from concept screening surveys to qualitative interviews—designed to uncover the strongest ideas and shape them into winning propositions. The approach depends on the challenge, the category, and the stage of development.

Why concept testing matters

Concept testing takes time, effort, and budget. But skipping it is far more expensive.

Launching without feedback risks wasting not only investment but reputation. Failed products don’t just disappear—they can damage brand equity and undermine trust. The cost isn’t always visible in quarterly reports, but it shows up in lost momentum, team morale, and market position.

Concept testing isn’t just risk mitigation—it’s market strategy made smarter.

The history of product innovation is filled with high-profile flops—even from some of the world’s biggest brands.

The Amazon Fire Phone failed to gain traction despite the tech giant’s backing. With a high price tag, confusing interface, and lack of compelling features, it launched into a market already dominated by better-established smartphones.

Google’s Stadia, its cloud gaming platform, shut down just three years after launch. Despite promising a new era of gaming without consoles, it lacked exclusive content, struggled with latency, and failed to capture a committed user base.

Crystal Pepsi, relaunched in the 2010s after a brief 1990s run, was again pulled from shelves when nostalgic appeal couldn’t make up for consumer confusion over the taste.

Concept testing helps brands avoid these pitfalls. It identifies what works, what doesn’t, and why—long before a launch is on the line.

More than just risk mitigation, concept testing is a way to move forward with clarity and confidence.

To better understand how to choose the right research tools for the job, it helps to explore the differences between concept testing and related approaches. While concept testing evaluates the appeal, clarity, and potential of early ideas, test marketing is a more advanced phase that focuses on launch readiness—often requiring prototypes, pilots, or small-scale rollouts.

The choice of concept testing method should reflect the stage of development you’re in. If you’re still refining the idea, early-stage concept screening or co-creation research may be more appropriate than fully structured surveys. On the other hand, if you’ve already narrowed your shortlist, tools like conjoint analysis or max diff can help compare features and pricing more precisely.

At Kadence, we support brands at every point on this journey—whether you’re seeking feedback on rough ideas or testing final-stage execution. Visit our concept testing services page to explore how we design studies that match your market, method, and moment.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

9 Use Cases for Concept Testing

1. Validate whether your idea will take off

Just because something feels like a good idea doesn’t mean it’s market-ready. Concept testing gives brands evidence—rather than gut instinct—on whether a new idea resonates with real consumers. It’s a chance to double down on the right concepts and walk away from the rest.

2. Cut through internal debate

Strong opinions can stall progress. Concept testing gives everyone—from product teams to stakeholders—objective data to work from. It brings clarity to creative discussions and helps unify decision-making around what the audience actually wants.

3. Compare competing concepts

Put multiple ideas in front of consumers and let them decide. Online concept testing lets you test head-to-head and identify clear winners before moving into development.

4. Prioritize the right features and benefits

Which features matter most? Which could be dropped without impact? Testing helps refine the value proposition by spotlighting what your audience really cares about.

5. Understand price sensitivity

A concept isn’t viable unless it can be sold profitably. Testing can uncover how much consumers are willing to pay and what pricing tier the concept fits.

6. Iterate before you launch

Concept testing isn’t just a greenlight mechanism. It’s a feedback loop. Test, tweak, retest—until the idea is tight.

7. Find your ideal audience

Early testing can reveal which segments respond best—whether that’s by age, income, lifestyle, or geography. That insight can shape both product development and marketing.

8. Fine-tune your messaging

The best idea still needs the right words. Use concept testing to explore different messages, formats, or taglines before you commit to a campaign.

9. Continue learning post-launch

Testing doesn’t stop at go-live. Keep tracking reactions to refine your offer, improve communication, or inform future versions.

Does concept testing really work?

Some brand leaders believe that true innovation comes from bold intuition—not research. There’s the often-quoted line about Henry Ford: “If I had asked people what they wanted, they would have said faster horses.”

But Ford wasn’t anti-feedback. He understood that innovation isn’t about asking people what they want—it’s about understanding what they value. That’s where concept testing proves its worth.

At Kadence, concept testing goes beyond asking respondents to pick a favorite. We design studies that uncover emotional triggers, hidden expectations, and real-world trade-offs—between product features, brand fit, and price.

It’s not about dumbing down ideas. It’s about making sure the best ones succeed.

The Kadence Approach to Concept Testing

Our approach blends both qualitative and quantitative methods, tailoring the study design to the market, objective, and stage of development. Below are a few examples of how concept testing delivers results:

Toiletries

A personal care brand wanted to create a new line of shower gels for teenagers. We began with an online concept screening survey to identify early-stage winners, then moved into co-creation sessions with the target audience. The result: a validated, compelling range of fragrance and packaging ideas ready for development.

Takeaway Coffee

To tap into the summer iced coffee market, a global beverage brand partnered with us to run a full concept development sprint. After an internal ideation workshop, we tested multiple drink concepts and price points using online quantitative methods. Follow-up focus groups fine-tuned the winning ideas. The brand launched with confidence, backed by clear consumer demand data.

Travel Advertising

For a national tourism board, we tested multiple ad concepts to see which creative route would drive the greatest increase in intent to visit. By establishing a baseline and tracking uplift across variations, we helped the client land on messaging and visuals that resonated most with high-value travelers.

Food (B2B)

A major food brand wanted to explore the viability of a direct-to-customer (D2C) model for its business buyers. Through in-depth interviews, we tested different fulfillment concepts and gathered feedback on brand perception, value, and pricing. Insights helped shape a more appealing offer with a clear route to market.

Research methods for concept testing

At Kadence, we use a range of concept testing methods—qualitative, quantitative, and hybrid—depending on the stage of development and the decisions a brand needs to make.

We don’t lead with methodology. We start by asking the right questions. What do you already know? Are you testing multiple concepts or refining one? Do you need high-level feedback or deep diagnostic insight? Should your focus be on emotional resonance, commercial potential, or both?

The answers shape our approach.

If you’re deciding which research technique to use, your approach should match the development phase you’re in. For example, exploratory qualitative research can help shape ideas during early-stage innovation, while online surveys are ideal when you’re comparing finalised concepts at scale. We break this down in our guide to how to conduct concept testing for different stages of product development, which outlines which tools to use—and when.

Online Surveys

Online concept testing is one of the most effective ways to gather structured feedback at scale. Surveys can reach thousands of carefully profiled respondents, producing data that can be analyzed, ranked, and compared across audiences. Our team builds surveys that simulate real-world decisions—allowing brands to test features, pricing, and positioning in controlled conditions. We then apply advanced statistical techniques to extract what matters most.

Qualifying the Right Audience

Before diving into the core of the concept test, we recommend using screener questions to ensure you’re speaking to the right respondents. These filter out participants who don’t meet your criteria, like frequency of use, category involvement, or geography.

Demographic questions—such as age, income bracket, and profession—are typically placed at the end. They allow for segmentation analysis without overwhelming the participant up front. When used thoughtfully, this profiling ensures your results reflect your true target market.

Focus Groups

Focus groups deliver the kind of texture and nuance you can’t get from numbers alone. Whether online or in-person, they create a space where consumers engage with your concept, react in real time, and build on each other’s thoughts. We use these sessions to uncover gut reactions, decode emotional cues, and surface new angles that spark further refinement.

Depth Interviews

When individual perspective matters more than group dynamics, depth interviews offer space to go deeper. We speak one-on-one with target users to explore motivations, hesitations, and behavioral drivers—often revealing insights that shape messaging, design, or product positioning.

Ethnography

Sometimes, the richest insights come from observation rather than direct questioning. Ethnographic research puts us in the everyday environments of your target audience. Through diaries, photo journals, and in-context observation, we gain a clearer picture of the unmet needs and behaviors that influence purchasing decisions.

Online Communities

Online concept testing communities allow brands to capture evolving feedback over time. These short-term, private digital spaces encourage participants to interact with your concepts through posts, videos, and tasks. Unlike traditional surveys, communities evolve as the research progresses—ideal for iterative concept development or creative refinement.

By matching the right method to the right stage, we help brands maximize insight while staying conscious of timing, scale, and cost.

Comparing Concept Testing Methods

Method

Best For

Key Benefits

Online Surveys

Screening and prioritizing multiple concepts at scale

Fast turnaround, scalable, enables clear comparison across attributes like price and features

Focus Groups

Exploring emotional reactions and creative direction

Rich qualitative insight, visual feedback, discussion of messaging and positioning

Depth Interviews

Understanding motivations and reactions in detail

In-depth exploration of decision-making, barriers, and expectations

Ethnography

Observing how people interact with concepts in real life

High authenticity, uncovers unmet needs and real-world context

Online Communities

Iterative concept development and testing over time

Continuous feedback, co-creation, adaptable over several days or weeks

Not sure whether concept testing or test marketing is the right approach for your stage? While both involve gathering real consumer feedback, they differ in purpose, timing, and scale. Explore our breakdown of concept testing vs. test marketing to understand which method best fits your innovation pipeline.

Choosing Between Monadic and Sequential Design

Two of the most common approaches in survey-based concept testing are monadic and sequential designs. In a monadic design, participants evaluate one concept in isolation, allowing for deep focus and reducing bias. This method delivers high-quality feedback but requires a larger sample size to compare concepts statistically.

A sequential design—where respondents review multiple concepts in one sitting—is faster and more cost-effective, especially in early screening stages. However, results can be influenced by order effects and fatigue, so it’s essential to randomize presentation order and monitor data quality carefully.

How Long Should a Concept Survey Be?

Length affects engagement. In our experience, surveys for concept testing perform best when kept under 25 minutes or 30 questions. Beyond that, respondent fatigue sets in, and data quality drops. Shorter, focused surveys tend to yield clearer insights—and make it more likely participants give considered feedback.

Making Sense of the Data

In survey-based concept testing, many responses are captured using Likert scales—asking how likely someone is to buy, how appealing a concept is, or how innovative it feels, rated on a 5- or 7-point scale.

One of the most actionable ways to interpret this data is by using Top 2 Box scoring: calculating the percentage of respondents who selected the top two positive responses (e.g., “very likely” or “likely”). This allows for fast comparison across multiple concepts and reveals which ideas stand out from the crowd.

Whether you’re running a product concept survey, testing pricing scenarios, or evaluating new messaging, these metrics can reveal what matters most to your audience.

The Role of Design

At Kadence, we bring creativity to every stage of concept testing, combining research expertise with in-house design capabilities to help brands move from idea to impact.

Often, the early concepts we receive are rough. They might start as a few words on a Post-it note or a collage of reference images. That’s where our design team steps in. We transform early-stage ideas into tangible stimuli that consumers can engage with—whether that’s a mock-up of an ad, a service visualisation, a website prototype, or test copy for a landing page.

We’re also exploring the use of augmented reality (AR) to elevate product concept testing. Using AR, we can generate digital 3D prototypes that participants can view through their smartphones in real environments. This approach enhances engagement and delivers more authentic feedback—especially when compared to static visuals—while remaining highly efficient and scalable.

Beyond visual execution, our work is shaped by the principles of design thinking, a framework that ensures ideas are developed with consumer needs at the center.

The five stages of design thinking include:

Empathise: Understand your audience’s real-world context, needs, and pain points.

Define: Frame the core problem or opportunity you want to solve with precision.

Ideate: Brainstorm solutions based on what the research has revealed so far.

Prototype: Build a working version—whether physical, digital, or visual—for feedback.

Test: Put your concept in front of your audience, gather reactions, and refine as needed.

Many of our clients reach us during the ideation or prototype phase, but concept testing can also inform earlier and later stages. Our design-led, research-backed approach is part of what makes concept testing with Kadence more actionable and more commercially relevant.

10 Top tips for successful concept testing

Set clear objectives Start with a focused brief. What exactly do you want to learn—and how will you act on the findings? Whether you’re choosing between concepts or refining a single idea, clarity up front keeps the research sharp and the results meaningful.

Don’t fall too in love with your ideas Concept testing isn’t about validating hunches. It’s about letting the customer response guide decisions. Stay open. If a promising product concept flops in testing, let it go. Great ideas are rarely one-offs—and the right research helps you spot what’s worth pursuing.

Find the right people Your target audience matters more than volume. We’ve tested concepts with teenage gamers, healthcare professionals, rural farmers, and C-suite decision-makers. Whether you need broad reach or a niche segment, finding the right participants is half the battle.

Bring it to life Early-stage ideas often need help becoming real for consumers. That’s why our in-house team turns sketches, mockups, and rough copy into visuals that spark real feedback. The stronger the stimulus, the sharper the insight.

Iterate quickly and often Few concepts are perfect the first time. That’s why iterative testing—refining, retesting, refining again—gets better results. We use agile design and research cycles to sharpen ideas quickly, often in just days.

Stay flexible Concept testing is not a fixed recipe. Sometimes you need a quick screen. Other times, deep qualitative work. Let your goals and the audience shape the approach—not the other way around.

Listen beyond the words Good research isn’t just about what people say—it’s how they say it. Our researchers are trained to pick up on hesitations, contradictions, and patterns that reveal deeper insight into what people really think.

Context matters A winning idea on paper might underperform in the real world. Test in context: how the idea compares to alternatives, fits with your brand, and lands emotionally with the audience. Concept scores are just one piece of the puzzle.

Protect your IP Early concepts are sensitive. We’ve built secure systems to ensure designs, copy, and mockups stay confidential. Features like watermarked images and self-destructing videos help reduce leaks—and in over a decade, we haven’t seen one.

Keep testing after launch Consumer needs shift fast. Great brands keep refining after launch. Concept testing isn’t a one-off event—it’s a habit. Keep listening, keep adjusting, and your product stays relevant.

Why It Pays to Get Concept Testing Right

Every great brand knows this: launching a new product isn’t just about creativity or gut feel. It’s about getting closer to your audience—understanding their reactions, their hesitations, their unmet needs—and building from there. That’s what concept testing delivers.

It’s not a barrier to innovation. It’s the mechanism that makes innovation work.

When done right, concept testing doesn’t just tell you which ideas are most appealing. It helps you craft better ones. It shows you where to focus investment, how to improve your offer, what to communicate, and—crucially—what not to pursue. It gives teams clarity, stakeholders confidence, and brands a stronger shot at real-world success.

Because the difference between a bold idea and a breakthrough product isn’t luck. It’s research-backed confidence.

To explore how concept testing services can support your product development process—whether you’re refining early ideas or validating go-to-market strategies—learn more about our concept testing solutions.

Rising inflation and economic uncertainty were expected to put an end to discretionary spending for middle-income households. Instead, consumers are making room for indulgence. Across the US, UK, and Europe, households earning moderate incomes continue to prioritise non-essential purchases at rates far closer to affluent consumers than economic models predicted. McKinsey’s 2024 Global Consumer Sentiment Survey found that 42% of middle-income respondents in developed markets still plan to spend on travel, dining out, and personal care in the next year, just nine percentage points lower than high-income households.

The resilience of discretionary spending in the face of rising costs defies conventional economic assumptions. It is not a case of irrationality or denial. It reflects a shift in how consumers measure value. After years of pandemic-driven disruption, middle-class buyers are increasingly framing small luxuries as essential to emotional well-being, not as reckless spending. An affordable meal out, a short domestic trip, or a new skincare product carries more than monetary worth. It represents normalcy, reward, and agency in an environment where larger financial goals often feel less attainable.

This trend is not a short-term reaction to inflation, nor is it purely sentimental. It is structurally rational behaviour shaped by stress, lifestyle adjustment, and evolving definitions of security. Spending on modest treats provides a sense of control and immediacy when long-term stability—home ownership, retirement savings—feels increasingly out of reach. Consumers are not abandoning caution; they are recalibrating what prudence looks like in real terms.

Understanding this shift is critical for brands, retailers, and policymakers. Indulgence spending among the middle class is not a deviation from rational economic behaviour. It is an adaptation to new realities, where emotional resilience and quality of life have become primary considerations alongside price and necessity.

Tight Budgets, Sharp Choices

The pressure on household budgets is real. Inflation has driven up the cost of essentials—housing, food, energy—leaving less flexibility for discretionary categories. Yet rather than abandoning non-essential purchases altogether, middle-class consumers are reprioritising with striking precision. The pattern is visible across the US, UK, and Europe: subscription services are among the first to be cancelled, big-ticket electronics are postponed, and plans for major home renovations are shelved. But the impulse to carve out space for small luxuries remains intact.

KPMG’s 2024 Middle-Class Financial Priorities report highlights this shift. In a survey of households earning between 75% and 150% of median income, nearly 60% reported cutting back on monthly expenses such as media subscriptions and dining delivery apps. However, the same respondents overwhelmingly indicated an intention to preserve budget for “quality of life” items, including occasional dining out, personal care products, and leisure travel under 500 miles. The data suggests that discretionary spending is not vanishing—it is being filtered through a more selective lens.

A similar rebalancing is evident in Europe. OECD research published earlier this year shows that while the ownership of new vehicles among middle-income households declined by over 8% between 2022 and 2024, spending on local travel, cultural events, and speciality food purchases held steady. In the UK, Deloitte’s 2024 consumer tracker found that middle-income households were 30% more likely to describe smaller, experiential purchases as “essential for well-being” than they were before the pandemic.

The underlying dynamic is a redefinition of value. Consumers are moving away from evaluating purchases solely on cost or prestige. Instead, the metric is experiential reward—whether a purchase delivers emotional uplift, stress relief, or a sense of personal investment. A $50 skincare product or a weekend away is justified not by indulgence for its own sake, but by what it represents: a manageable, affirming investment in quality of life.

This sharpening of priorities is not a retreat from financial responsibility. It is a recalibration. Households are preserving choice and pleasure even as long-term goals grow more distant. The middle-class response to inflation is not to close the wallet entirely, but to spend carefully, reinforcing emotional resilience where it matters most.

Where the Money Is Still Flowing

The resilience of middle-class discretionary spending becomes clearest when looking at where the money continues to move. Small luxuries, particularly those offering immediate personal gratification without long-term financial strain, are absorbing a disproportionate share of discretionary budgets. These are not extravagant purchases but considered indulgences—choices that allow consumers to feel rewarded without incurring future economic risk.

Dining out remains one of the strongest performing sectors. Mastercard SpendingPulse data from early 2024 showed that spending at fast-casual and premium-casual restaurants in the US rose by 8% year-on-year, even as fine dining bookings declined. Consumers are trading down from high-end experiences but refusing to give up the social and emotional value of meals shared outside the home. In the UK, Statista reports that visits to casual dining chains increased by nearly one-fifth compared to 2022 levels, concentrated among households earning £30,000 to £70,000 annually.

Beauty and skincare purchases are following a similar trajectory. McKinsey’s 2024 Global Beauty Survey found that middle-income consumers accounted for nearly half of the growth in skincare sales across Europe and North America, often favouring mid-tier brands offering “clinical-grade” results at accessible prices. Rather than abandoning beauty spending, buyers are shifting toward products that promise tangible outcomes—improved skin health, self-care benefits—over prestige branding. The emphasis is not on conspicuous consumption but on self-affirmation.

Domestic travel, particularly short-haul trips, has also proven remarkably resilient. According to Mastercard’s travel trends report, bookings for domestic leisure trips under 300 miles rose by 12% in the US during the past year, primarily driven by middle-income households. European markets such as France and Germany showed parallel trends, with regional rail and car rental bookings outperforming international air travel. Travel, even scaled down, remains a critical outlet for recreation and stress relief, viewed as a justifiable investment rather than a luxury.

Personal wellness has evolved from a niche concern to a consistent budget item. Deloitte’s 2024 Health and Wellness Tracker found that expenditures on fitness apps, meditation subscriptions, and nutritional supplements rose by nearly 15% among middle-income consumers compared to 2022. Spa treatments and boutique fitness sessions also saw modest but steady gains, especially when bundled into affordable packages. Wellness is increasingly framed not as optional self-indulgence but as proactive health maintenance—a narrative that middle-class consumers embrace even under financial strain.

What ties these sectors together is not mere resilience but strategic prioritisation. Consumers actively choose experiences and products that deliver emotional payoff without undermining longer-term financial goals. Small luxuries have become part of how households navigate financial pressure, balancing restraint with resilience.

How Indulgence Looks Different Around the World

The appetite for small luxuries is global, but its expression varies sharply across markets. Cultural context, inflationary pressure, and recovery patterns from the pandemic shape how and where middle-class consumers indulge.

In the United States, experience is taking precedence over material accumulation. Mastercard’s 2024 SpendingPulse report shows that while retail sales for durable goods have slowed, spending on travel, dining, and entertainment continues to climb. Middle-income households prioritise activities that create memories and offer a sense of immediacy, even as they pull back on home goods and apparel. The pattern reflects a broader recalibration, where the value of money is increasingly measured in lived experience rather than possessions.

The United Kingdom mirrors this behavioural split, though with sharper trade-offs. Ipsos data published earlier this year indicates that middle-income British households are aggressively trading down on everyday essentials—switching to discount supermarkets and delaying home improvements—while deliberately protecting spending on experiential categories. Budget airline bookings, concert attendance, and dining at independent restaurants remain surprisingly resilient. The message is clear: not all spending is negotiable, even under pressure.

In continental Europe, the indulgence lens often narrows toward artisanal quality. In France and Germany, Euromonitor reports that while overall household budgets have tightened, purchases of artisanal food, skincare, and local leisure travel have held steady or even grown modestly. Consumers are not abandoning discretionary spending, but are redirecting it toward smaller, more meaningful pleasures that emphasise craftsmanship, locality, and authenticity.

Southeast Asia presents a different dynamic, driven by digital acceleration and aspirational consumption. In Singapore, Indonesia, and the Philippines, middle-income consumers are investing in affordable upgrades—beauty products, domestic travel, and entry-level tech such as smartphones and wearable devices. According to Bain & Company’s 2024 Southeast Asia Digital Economy Report, there has been a surge in beauty e-commerce, with mid-tier brands seeing the fastest growth among urban middle-class buyers. Here, indulgence is closely tied to self-improvement and digital connectivity rather than traditional luxury markers.

China and India present a distinct dynamic. In China, middle-class consumers focus on premium health, wellness, and education-related services. Mastercard’s 2024 China Consumption Outlook shows strong growth in short domestic leisure travel, boutique fitness memberships, and “new luxury” beauty brands that offer substance over logo appeal. In India, indulgence is often family-centred. Euromonitor data highlights that spending on family experiences—mall outings, cinema, casual dining, and affordable domestic holidays—is being prioritised, even as households economise on electronics and apparel. The middle class is seeking small windows of joy that offer collective, not just individual, payoff.

Across these regions, indulgence spending is far from homogeneous. It is shaped by cultural narratives about success, wellness, and emotional reward. Yet the underlying behaviour is consistent: even under inflationary strain, middle-income consumers are unwilling to surrender the experiences and products that sustain a sense of control, progress, and personal value.

Why Indulgence Feels Necessary, Not Excessive

The persistence of small luxuries in strained economic times is not a matter of consumer irrationality. It is a rational psychological response to prolonged stress, uncertainty, and shifting social norms. For many middle-class households, small indulgences have moved beyond occasional rewards to become a form of emotional maintenance—a way to reassert agency and sustain morale when broader financial goals feel increasingly distant.

Much of this shift can be traced to the post-pandemic “live for today” mindset. After years of deferred plans and disrupted routines, consumers across income levels have shown a greater willingness to prioritise present-day satisfaction. Behavioural economists point to the acceleration of hedonic adaptation—the tendency to return to a baseline level of happiness despite external changes—as a key factor. When future security feels less certain, spending on immediate emotional uplift becomes a practical way to protect mental well-being.

American Psychological Association research on stress-related spending supports this view. A 2024 report found that nearly 60% of middle-income consumers in the US admitted to occasional “treat spending” as a coping mechanism, with the majority framing such purchases not as extravagance, but as essential self-care. Similar patterns emerged in the UK and Singapore, where smaller, experience-driven expenditures were linked to lower reported stress levels in middle-income groups.

Social behaviour further reinforces the normalisation of indulgence. Small splurges—dining out, a weekend getaway, a new skincare regimen—are highly visible on platforms like Instagram and TikTok. Sharing these moments has become part of how consumers construct narratives of resilience and self-investment. The effect is cumulative. What once might have been considered unnecessary spending is now broadly perceived as a reasonable way to manage life’s pressures.

Rather than retreating into austerity, many middle-class consumers are making conscious choices to maintain emotional balance through manageable rewards. In modern economic conditions, where traditional markers of financial progress are harder to achieve, these decisions are not acts of recklessness. They are strategies for preserving stability, dignity, and optimism in everyday life.

Small Luxuries, Big Opportunities

For brands, the persistence of small indulgences offers more than a temporary sales opportunity. It signals a deeper shift in how consumers assign value—one that demands careful strategic recalibration. Positioning products as accessible rewards or emotional enhancers, rather than as markers of status or success, will increasingly define market relevance.

Middle-class consumers are not looking for extravagant gestures. They are seeking personal moments of satisfaction, convenience, or self-expression that fit into constrained budgets. Products that deliver relaxation, confidence, or small affirmations of progress resonate far more than those that lean heavily on traditional luxury cues. In this environment, storytelling around personal value matters more than aspirational branding. A meal kit that saves time and creates family rituals, a skincare serum that represents self-care rather than vanity, a local mini-break that restores mental clarity—these are the narratives gaining traction.

The danger for brands lies in misreading the room. Overemphasising luxury, exclusivity, or aspirational distance risks alienating a consumer base that values relatability and tangible benefit over status. Innovation must centre on affordability without sacrificing the experience of quality. Smart packaging, modular services, and tiered product lines are helping some brands maintain margins while broadening emotional appeal.

Real-time market research is critical to navigating these shifts. Understanding which categories of small luxuries matter most—and how definitions of indulgence vary between regions, income brackets, and life stages—allows brands to tailor offerings with precision. Blanket assumptions about “affordable luxury” no longer hold. The brands that invest in nuanced, behaviour-led insights will be the ones best positioned to capture loyalty in an economy where emotional and financial resilience are increasingly intertwined.

Indulgence in an Age of Restraint

Discretionary spending among middle-income consumers is too often dismissed as irrational, a stubborn refusal to accept economic reality. This view misses the point. Small indulgences are not acts of denial. They are structural adjustments to a world where traditional financial milestones—home ownership, long-term savings, upward mobility—have become harder to secure. Preserving moments of joy, autonomy, and emotional stability has become a rational survival strategy.

Understanding these patterns is critical for anyone forecasting the next phase of consumer behaviour. Micro-indulgence is more than a passing phenomenon. It is a leading indicator of broader consumer sentiment, revealing how confidence, stress, and hope are negotiated at the household level. Brands and policymakers that fail to track these shifts will misread the market, mistaking emotional recalibration for economic irrationality.

At Kadence International, our global research shows that middle-class indulgence is not a short-term reaction to inflationary pressure. It is an embedded behavioural shift, one that will continue to shape spending across sectors well beyond the current cycle. Those who frame their growth strategies around emotional consumption, rather than rigid income segmentation, will be best positioned to capture resilience spending in an economy where financial caution and the pursuit of quality of life are no longer at odds, but deeply intertwined.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

In the last year alone, bookings for luxury river cruises by travellers over the age of 65 rose by more than 70%. In Southeast Asia, spa and wellness retreats report that seniors now make up the fastest-growing customer group. And in the United States, recent data shows that older adults are adopting wearable tech at a faster clip than millennials. These aren’t isolated shifts—they’re signals of a broader recalibration underway in global consumption.