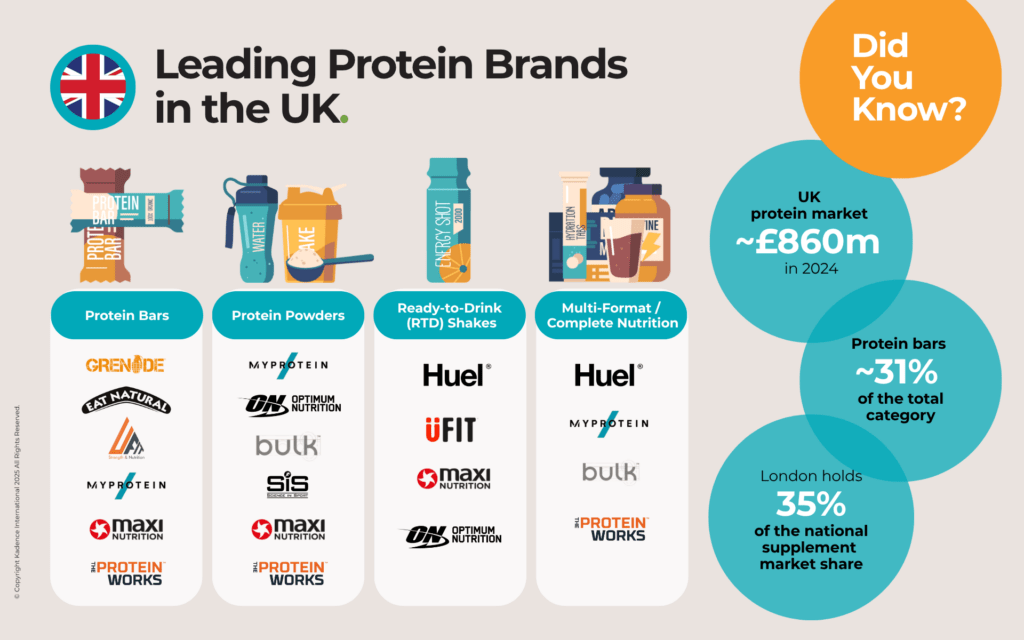

Protein has slipped out of the gym and into everyday life. It’s no longer the domain of weightlifters or meal-prep obsessives, but something far more ordinary and far more widespread. In Britain, it now turns up in desk drawers, schoolbags, glove compartments, and corner shop fridges. It’s being stirred, shaken, squeezed, and snackified. And, crucially, it’s not being consumed for muscle. It’s for focus. For balance. For the small but satisfying sense of doing something right.

Sales of protein bars, powders, and drinks have climbed 24.2% in the past year, pushing the UK’s sports nutrition market to £1.1 billion. But the term “sports” is misleading. For many, protein isn’t about performance at all. It’s about practicality. Commuters pick up ready-to-drink shakes between trains. Office workers reach for a bar between Zoom calls. Parents hand protein yoghurts to teenagers because they feel vaguely healthier than crisps. Protein, today, is about keeping things ticking over.

That quiet normalisation is most obvious on the high street. Where once there was a dusty corner of the supermarket for “active lifestyles”, now there are prominent displays of high-protein snacks, cereals, bakery items, and even desserts. It’s a word that works across the nutritional spectrum, something that can sit beside indulgence as easily as it can beside restraint.

And British shoppers aren’t short on options. Shelves are filled with chocolate-coated, dairy-free, oat-based, and whey-packed bars, flavoured with everything from peanut butter to salted caramel. The variety says as much about branding as it does about diet. Protein has become shorthand for modern food values: a desire for function, as well as taste, convenience, and, increasingly, identity.

Protein is no longer just a supplement. For many, it reflects small, everyday choices that align with broader intentions—eating well, staying alert, and maintaining balance. In a culture increasingly shaped by wellbeing, high-protein foods offer a quiet reassurance that you’re doing something good for yourself.

What’s Driving the Protein Push

What’s driving protein’s rise isn’t hype, but how effortlessly it fits into everyday routines. Unlike other health trends that require restriction or reinvention, protein works quietly in the background, adding structure, energy, and reassurance. From Gen Z to pensioners, each generation is finding its own reasons to embrace it.

Millennials and Gen Z are leading the shift, but they’re not chasing muscle gains. Recent research revealed that over 60% of UK adults under 35 say they consume high-protein foods to feel energised and manage stress, rather than for fitness. On platforms like TikTok, #highproteinmealprep has surpassed 700 million views, with fridge tours and influencer routines turning protein bars and powders into everyday essentials. These are not supplements. They are lifestyle markers, shared as much for accountability as for aesthetics.

Yet the interest is not confined to the under-40s. In a recent survey, 45% of UK consumers over 55 said they were increasing protein intake to support healthy ageing. This group is not buying protein for trend’s sake, but for muscle preservation and mobility. The shift reflects a broader awareness that protein is not just for the gym. It is a foundation for long-term wellbeing.

One motivation stands out across age groups and lifestyles: functionality. Unlike diets that cut, cleanse, or punish, high-protein choices add something. They help people feel fuller, stay sharper, snack less, and simplify mealtimes. This reflects Britain’s broader wellness economy, where the emphasis is on feeling well rather than performing wellness.

This also helps explain why consumers prefer familiar formats. Bars, shakes, yoghurts, and puddings continue to dominate, not because they are new, but because they are practical. Most shoppers are not looking for lab-designed alternatives. They want recognisable foods that fit their habits and offer clear functional benefits.

The result is not a fleeting trend, but a gradual evolution in how people approach food. Protein is not a disruptor. It is an enabler. It offers small, practical wins that add up over time. In a culture where wellness is no longer niche, that promise holds lasting appeal.

The Brand Strategy Behind the Boom

As the appetite for protein grows, so too has the way it is marketed. In supermarkets and corner shops alike, protein is no longer confined to the health aisle. It appears on endcaps, in meal deals, and even in vending machines. It has been repositioned not as a supplement, but as a shortcut to modern living.

Marketing once focused on performance: leaner, stronger, faster. Now it leans toward everyday credibility. Products no longer ask consumers to train harder. They position themselves as tools to help people keep going. UFIT’s ready-to-drink shakes, for instance, are priced at £1.79 for a grab-and-go bottle, aimed at shoppers who have never set foot in a supplement store. Grenade, one of the UK’s bestselling protein bar brands, leads with indulgence rather than nutrition. Flavours like white chocolate cookie, fudge brownie, and peanut butter make the experience feel more like a treat than a transaction.

Even traditionally masculine brands like Jack Link’s have adapted. The US-born jerky maker now invests in UK campaigns across esports, festivals, and social media. This is no longer protein for the gym. It is protein for gaming, raving, and late-night snacking. The shift is strategic. In Britain, protein has become a lifestyle.

Much of this success comes down to the flexibility of the format. Bars and shakes don’t require a new habit. They fit easily into existing ones. That’s also why brands have doubled down on packaging that communicates quickly, using bold labels like “20g PROTEIN,” simplified ingredient lists, and soft colour palettes borrowed from the wellness world.

And the storytelling doesn’t stop at the shelf. Influencer partnerships, especially with micro-influencers who reflect everyday routines, have helped protein products blend seamlessly into social feeds. Not as a flex, but as a cue. In a world where the line between food and self-image continues to blur, that visibility matters.

In the UK, brands aren’t selling protein as performance. They’re selling it as permission. Permission to snack, to simplify, to opt into health without opting out of pleasure. It is this careful balance between function and familiarity that has propelled protein from niche to necessity.

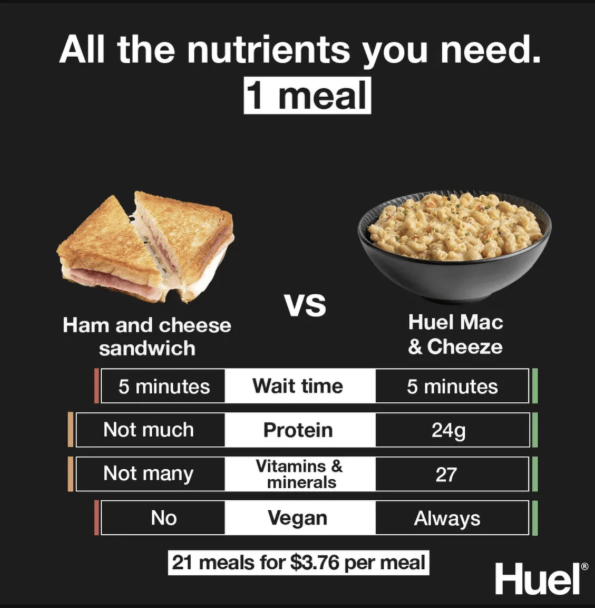

Image credit: Huel

Huel’s success tells a story far bigger than meal replacement. Founded in the UK in 2015, the brand launched with a promise of nutritional completeness and convenience, offering vegan shakes and powders for those too busy to cook but unwilling to compromise on health. It quickly moved from niche to norm, propelled by savvy digital marketing and a cult-like community of professionals, students, and time-pressed urbanites.

What makes Huel notable is how it positioned protein as a practical staple instead of a specialist tool. Its expansion from online-only sales to supermarket shelves brought ready-to-drink shakes and bars into the hands of everyday shoppers. By 2024, Huel’s global footprint had reached 25,650 stores, its UK retail presence strengthened, and its annual sales hit £214 million, an increase of 16 percent year-on-year. The brand’s profitability also grew sharply, with pre-tax profit nearly tripling in the same period.

Huel hasn’t leaned on performance or indulgence. Instead, it has championed efficiency, routine, and nutritional balance, values that resonate with modern British consumers, especially millennials and Gen Z. In doing so, it helped redefine what protein means in everyday life.

How the UK Compares Globally

Britain’s protein habit may feel local, but it is playing out on a global stage. Around the world, consumers are rethinking when and why they reach for protein. Yet the UK stands apart not in volume, but in tone. While other countries frame protein around performance, Britain treats it more like a life skill. It is about balance, ease, and everyday upkeep.

In the United States, the trend has gone maximalist. Protein shows up in ice cream, pancake mix, breakfast cereal, and even candy. Proffee, a mash-up of protein and iced coffee, started as a TikTok trend and quickly moved into cafés and ready-to-drink ranges. Sixty-three percent of Americans actively look for protein in snacks. The line between indulgence and function is all but gone.

In Southeast Asia, the shift looks different. Economic growth has made animal protein more accessible, driving up demand. At the same time, younger consumers in countries like Thailand and Singapore are drawn to plant-based alternatives, which they associate with health, sustainability, and modernity. In Thailand, sixty-seven percent of consumers say they plan to reduce meat consumption. The motivation is not ethical but personal. People want to feel better and live longer.

In Japan, protein trends are shaped by age. An older population is fuelling demand for products that support strength and mobility but are easy to consume. Protein jellies, soft snacks, and drinkable supplements are now common, pitched as daily maintenance rather than athletic fuel.

China is experiencing a boom in online protein sales, up sixty-eight percent yearly in 2023. A mix of fitness aspirations and beauty messaging drives the growth. Protein powders are popular with women and have been promoted as tools for weight management and skin health. Livestream shopping and influencer campaigns sell a lifestyle as much as a product.

In India, the conversation is still emerging. A large percentage of the population remains protein deficient, but a growing middle class is engaging with protein as a marker of wellbeing. Dairy brands like Amul have launched fortified lassi and ice cream, positioning protein as both nutritious and desirable.

Across these regions, protein is rising in relevance. But few markets have made it as ordinary as the UK. Here, it is not aspirational or remedial. It is part of the meal deal, the snack shelf, and the weekday routine. It does not announce itself. It just fits.

The Rise of a Rotational Approach to Protein

Protein may be having its moment, but British shoppers are not choosing sides. The surge in high-protein eating has not sparked a divide between meat and plants. Instead, people are mixing both, often within the same day, and sometimes the same meal.

Part of the shift is pragmatic. Meat remains central to most diets, but plant-based options have gained ground as a way to lighten meals without losing satisfaction. The UK leads Europe in plant-protein innovation, accounting for roughly 18 percent of all new product launches. Supermarket shelves now carry lentil-based pasta, oat-protein shakes, vegan protein bars, and meat-free versions of familiar British dishes.

This is not happening because the nation has gone vegetarian. Most consumers still identify as omnivores or flexitarians. What has changed is the desire for variety and balance. A plant-based lunch does not preclude roast chicken at dinner. It simply reflects a flexible approach to food, guided by mood, values, or convenience.

Protein branding speaks to this shift. On one shelf, whey-based shakes and jerky target muscle and recovery. A few paces away, pea-protein bars promise calm, clarity, and clean ingredients. Both are selling, often to the same household. In The Telegraph’s round-up of the year’s best protein bars, vegan and dairy-based options sit side by side, not as rivals but as parallel answers to different needs.

Taste, convenience, and credibility matter more than protein source. Shoppers want it to work, but they also want it to feel right—nutritionally, culturally, and ethically. The success of the category depends less on what it is made from and more on how well it fits into daily life.

In Britain, this is not about replacement. It is about rotation. And that, more than anything, explains why protein has found a place across such a wide swathe of the population.

What the Protein Economy Means for the Future

Protein may be having its moment, but British shoppers are not choosing sides. The rise of high-protein eating has not triggered a divide between meat and plants. Instead, people are blending both, often within the same day, and sometimes the same meal.

Part of this shift is practical. Meat remains a staple, but plant-based options have gained ground as a way to lighten meals without sacrificing taste. The UK leads Europe in plant-protein innovation, responsible for around 18 percent of all new launches. Supermarkets now stock lentil-based pasta, oat-protein shakes, vegan protein bars from brands like Huel and Tribe, and meat-free versions of familiar dishes.

This is not happening because the country has gone vegetarian. Most consumers still identify as omnivores or flexitarians. What has changed is the desire for variety and balance. A plant-based lunch does not mean skipping chicken at dinner. It simply reflects a flexible, responsive way of eating.

Protein branding follows suit. On one aisle, whey-based shakes and jerky from brands like UFIT and Jack Link’s are positioned for strength and recovery. Nearby, pea-protein bars and oat-based products promise calm, energy, and simplicity. Both types sell, often to the same person.

Taste, convenience, and credibility matter more than the source. Consumers want protein that works, but they also want it to align with their habits, values, and sense of self. Success in this category depends not on whether the protein is animal or plant, but on how well it fits into daily life.

In the UK, this is not about replacement. It is about rotation. And that, more than anything, explains why protein has broad appeal across generations, income brackets, and lifestyles.

Looking to understand the next wave of protein consumers? At Kadence International, we help brands uncover what drives demand, from satiety to sustainability, and how to connect with evolving needs through the right formats, flavours, and messaging. Whether you’re refining recipes, developing new product lines, or targeting new segments, our research gives you the evidence to act confidently. Get in touch to see how we can support your next move.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

British shoppers are entering a new era of grocery buying – less impulsive, more deliberate, and increasingly shaped by price. Grocery inflation rose to 3.5 percent in March, capping off two years of compounded cost pressure. Supermarket sales have softened, not because people are walking away, but because they’re buying fewer items and skipping anything that doesn’t feel essential.

Essentials are winning, volume is shrinking, and price has become the lead story. This shift isn’t just thrift – it’s agency. After months of rising bills and economic fatigue, shoppers are regaining a sense of control by editing their baskets. That often means skipping branded goods and sticking to private labels.

Discounters are reaping the gains. Aldi’s market share is up to 11 percent, and Lidl is outpacing rivals in sales growth. But this isn’t just about who’s winning – it’s about how. Shoppers aren’t compromising; they’re recalibrating. Value now means quality at the right price, not a badge name. What’s happening isn’t tactical – it’s behavioural.

What distinguishes this period from past inflation spikes is the speed and confidence of the switch. Brand loyalty, long considered a mainstay of British retail, is now a conditional contract. If a supermarket can’t justify its price point – through quality, loyalty perks, or convenience – shoppers will walk.

Retailers are moving fast to keep up: shrinking private-label ranges to what works, tuning promotions, and reframing value as a daily promise. On paper, it looks like a margin problem. In reality, it’s a permanent shift in how households define value – and there’s little reason to think it’ll snap back.

This isn’t a belt-tightening moment. It’s a consumer reorientation. People aren’t just buying less; they’re buying differently. And in doing so, they’re quietly forcing a reset in how the UK grocery industry defines, delivers, and earns loyalty.

Inflation at the Checkout: What’s Really Driving the Shift?

Walk through any UK supermarket right now, and the change isn’t just in the receipt – it’s in the way people are shopping. Labels are read more slowly. Own-brand products are picked up, put back, then chosen again. Familiar items suddenly feel like indulgences.

What’s happening at the checkout isn’t just about price increases. It’s a psychological shift. Shoppers aren’t just spending less – they’re thinking differently. The same budget now feels tighter, not only because of higher prices but because of how those prices are being perceived.

Anchoring is one reason. Consumers aren’t comparing this week’s price to last week’s – they’re comparing it to what they used to pay before “everything got expensive.” That reference point, even if outdated, sticks. When a block of cheese crosses the £3 mark, it doesn’t matter if it’s only a 5p rise – it’s crossed an invisible line. And that line reshapes everything around it.

Mental accounting adds another layer. People are rebalancing invisible budgets in their heads. Spend £2 more on milk, and that £2 has to come from somewhere else. They’re not just making trade-offs – they’re making calculations. Essentials stay, extras go, and even mid-tier items are under scrutiny if there’s a cheaper equivalent close by.

Then there’s price perception. It’s not what something costs – it’s what it feels like it should cost. That’s why a 10% rise might barely dent volume in one category but trigger a collapse in another. It’s not rational, but it’s real – and it’s guiding what goes in the basket.

For retailers and brands, this moment demands more than sharper pricing. It requires fluency in how shoppers frame value. That might mean pricing just below emotional thresholds or structuring offers that signal stability – even when costs are climbing. In this climate, perception can be as powerful as reality.

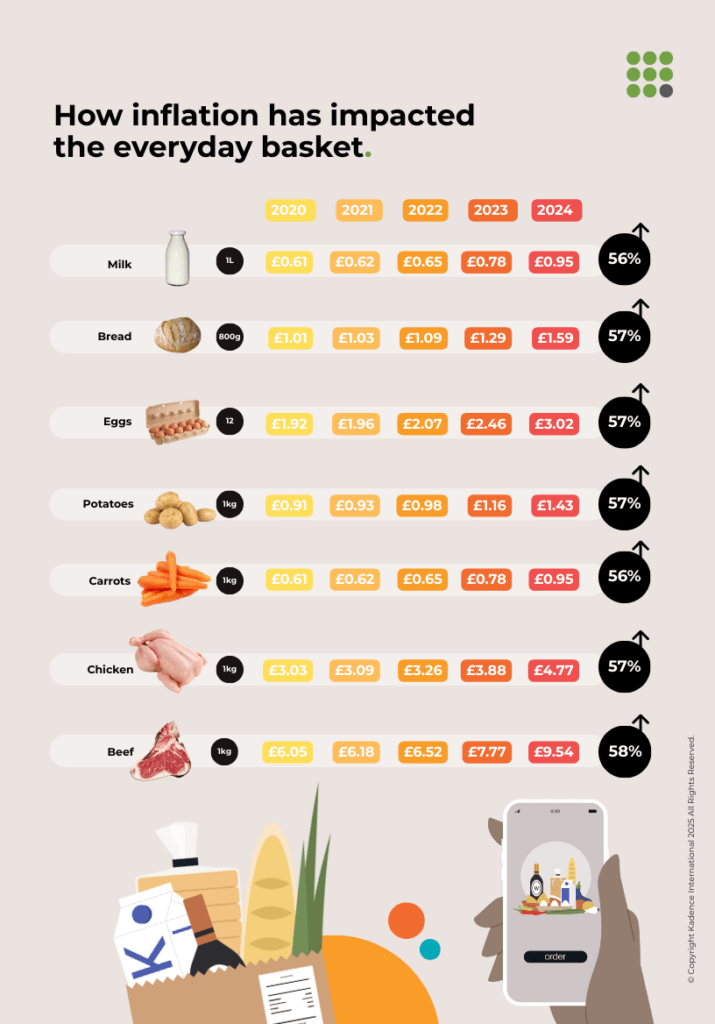

What does inflation feel like in real terms? The chart below shows just how much everyday items have risen since 2020.

Brand Erosion in the Era of the Basket Reboot

Brand loyalty isn’t dead – but it’s under review. Across the UK, what once felt automatic is now under scrutiny. Shoppers are looking at familiar labels, hesitating, and reaching for something cheaper – often store-brand, often good enough.

It’s not just trading down. It’s trading out. The basket reset happening now is exposing which brands still hold meaning and which were riding on habit. In categories like cereal, canned goods, and pasta sauces, private label has moved from backup plan to first choice. When shoppers feel squeezed, brand preference isn’t about awareness – it’s about justification.

The most vulnerable brands are the ones that rely on shelf presence and recognition without clearly articulating why they cost more. A fancy label or nostalgic logo doesn’t hold up when the price delta is visible, and the value isn’t. Own-label is no longer the compromise – it’s the baseline.

Supermarkets know this. That’s why they’ve built out three-tiered private label strategies: essential ranges for price-sensitive shoppers, core lines that match national brands on quality, and premium sub-brands designed to compete with legacy products on both taste and packaging. In many cases, they’re winning on all three fronts.

Branded suppliers are feeling the squeeze. Promotions are being pulled. Negotiations are tighter. Some products are being delisted entirely as retailers prioritise margin and private-label growth. Even in higher-margin categories like snacks and beverages, shoppers are experimenting more – and defaulting less.

This moment demands more than marketing. It demands a proposition that holds up under pressure. Brands that offer clear functional benefits – whether that’s health, sustainability, or convenience – still earn a place. But those that relied on emotional inertia are being quietly swapped out, one basket at a time.

The question for consumer goods companies isn’t just how to defend share. It’s how to rebuild relevance. Because if shoppers are open to changing their habits, they’re also open to forgetting the brands that no longer reflect how they want to spend.

Frugality has rebranded itself – and fast. What used to be framed as a necessity or even a source of quiet shame has become a signal of control, intention, and in many cases, pride. The UK’s cost-of-living pressures have given rise to a new kind of grocery shopper: not just cost-conscious, but value-literate.

This isn’t driven solely by economics. It’s cultural. Discount shopping has moved out of the shadows and into the spotlight. TikTok is full of haul videos not from high-end retailers, but from Aldi and Lidl – highlighting bulk buys, dupes, and smart swaps. The tone isn’t apologetic. It’s instructional. Look what I saved. Look how much farther I stretched my budget. There’s a certain confidence in the captions: “You’d be mad to pay more.”

Digital tools have amplified the shift. Couponing, once a paper-based pursuit of extreme savers, has gone mobile and mainstream. Apps like Too Good To Go and supermarket loyalty platforms now offer real-time deals that reward flexibility, not just spending. Younger shoppers – especially millennials with families and Gen Z renters – are building grocery strategies around digital offers and flash pricing. Price matching isn’t a race to the bottom; it’s a form of skill.

What’s changed is the identity that surrounds all this. Saving money used to imply you didn’t have it. Now, it implies you’re informed. Especially among middle-income shoppers, there’s been a quiet erosion of stigma. Being a “deal hunter” no longer contradicts being design-conscious or health-focused. You can buy the store-brand canned tomatoes and still splurge on artisanal olive oil. You can track every penny and still care about the story behind your coffee.

This hybrid mindset – blending thrift and selectivity – is what many legacy brands are still struggling to read. Their customers didn’t disappear. They just rewrote the rules of what makes a product worth paying for.

It’s no longer enough to assume aspiration equals premium. In this landscape, brands have to justify every line of the receipt. They need to speak the language of value – but not just through lower prices. It’s about usefulness, quality, longevity, and emotional return on spend.

Smart shoppers aren’t waiting for brands to get it. They’re building baskets that reflect who they are now – pragmatic, digitally fluent, and empowered by information, not overwhelmed by it. The question isn’t whether this shift will last. It’s whether brands can keep up with customers who’ve stopped equating value with volume – and started defining it for themselves.

Retailers Rewrite the Rules

Retailers have stopped waiting for shoppers to come back to old habits. Instead, they’re adapting to new ones – fast. The traditional promotional cycle, once built around limited-time offers and seasonal spikes, has been replaced by something more fundamental: proving long-term value in real-time.

That shift is showing up everywhere. Tesco’s Clubcard Prices and Sainsbury’s Nectar Prices have moved from reward mechanics to central pricing strategies. What began as a loyalty tactic is now a core part of how these retailers compete with discounters. And it’s not just about price. It’s about visibility. Price tags on shelves now tell a story of what the customer is saving, not just spending.

Even premium grocers are adjusting. Waitrose, long associated with quality-first positioning, has expanded its Essentials range and emphasised value messaging in advertising. Its recent campaigns have spotlighted affordability without abandoning tone, suggesting that smart shopping doesn’t have to mean compromise.

But nowhere is the shift more aggressive than in private label. Across the sector, own-brand lines have become the innovation lab. Aldi and Lidl continue to lead, not just with price, but with product development that mirrors – and sometimes beats – national brands. The battleground isn’t just about matching flavor or format anymore. It’s about convenience, sustainability, and shopper emotion. A well-packaged ready meal that costs less and feels like a small win at the end of a long day? That’s more powerful than a deep discount.

Retailers are also experimenting with format. Smaller footprint stores are popping up in urban areas, designed around the grab-and-go shopper who wants efficiency, not abundance. Meal deals, shoppable recipes, “value hacks” – all of it engineered to speak the new shopper’s language: stretch, save, simplify.

Marketing has evolved in step. Circulars and point-of-sale have been replaced by in-app push notifications, hyper-local personalisation, and digital shelves that highlight time-sensitive offers. Messaging is less about indulgence and more about empowerment. You’re not just saving money; you’re being smart. You’re beating the system.

The result is a retail environment where success no longer comes from a breadth of range or deepest pockets. It comes from relevance – knowing who your customer is today, what trade-offs they’re willing to make, and how to meet them with the right balance of function, emotion, and frictionless value.

Case Study: How Aldi Became the Benchmark for Value With Purpose

Aldi’s rise in the UK has long been tied to price, but its current momentum speaks to something deeper: cultural relevance. While many retailers are reacting to consumer caution, Aldi has anticipated it – shaping not just how people shop but also how they think about spending.

Its private label dominance is no longer just about cost-cutting. Aldi has invested heavily in product development and packaging design that challenges branded equivalents, often earning accolades in blind taste tests. Shoppers aren’t settling – they’re discovering. Categories like wine, ready meals, and snacks now generate loyalty not as substitutes, but as preferred choices.

Where Aldi’s strategy truly stands out is in how it aligns with emerging shopper identity. The brand doesn’t apologise for low prices. It builds pride around them. Recent campaigns have leaned into humor and confidence, casting Aldi customers as smart, in-the-know shoppers rather than bargain hunters. The brand’s “Like Brands. Only Cheaper.” messaging isn’t defensive – it’s disruptive.

In-store, Aldi’s stripped-back format reinforces that every inch of shelf space must earn its keep. The tight range, fast checkout model, and curated promotions reflect a retailer that understands time, budget, and simplicity as core values – not just marketing points.

Aldi isn’t winning by chasing premium. It’s winning by reshaping what premium means in the mind of today’s value-driven consumer.

What Comes Next for Grocery, Brand Building, and British Retail

This isn’t just a cycle – it’s a structural shift. The current realignment in UK grocery is forcing a deeper redefinition of how brands are built, how value is communicated, and what kind of loyalty can actually be sustained in a low-growth, high-scrutiny environment.

The old model – premium equals quality, discount equals compromise – has fractured. What’s rising in its place is a hybrid mindset: shoppers who blend store brands and branded goods, who track savings as a personal KPI, and who want clarity in place of clutter. For brands and retailers, the challenge is no longer just about margin. It’s about meaning.

Products will still matter – but the story around them matters more. Why this? Why now? Why at this price? The brands that survive won’t just be better stocked or better known – they’ll be better understood. That means strategy rooted in real consumer behaviour, not assumptions. It means investing in insight before investing in shelf space.

We’ve entered an era where margins are thinner, decisions faster, and the consumer’s tolerance for noise almost nonexistent. The winners will be those who can decode the mindset behind the spend – what drives trust, what cues value, what kills interest – and adapt before the data shows up in declining sales.

For British retail, this could be a renaissance moment. But it will favor the precise, not the broad. Those who treat their audience as a living, evolving signal – not a static segment – those who invest in listening as much as launching.

Because the real growth ahead won’t come from pushing more into baskets. It will come from knowing what truly earns a place there.

A Market Redefined by Value Will Reshape the Industry

What’s happening in UK grocery right now isn’t a blip. It’s a reset. A recalibration of trust, relevance, and what constitutes a purchase worth making.

For brands, the margin for error has collapsed. Shoppers are not just selective – they’re strategic. They aren’t waiting to be impressed. They’re asking harder questions: Is this worth it? Is this credible? Does it deliver more than just a label?

Retailers that respond with nuance – not just price cuts – are the ones shaping the future. The discounter isn’t the disruptor anymore; it’s the new center of gravity. Traditional grocers that once competed on scale or loyalty must now compete on understanding. That means fewer assumptions, more clarity, and a sharper grasp on how value is perceived – not just priced.

Consumer behaviour isn’t snapping back. Once a shopper has built a new mental model of spending – one grounded in empowerment, not deprivation – it tends to stick. The post-abundance era doesn’t signal a withdrawal from consumption. It signals a new consciousness around it.

Over the next five years, British retail will be defined not by who shouts the loudest but by who listens best. That requires precision, pattern recognition, and real, ongoing intelligence on the evolving expectations of the people pushing the trolleys.

Smart brands won’t just ride this out. They’ll use it to rebuild better – on foundations that reflect today’s shopper, not yesterday’s playbook.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

In 2005, Nintendo was teetering on irrelevance in the UK. Once a dominant force, the gaming giant had been eclipsed by Sony’s PlayStation and Microsoft’s Xbox, holding a mere 5% market share in a space increasingly dominated by high-powered consoles and competitive gaming. Gaming had become synonymous with young, tech-savvy male audiences – a niche where Nintendo no longer held sway.

Within two years, Nintendo executed a turnaround that defied industry norms. By 2007, its UK market share had skyrocketed to 80%, driven by a marketing strategy that ignored the industry’s obsession with specs and focused on accessibility, playfulness, and the redefinition of what it meant to be a “gamer.” The Nintendo DS and Wii weren’t just consoles; they were cultural phenomena that expanded the gaming audience beyond teenage boys and esports enthusiasts to parents, professionals, and an emerging market now known as kidults – adults who engage in play-driven, nostalgic, and social entertainment.

This wasn’t just a comeback. It was a masterclass in market expansion, consumer behaviour, and brand reinvention. Nintendo didn’t just take back its position in gaming – it transformed the industry’s entire trajectory. How did they do it? And what lessons can today’s brands learn from this seismic shift?

The Market Landscape Before Nintendo’s Comeback

By the mid-2000s, gaming was a high-stakes, high-performance industry. Sony and Microsoft were in an aggressive race, pushing cutting-edge graphics, processing power, and online multiplayer experiences. The PlayStation 2 was the undisputed king, selling over 155 million units globally, while the Xbox, backed by Microsoft’s deep pockets, had secured a loyal base of hardcore gamers. Nintendo, once the industry’s dominant force, had been relegated to an afterthought.

The problem? The market had narrowed. Gaming had become a battlefield of tech specs and realism, catering to an increasingly insular demographic – young male gamers. The industry had overlooked a fundamental truth: entertainment isn’t just about cutting-edge technology; it’s about accessibility, emotional connection, and cultural relevance.

This was the opportunity Nintendo saw before anyone else. Instead of competing on hardware power, the company pivoted toward a different gaming experience, prioritising intuitive gameplay, social engagement, and an audience that had been ignored for too long.

Nintendo engineered one of the most dramatic turnarounds in business history by rejecting the industry’s fixation on complexity and high-performance specs. Its strategy didn’t just reclaim market share – it reshaped the gaming landscape, expanding the definition of who a gamer could be.

Key Strategies That Fueled Nintendo’s Success

Nintendo’s comeback wasn’t a fluke – it was a deliberate strategy that defied industry norms. While Sony and Microsoft escalated the hardware arms race, Nintendo redefined what gaming could be. Instead of emphasising specs, it broadened its audience and made gaming more intuitive, turning the conversation from power to play.

#1. Expanding the Audience Beyond Gamers

Gaming had long been marketed to young men obsessed with high-speed, high-performance play. Nintendo shattered this mould by targeting demographics the industry had ignored: families, women, and older adults. The company understood gaming wasn’t inherently niche; it had simply been positioned that way.

The strategy was simple but groundbreaking: the barriers stopping non-gamers from picking up a controller. The Wii and Nintendo DS were designed to be intuitive, eliminating the intimidating learning curves of traditional gaming. This wasn’t about mastering complex button combinations or navigating hyper-realistic battlefields; it was about play.

Nintendo’s marketing leaned into this accessibility, positioning gaming as a shared experience rather than a solo, skill-based pursuit. Instead of hyper-stylised action sequences, Nintendo’s ads featured families playing together in living rooms, grandparents competing with grandchildren, and social settings where gaming wasn’t just entertainment; it was connection.

The result? Nintendo didn’t just win back players – it created millions of new ones. This wasn’t just about reclaiming dominance; it was about reshaping the gaming audience entirely.

#2.Leveraging Innovative Gameplay Experiences

Nintendo’s resurgence wasn’t about cutting-edge graphics, faster processors, or blockbuster storytelling. It was built on a simple yet powerful principle of consumer psychology: ease of use. By stripping away complexity, Nintendo made gaming more accessible than ever.

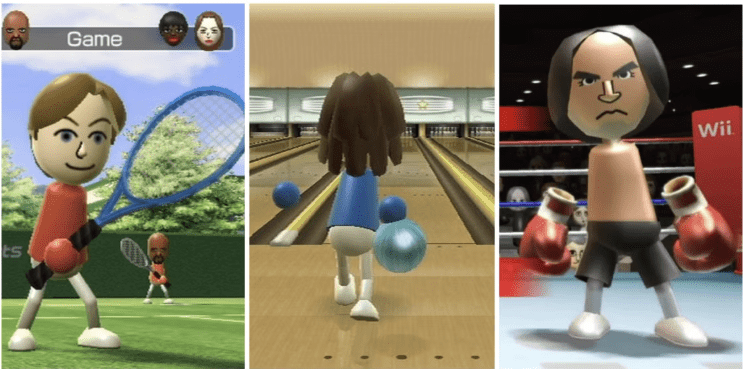

The Nintendo DS: A Touch-Based Revolution

It was built on a simple yet powerful principle of consumer psychology: ease of use. By stripping away complexity, Nintendo made gaming more accessible than ever.

Image Credit: Nintendogs Wiki Fandom

More importantly, Nintendo ensured the software supported this approach. Titles like Brain Age and Nintendogs weren’t designed for traditional gamers – they were built to attract a broader demographic, including older adults and casual players who had never picked up a console before. By moving away from conventional gaming tropes, the DS became a global sensation, selling over 154 million units.

The Wii: Motion-Control Gaming That Redefined Engagement

If the DS lowered the barrier to entry for handheld gaming, the Wii redefined accessibility in home entertainment. Launched in 2006, the Wii introduced motion-sensing controls that eliminated complex button inputs. Players could physically swing, punch, or steer their way through games, making gaming feel more interactive and immersive.

Image Credit: Game Rant

Bundling Wii Sports was a masterstroke. The Wii’s intuitive, motion-based gameplay made it essential for the living room, drawing in families, older adults, and social gamers. By 2007, the Wii had outsold the Xbox 360 and PlayStation 3.

Rather than competing in the high-performance gaming race, Nintendo carved out an entirely new segment – one that prioritised intuitive, inclusive, and social play. The company didn’t just win back market share; it expanded the definition of gaming itself.

#3. Creating a Software Lineup That Sold Consoles

Nintendo’s success wasn’t just about hardware innovation. The real driver behind the DS and Wii’s dominance was a software strategy that prioritised accessibility, engagement, and repeat playability. While competitors focused on high-budget, graphics-heavy blockbusters, Nintendo leaned into intuitive, universally appealing experiences that turned occasional players into loyal consumers.

The Power of Bundled Games

Few games have matched the cultural impact of Wii Sports. With simple motion controls for tennis, baseball, and bowling, Wii Sports turned gaming into an active, social activity. The result? It became one of the best-selling games of all time.

Similarly, Brain Age for the DS tapped into a new category of users: adults looking for cognitive challenges. Its premise, built around mental exercises and daily training, positioned the DS as a lifestyle product. This pivot expanded Nintendo’s consumer base and set the stage for future mainstream gaming trends.

Franchises That Defined an Era

Beyond bundled titles, Nintendo doubled down on its iconic IPs. Mario Kart DS brought the beloved racing franchise to handheld gamers, while New Super Mario Bros. revitalised classic platforming for a new generation. These titles weren’t just nostalgia-driven – they were strategically designed to leverage Nintendo’s strongest assets while remaining accessible to casual players.

Image Credit: The Gamer

The Wii also saw a boom in motion-driven exclusives. Games like Wii Fit turned the console into a fitness tool, targeting a demographic far beyond traditional gamers. This content diversification ensured Nintendo wasn’t just selling consoles; it was building long-term engagement.

Image Credit: Game Stop

By focusing on intuitive gameplay, evergreen franchises, and software that appealed to untapped markets, Nintendo created a virtuous cycle: every best-selling game drove more console sales, and every console sale expanded the audience for future games. This strategy transformed Nintendo from an industry underdog to a market leader once again.

#4. Making Gaming More Affordable and Accessible

While Sony and Microsoft were engaged in a hardware race, pushing consoles with advanced graphics and premium pricing, Nintendo took a different approach. It focused on affordability, positioning the DS and Wii as low-cost, high-value alternatives that didn’t require a deep investment in gaming culture or expensive accessories. This pricing strategy wasn’t just about undercutting the competition; it was about lowering the barrier to entry and widening the consumer base.

Disrupting the Price War

In 2006, the PlayStation 3 launched at £425 in the UK, while the Xbox 360 ranged from £209 to £279. The Nintendo Wii, by contrast, entered at just £179—an accessible price point that made it an easy choice for families, casual gamers, and first-time buyers long priced out of gaming.

The DS followed a similar model. At launch, it was significantly cheaper than Sony’s handheld PSP, which was marketed as a high-performance portable console with multimedia capabilities. While the PSP struggled to compete with the rise of smartphones in the years ahead, the DS thrived by staying true to its core audience – offering simple, engaging experiences at a price point that felt accessible.

The Cost-to-Value Proposition

Price alone wasn’t enough – Nintendo had to prove value. Bundling Wii Sports gave consumers an instant reason to buy, eliminating the need for additional purchases. The Wii’s motion controls also removed the expense of extra accessories. Meanwhile, the DS thrived on a library of budget-friendly, mass-appeal titles, positioning gaming as an everyday activity rather than a luxury.

This affordability-first strategy had long-term implications. It cultivated a new generation of casual gamers, many of whom might never have considered purchasing a console. More importantly, it reinforced Nintendo’s reputation as the most accessible gaming brand, not just competing for market share but actively expanding the market.

By rejecting the premium-price model and focusing on mass-market adoption, Nintendo proved that success in gaming wasn’t just about hardware specs; it was about making gaming available to everyone.

#5. A Marketing Masterclass in Consumer Engagement

Nintendo’s comeback wasn’t just about hardware, software, or pricing – it was about storytelling. While Sony and Microsoft marketed gaming as a high-performance, immersive experience for dedicated players, Nintendo positioned gaming as something entirely different: a social, intuitive, and universally accessible activity. This shift in messaging was a fundamental repositioning of what gaming meant to consumers.

The Shift from Power to Play

Sony’s PlayStation 3 campaign emphasised its powerful hardware, with cinematic trailers showcasing hyper-realistic graphics and advanced processing power. Microsoft’s Xbox 360 leaned into its online gaming ecosystem, targeting hardcore players with a focus on multiplayer capabilities.

Image Credit: Miscrave

Nintendo went in the opposite direction. It didn’t market specs – it marketed people. Instead of high-adrenaline gameplay, its ads showed families, grandparents, and first-time gamers picking up a Wii remote and playing instantly. The message was clear: gaming wasn’t just for gamers anymore.

Turning Gaming into a Shared Experience

The Wii Would Like to Play became one of the era’s iconic marketing campaigns. Featuring two suit-clad Japanese men introducing the Wii to everyday households, it emphasised invitation over exclusivity. Nintendo wasn’t selling a console; it was selling interaction, laughter, and inclusion.

For the DS, Nintendo leaned into relatability. The Touch Generations campaign targeted non-gamers, featuring celebrities and everyday users engaging with brain-training games, puzzle titles, and social experiences. This wasn’t gaming for the elite; it was gaming for everyone, reinforcing the company’s core strategy of mass accessibility.

Retail Strategy and Experiential Marketing

Beyond traditional advertising, Nintendo excelled at experiential marketing. The company rolled out widespread in-store demo stations, allowing hesitant buyers to try the Wii’s motion controls or experience the DS’s touchscreen before making a purchase. This hands-on approach eliminated scepticism and turned a casual interest into immediate conversion.

Nintendo also capitalised on the rise of social proof. Word-of-mouth marketing skyrocketed as the Wii became a staple in living rooms worldwide. The more people saw their friends and family engaging with Nintendo products, the more likely they were to join in, creating a viral effect that fueled record-breaking sales.

By shifting its marketing from performance-driven specs to emotion-driven engagement, Nintendo didn’t just sell consoles – it sold experiences. In doing so, it reshaped the gaming industry, proving that success wasn’t about catering to the existing market but creating an entirely new one.

#6. The Long-Term Impact on Gaming and Consumer Behavior

Nintendo’s strategy didn’t just reclaim market share – it redefined gaming itself. It shifted perceptions of who a “gamer” could be and expanded what gaming could offer. The ripple effects went beyond Nintendo, reshaping the industry and consumer expectations for years.

Mainstreaming Casual and Social Gaming

Before the Wii and DS, gaming was a niche hobby dominated by young men. Nintendo shattered that perception, proving gaming could be inclusive, social, and effortless. The runaway success of Wii Sports, Brain Age, and Nintendogs sparked demand for intuitive, accessible gameplay – paving the way for mobile gaming’s rise.

Nintendo inadvertently set the stage for the mobile gaming revolution by lowering the entry barrier and emphasising fun over complexity. The App Store, launched in 2008, followed the same principles: games that were simple to learn, easy to access, and designed for mass appeal. Today, the global mobile gaming market generates more revenue than console and PC gaming combined, a shift that can be traced back to Nintendo’s strategy of broadening the gaming audience.

The Legacy of Motion Controls and Interactive Gaming

Initially dismissed as a gimmick, the Wii’s motion controls became a blueprint for interactive gaming. Microsoft’s Kinect and Sony’s PlayStation Move were direct responses, chasing the demand Nintendo had created. More significantly, the idea of physical engagement in gaming extended beyond consoles – AR and VR gaming owe much of their mainstream appeal to Nintendo’s early innovations.

Image Credit: Nintendo

Nintendo’s focus on intuitive play also influenced how developers approached game design. Today, user-friendly mechanics and immediate engagement are central to many of the industry’s best-selling titles, from fitness-based games like Ring Fit Adventure to the continued success of Just Dance, a franchise built on motion-based play.

A Blueprint for Market Expansion

Nintendo’s greatest lesson wasn’t reclaiming market share – it was creating new demand. Rather than competing in a saturated market, it identified an untapped audience and built products around them.

This strategy continues to influence modern gaming. The resurgence of retro consoles, the rise of cloud gaming services that prioritise accessibility over hardware power, and even the success of games like Animal Crossing: New Horizons – which attracted a massive non-traditional gaming audience – can all be linked to the blueprint Nintendo established in the mid-2000s.

Nintendo didn’t just revive its brand – it reshaped the gaming industry. By proving that innovation comes from creating trends, not following them, it set a new standard for market disruption. And its influence didn’t stop at gaming.

Nintendo’s resurgence wasn’t just a corporate turnaround; it redefined how entertainment itself was consumed. By shifting gaming from a skill-based pursuit to a social, inclusive experience, it expanded the industry’s reach far beyond its traditional audience. The DS and Wii weren’t just successful consoles; they were cultural phenomena that reshaped consumer behaviour, fueled the rise of casual gaming, and set the stage for today’s interactive entertainment trends.

The takeaway for brands? Market dominance isn’t about competing harder – it’s about expanding the playing field. Nintendo succeeded by challenging assumptions, identifying unmet consumer needs, and making gaming effortless and engaging. It didn’t just reclaim leadership; it shaped the future of digital entertainment for decades.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Streaming is no longer an emerging trend – it has firmly established itself as the dominant mode of entertainment. Yet, how people stream content varies significantly by region and generation. While the US, UK, and Southeast Asia all favour on-demand viewing, regional and demographic nuances are shaping the next phase of the industry.

In the US, streaming now accounts for 43% of total TV consumption – more than double its share from a few years ago. However, subscription fatigue is rising, with nearly one-third of consumers cancelling at least one service in the past year. As a result, ad-supported models are gaining ground, providing brands with new ways to reach audiences moving away from traditional paid subscriptions.

In the UK, live TV’s decline is accelerating, particularly among younger viewers. In 2023, fewer than half of 16-24-year-olds watched live television weekly. As streaming overtakes traditional viewing, Netflix has pulled ahead of BBC1 in total audience reach. The demand for locally produced content remains strong, prompting global platforms to increase investment in British programming to retain subscribers.

In Southeast Asia, a mobile-first approach defines the streaming landscape, with over 90% of users accessing content via smartphones. This preference fuels a strong demand for locally produced content, often surpassing global franchises in popularity. Live streaming, frequently combined with e-commerce, has emerged as a significant engagement tool, allowing consumers to interact with sellers in real-time. Additionally, the region is at the forefront of AI-driven content recommendations, as platforms utilise advanced algorithms to enhance user experiences.

Streaming preferences vary significantly across generations. Gen Z and Millennials gravitate towards short-form, socially-driven content, with platforms like TikTok and YouTube being particularly popular. In contrast, Gen X and Baby Boomers lean towards longer, ad-free viewing experiences, often favouring traditional television and subscription-based streaming services. Despite these differences, binge-watching is a common behaviour across all age groups. Notably, younger viewers are increasingly engaging with interactive content, reflecting their desire for more immersive experiences.

The Rise of Streaming and the Decline of Traditional TV

The shift from traditional television to streaming is now undeniable, reshaping how audiences consume content across global markets. While linear TV still holds relevance in certain demographics, the numbers tell a different story:

In the US, streaming accounts for 41.6% of total TV consumption, with cable and broadcast TV dropping below 50% for the first time.

In the UK, Netflix has surpassed BBC1 in total viewership, a milestone that signals a permanent shift toward on-demand content.

In Southeast Asia, 71% of TV viewers now consume ad-supported streaming, putting digital platforms on par with traditional television in the region.

This shift isn’t just about technology – it’s about consumer behaviour. Audiences today demand flexibility, personalisation, and content tailored to their interests, leaving behind the rigid schedules of linear programming. Younger viewers, in particular, are turning away from appointment-based TV, opting instead for platforms that provide immediate, algorithm-driven recommendations.

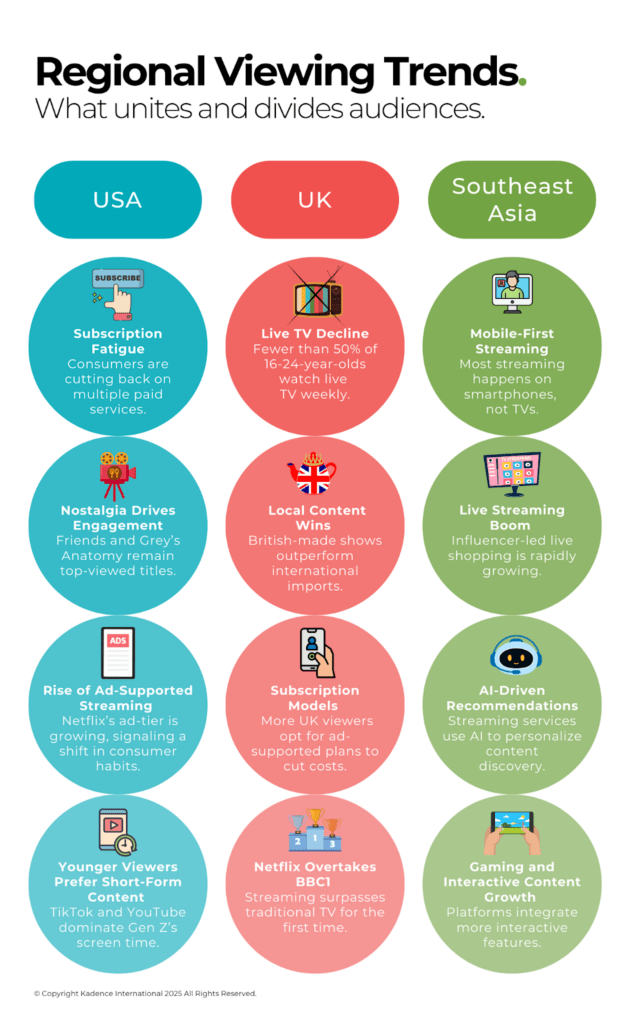

Regional Viewing Trends: What Unites and Divides Audiences?

Streaming trends vary widely across regions, influenced by cultural preferences, technological access, and economic factors. While some viewing habits are universal, key differences reinforce the need for region-specific content and marketing strategies.

United States

In the US, subscription fatigue is reshaping streaming habits. While platforms dominate TV consumption, 42% of users feel overwhelmed by too many choices, and nearly half plan to cancel at least one service. This has accelerated the shift to ad-supported tiers, with 39% of Netflix’s new subscribers opting for its lower-cost, ad-backed plan.

To counteract subscription fatigue and attract cost-conscious viewers, streaming platforms are increasingly embracing ad-supported models. The success of these tiers signals a growing consumer preference for lower-cost options over premium, ad-free experiences.

Image: Grey’s Anatomy

Despite the surge in new content, licensed shows continue to dominate streaming viewership. In 2024, Grey’s Anatomy ranked as the second most-watched streaming program, amassing 47.85 billion minutes viewed across Hulu and Netflix. Friends remains a staple on streaming platforms, while classic titles like The Big Bang Theory and Little House on the Prairie also saw significant engagement. The sustained popularity of older programs highlights the enduring appeal of nostalgia-driven content and the power of deep, long-running libraries.

United Kingdom

The UK’s youngest viewers are turning away from live TV, with less than half of 16-24-year-olds watching it weekly. Streaming platforms have stepped in to capture this audience, and Netflix now commands a larger share of viewership than BBC1. Meanwhile, investment in British-made productions is driving subscriptions, reinforcing the appeal of localised content.

A strong preference for locally produced content continues to shape the UK streaming market. Platforms are responding with increased investment in British programming, recognising its role in retaining subscribers and differentiating services in a competitive landscape.

Ad-supported streaming is also gaining momentum, offering cost-conscious viewers an alternative to rising subscription fees. For advertisers, this shift creates new opportunities to engage audiences within premium, on-demand environments.

Image: Mr Bates vs The Post Office

In 2024, several television programs captured the attention of UK audiences, reflecting diverse viewing preferences. Mr Bates vs The Post Office became the most-watched program of the year, drawing nearly 14 million viewers on ITV. Meanwhile, American sitcoms continue to dominate streaming, with The Big Bang Theory topping charts at 63.1 million views, followed by Friends with 55.8 million views. Netflix’s Black Doves, a recent release, amassed 57.7 million views, demonstrating the platform’s ability to drive audience engagement. These trends highlight the UK’s dual appetite for homegrown dramas and globally recognised franchises, reinforcing the importance of a diverse content library for streaming platforms.

Southeast Asia

Mobile streaming dominates Southeast Asia, where most viewers watch content on smartphones rather than TVs. Unlike Western markets, where streaming services compete for subscription revenue, free-to-watch and ad-supported content drive engagement, with AI-powered recommendations shaping viewing habits.

Local and regional content dominates viewer preferences, with audiences favouring stories and characters that resonate with their own experiences. This demand has spurred a surge in locally produced content, catering to the diverse linguistic and cultural landscape of the region.

Live streaming and social commerce are reshaping the entertainment paradigm. Platforms are increasingly integrating shopping features into live broadcasts, creating interactive experiences that blend entertainment with e-commerce.

Artificial intelligence is playing an influential role in content recommendations, enhancing user engagement by tailoring suggestions to individual viewing habits. This personalisation fosters deeper connections between viewers and platforms, driving sustained engagement.

Collectively, these regional trends highlight the multifaceted nature of the global streaming ecosystem. While certain viewing habits transcend borders, nuanced differences underscore the necessity for brands and content creators to adopt region-specific strategies to effectively engage diverse audiences.

Image: Vikram Vedha

Southeast Asia’s top content reflects the region’s diverse tastes and growing demand for localised programming. In 2024, the highest-grossing show on Netflix was Vikram Vedha (a hit in Indonesia and Thailand), racking up 45 million views in just one month. Korean dramas are also a key driver, with Crash Landing on You earning 58 million views across Southeast Asia, highlighting the region’s preference for international content that still feels locally relatable. Meanwhile, Indonesian dramas like Tiga Dara saw a surge, with 20 million views on local streaming platforms like GoPlay. This shows the growing need for platforms to balance global hits with region-specific content.

The Generational Divide in Streaming Habits Gen Z and Millennials

Streaming habits are deeply shaped by generational preferences, with younger audiences favoring social-driven, short-form content, while older viewers remain loyal to traditional long-form programming.

Gen Z and Millennials

Gen Z and Millennials consider streaming an extension of their digital ecosystem, where content is discovered through social media platforms like TikTok and YouTube, not traditional TV guides. Their preferences lean toward short-form, algorithm-driven entertainment, emphasising speed, interactivity, and shareability. The rise of gaming-integrated streaming further caters to their desire for immersive, participatory experiences.

Gen X and Baby Boomers

Gen X and Baby Boomers gravitate toward long-form content, including feature films and multi-season TV series. They prioritise ad-free experiences, choosing premium streaming options over ad-supported models. Nostalgia drives their content choices, as they revisit classic shows and familiar genres instead of new releases. Unlike younger audiences, they prefer a slower pace, showing more loyalty to scheduled programming and series they can follow over time.

The Universality of Binge-Watching

Binge-watching transcends generational divides, becoming a common behaviour across all age groups. 72% of TV viewers report watching at least three episodes in one sitting, showing that while content preferences may differ, the desire for extended viewing sessions is universal.

The Future of Streaming: What the Numbers Predict

The future of streaming is being shaped by three key trends: AI-driven content discovery, the rise of ad-supported tiers, and a growing focus on live content. As audiences increasingly demand personalisation, affordability, and real-time engagement, platforms that fail to keep pace risk losing relevance.

The Growing Role of AI in Shaping Recommendations

Artificial intelligence is playing an increasingly vital role in streaming platforms, driving personalised content recommendations. Netflix, for instance, attributes 80% of viewer activity to its AI-driven recommendations, a strategy that is estimated to save the company $1 billion annually in customer retention.

Amazon Prime Video is also exploring AI through its “AI Topics”, which curates content categories based on individual interests, offering a more tailored and intuitive content discovery experience.

The Rise of Hybrid Models

In response to diverse consumer preferences, many streaming services are adopting hybrid monetisation models that blend subscriptions with ads. Disney+, Netflix, and Amazon Prime have launched ad-supported tiers, providing more affordable options for viewers while expanding revenue streams.

This approach seeks to balance user experience with profitability, accommodating both ad-tolerant and ad-averse audiences.

Increased Investment in Regional Content

Streaming giants are investing heavily in regional content to better engage local audiences and strengthen their subscriber base. By producing and promoting local programming, platforms can build deeper connections with viewers, enhancing loyalty. This approach not only broadens their subscriber base but also enriches the global content library with diverse cultural narratives.

Streaming’s Push into Live Sports and Event-Based Content

Streaming services are increasingly venturing into live sports and event-based programming, capitalising on the enduring appeal of real-time content. Netflix, for example, is exploring opportunities in live sports and video games, aiming to diversify its offerings and attract a wider audience.

This shift signals a move toward more immediate and dynamic content, challenging traditional broadcast models.

Impact of Hollywood’s Production Slowdown

Hollywood’s production slowdown is beginning to affect streaming platforms, leaving fewer new titles for viewers accustomed to a steady flow of fresh content. As a result, platforms must turn to diversified content strategies, such as investments in international productions and alternative programming, to keep subscribers engaged during periods of limited new releases.

What This Means for Brands and Marketers

For brands, streaming’s evolution presents both challenges and opportunities. Success hinges on market research, allowing companies to tailor content and advertising to shifting viewer behaviours.

The Importance of Streaming Data for Audience Segmentation

Streaming platforms generate vast amounts of data, offering insights into viewer behaviours, preferences, and engagement patterns. By analyzing this data, brands can segment audiences more precisely, tailoring content and advertisements to specific demographics and viewing habits. This targeted approach enhances marketing efficiency by directing efforts toward the most receptive audience segments.

Adapting Media Strategies to Shifting Viewing Habits

As consumer viewing habits evolve, brands must adjust their media strategies accordingly. The decline of traditional television and the rise of on-demand streaming necessitate a reevaluation of advertising channels. Investing in streaming platforms, particularly those offering ad-supported models, allows brands to reach audiences where they are increasingly spending their time. Additionally, understanding peak viewing times and content preferences can inform the timing and placement of advertisements, maximising impact.

Crafting Platform-Specific Content

Different streaming platforms cater to varied audience preferences and content formats. For instance, TikTok thrives on short-form, viral content, while platforms like Netflix and YouTube accommodate longer-form videos. Brands should develop platform-specific content strategies, ensuring that the style, length, and messaging align with the expectations of each platform’s user base. This approach not only enhances engagement but also demonstrates an understanding of the platform’s culture and audience.

Leveraging Influencers to Drive Engagement

Influencers play a pivotal role in shaping viewer perceptions and driving engagement on streaming platforms. Collaborating with influencers who resonate with target audiences can amplify brand messages and foster trust. These partnerships can take various forms, including sponsored content, product placements, or co-created material. Given influencers’ ability to authentically connect with their followers, such collaborations often result in higher engagement rates compared to traditional advertising methods.

Exploring Opportunities in Interactive Content and Partnerships

Interactive content, such as polls, quizzes, and live Q&A sessions, encourages active audience participation, leading to deeper engagement. Brands can integrate interactive elements into their streaming content to create immersive experiences that captivate viewers. Additionally, forming partnerships with content creators or streaming platforms can provide access to new audiences and innovative content formats. For example, collaborating on exclusive content or sponsoring popular series can enhance brand visibility and association with high-quality programming.

Adapting to Changing Audience Behaviors

As streaming platforms reshape how audiences consume media, brands are under pressure to respond to rapidly changing viewer behaviours. The era of broad, generalised marketing strategies is fading. Success now depends on brands’ ability to customise content and marketing to fit specific regional trends and audience demands. Those that effectively leverage data-driven insights and align their messaging with platform-specific cultures will be better positioned to build stronger relationships with consumers and stay ahead in a crowded and competitive market.

A New Era of Streaming Requires a New Playbook

The one-size-fits-all content strategy is dead. Brands that fail to localise, personalise, and diversify their streaming approach will be left behind. The future belongs to those who stop chasing trends—and start using market intelligence to shape them. Today, audience behaviour is shaped by regional preferences, generational divides, and technological disruption – forces that demand a more sophisticated, localised, and data-driven approach from brands and content creators.

For years, global entertainment operated on the assumption that content produced for one audience could seamlessly translate to another. That model no longer holds. The numbers tell the story – while US viewers remain captivated by nostalgia-driven programming, younger audiences in the UK are abandoning linear TV entirely, and Southeast Asia’s mobile-first users are redefining engagement through live streaming and AI-driven recommendations. If streaming platforms and brands fail to recognise these shifts, they risk becoming irrelevant in key markets.

Localisation Is No Longer Optional

Local content is no longer a niche offering – it is a competitive necessity. Global streaming giants are pouring billions into regional productions because they have seen the data: subscribers are more loyal to platforms that cater to their cultural and linguistic preferences. In Southeast Asia, hyper-local content consistently outperforms Western programming. In the UK, British-made series draw more sustained engagement than many high-budget imports. A global strategy must start with a deep understanding of audience preferences at the local level – a reality that only market research can fully capture.

Agility Is the Only Way Forward

Streaming is not just replacing television; it is fragmenting it beyond recognition. The rise of ad-supported tiers, the growing dominance of TikTok-style short-form content, and the push toward interactive programming all signal that consumer habits will continue to evolve at breakneck speed. The platforms and brands that succeed will not be those clinging to legacy strategies, but those that move fast, test often, and adapt constantly.

In this new era of streaming, the winners will not be those with the biggest budgets but those with the best insights. The days of assuming global audiences behave the same way are over. For brands and marketers, the only way forward is a strategy that is localised, data-backed, and built for change.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Volvo’s recent announcement to revise its ambitious plan for an all-electric lineup by 2030 has raised eyebrows across the automotive industry.

Instead of committing to a fully electric fleet, the company instead aims to “electrify” 90% of its vehicles, incorporating a mix of fully electric, hybrid, and plug-in hybrid models. This pivot begs the question: will it slow down the UK electric vehicle market?

The UK’s commitment to net-zero emissions by 2050 and the government’s ban on new petrol and diesel cars by 2030 have undoubtedly generated significant interest in EVs from consumers. However, widespread adoption still faces its challenges. Our research for automotive clients shows consumers struggle with several issues, including understanding EV technology, navigating charging infrastructure, and dealing with “range anxiety”—the fear of running out of power during a trip. Even smaller concerns, like the absence of traditional engine noise, have made potential buyers hesitant to make the switch.

These barriers and an evolving market signal that the road ahead for EV adoption in the UK requires more than innovative vehicles. It demands a comprehensive approach that addresses these consumer concerns and demystifies the EV experience. Automotive manufacturers must rethink their strategies, not just in terms of product offerings but also in how they engage and educate customers.

Identifying Key Barriers to EV Adoption in the UK

Understanding the Technology: A Daunting Learning Curve

Despite increased awareness, some consumers still feel ill-informed about EV technology. Many are uncertain about battery life, maintenance costs, and the differences in driving dynamics compared to internal combustion engine (ICE) vehicles. This knowledge gap is especially pronounced among older consumers and those less inclined to adopt new technologies. For these individuals, transitioning from a familiar ICE vehicle to an EV is not merely a financial decision but a significant cognitive shift.

Automakers must simplify this learning curve. Providing clear, jargon-free information and interactive tools, such as virtual simulations and augmented reality experiences, can help potential buyers more intuitively understand EV features and benefits. Educating consumers through immersive experiences will be crucial in transforming curiosity into confidence.

Charging Infrastructure: A Puzzle Yet to Be Solved

Despite the expansion, the UK’s charging infrastructure is still seen as inadequate.

According to EV Magazine, As of April 2024, the UK boasts 61,232 public EV charging points, representing a remarkable 53% increase from the previous year. However, this growth has not kept pace with the rising demand for EVs. The distribution of these chargers remains uneven, with urban areas well-served while rural regions lag. This disparity contributes to “range anxiety,” a significant psychological barrier that deters many potential EV buyers.

A more strategic approach is needed to address this. AI and machine learning can optimise the placement of new charging stations by analysing traffic patterns, vehicle usage, and energy demand. Moreover, dynamic pricing models managed by AI can incentivise off-peak charging, helping to balance the grid and reduce consumer costs.

Range Anxiety: The Psychological Hurdle

Beyond the physical constraints of charging infrastructure lies the psychological barrier of range anxiety. Despite advancements in battery technology, which have significantly improved the range of modern EVs to an average of 200-250 miles per charge, consumer perceptions lag behind reality. A 2023 survey by the Energy Saving Trust found that 65% of respondents still believe EVs couldn’t meet their daily driving needs. This disconnect underscores the power of consumer psychology, which can be as formidable a barrier as the technological limitations themselves.

Manufacturers can counteract these perceptions through transparent, real-world demonstrations of EV capabilities, such as long-distance road trips or live-streamed journeys that showcase the reliability and range of modern EVs. Additionally, offering extended test drives can help consumers experience the range and charging process first-hand, alleviating their concerns.

Lack of Engine Noise: A Sensory Barrier

For many drivers, the sound of a traditional engine is an integral part of the driving experience, providing auditory feedback that enhances the sense of control and connection to the vehicle. Though often seen as a benefit, the silence of EVs can feel disconcerting to drivers accustomed to the roar of a traditional engine. This lack of sensory input is more than a superficial concern; it affects the emotional connection and driving satisfaction for some consumers, particularly those in luxury segments.

To bridge this gap, several manufacturers are introducing artificial engine sounds that mimic traditional engines. Porsche’s “Electric Sport Sound” and BMW’s collaboration with composer Hans Zimmer to create a soundscape for their EV models are examples of how brands address this sensory barrier. These innovations help make EVs more appealing to drivers who miss the auditory cues of internal combustion engines while still highlighting the superior torque and acceleration characteristics of EVs, which can offer a thrilling experience akin to high-performance petrol vehicles.

Government Policies and Incentives Shaping the Future of EV Adoption in the UK

The UK government has set ambitious targets to phase out the sale of new petrol and diesel cars by 2030, but achieving these goals will require a robust framework of policies and incentives designed to support both consumers and the automotive industry.

Tax Incentives and Subsidies: One of the most effective ways to encourage EV adoption is through financial incentives. The UK government currently offers a plug-in car grant of up to £2,500 for eligible EVs, and EV buyers are exempt from paying vehicle excise duty. However, as the market matures, these incentives may need to be adjusted to maintain effectiveness. Implementing tax benefits for businesses that invest in fleet electrification and providing subsidies for home and workplace charging installations can further stimulate demand.

Investment in Charging Infrastructure: The government has pledged £1.3 billion to expand the charging network nationwide to support the growing number of EVs. This includes funding for rapid charging hubs on major motorways and investment in local on-street charging solutions for residential areas without off-street parking. A unified charging network, possibly regulated to ensure interoperability and standardised payment systems, will be essential to provide a seamless user experience.

These policies, combined with ongoing public awareness campaigns, will be critical in driving the widespread adoption of EVs and achieving the UK’s net-zero emissions goals.

Technological Advancements Transforming the UK EV Ecosystem

Emerging technologies like AI, machine learning, and blockchain are also set to revolutionise the UK EV ecosystem.

AI and Machine Learning for Optimised Infrastructure: By analysing traffic patterns, energy demand, and user behaviour, AI can help determine the optimal locations for new charging stations. This reduces congestion and improves the overall efficiency of the network. AI can also manage dynamic pricing to encourage off-peak charging, balancing grid demand and lowering costs.

Blockchain for Transparent and Secure Energy Trading: Blockchain technology can enable secure, transparent energy transactions between EV owners and the grid. Initiatives like Vehicle-to-Grid (V2G) technology allow EVs to act as decentralised energy storage units, feeding excess power back into the grid during peak demand periods. This not only provides EV owners with a new revenue stream but also helps stabilise the grid and integrate renewable energy sources more effectively.

These technological advancements can help the UK meet its electrification goals, creating a resilient and user-friendly EV ecosystem that addresses both current challenges and future demands.

Global Market Dynamics in the EV Sector

Globally, brands have successfully employed differentiated strategies to address the diverse EV market.

In the US, for example, Ford has capitalised on the brand equity of its iconic Mustang by launching the Mach-E, an electric SUV that leverages the Mustang’s heritage to appeal to traditional car enthusiasts while introducing them to electric mobility.

In contrast, in China, where the market is dominated by first-time car buyers and younger demographics, brands like NIO have focused on offering a premium, tech-centric experience complete with autonomous driving features and luxury interiors.

In the UK, brands may want to consider adopting a hybrid strategy, integrating insights from various global markets while tailoring their approach to local consumer sentiments. By doing so, they can better navigate the complexities of consumer behaviour, ensuring that no segment feels left behind in the shift toward electrification.

Strategic Recommendations for Automotive Brands

The transition to electric vehicles (EVs) presents a multi-faceted challenge that demands a strategic and consumer-centric approach.

Here are three key recommendations for automotive brands looking to refine their EV strategies, supported by verified examples from global markets:

#1. Develop Hybrid and Plug-In Hybrid Models as Transitional Products

The leap from internal combustion engine vehicles to fully electric vehicles can be too abrupt for many consumers. Hybrid and plug-in hybrid electric vehicles (PHEVs) are a valuable bridge, offering a mix of electric and traditional driving experiences. This strategy not only eases the transition but also addresses concerns such as range anxiety and charging infrastructure limitations.

Actionable Steps:

Expand Hybrid Portfolios: Brands should diversify their hybrid and PHEV offerings across vehicle segments, including sedans, SUVs, and luxury vehicles. This allows consumers to choose a hybrid model that fits their lifestyle and needs.

Emphasise Versatility and Convenience: Marketing campaigns should highlight the convenience of hybrids, such as the ability to switch between electric and gasoline power, which can alleviate range anxiety.

Example: Toyota’s success with the Prius, especially in the US market, illustrates the power of a well-positioned hybrid vehicle. The Prius launched as the world’s first mass-produced hybrid in 1997, has since become synonymous with hybrid technology. Its unique design and the introduction of Toyota’s Hybrid Synergy Drive system in 2004 helped it capture a significant market share by providing a distinct identity and strong performance. This strategy has been pivotal in making the Prius the best-selling hybrid worldwide, appealing to eco-conscious consumers and those looking for cost-effective driving options.

Source: Green Car Reports

2. Invest in Charging Infrastructure Partnerships to Ease Range Anxiety

A significant barrier to EV adoption is the perceived lack of reliable charging infrastructure. While governments and private entities are expanding the charging network, automotive brands can accelerate this process through strategic partnerships and investments.

Actionable Steps: