A bold move into familiar territory – will it pay off?

Chipotle’s announcement to open its first restaurant in the country, which inspired its menu, raises eyebrows and expectations. Partnering with Latin American restaurant operator Alsea, the US-based chain is entering a market where culinary authenticity isn’t a differentiator; it’s the starting point. For Chipotle, this market entry isn’t just about expansion. It’s a litmus test: Can a brand that interprets Mexican cuisine resonate with consumers who live and breathe it?

The answer will depend not just on flavor but also on strategy and whether modern tools like hyper-local research and cultural intelligence can bridge the gap between inspiration and expectation.

Lessons From the First Movers

Chipotle isn’t the first American brand to try its luck in Mexico. In 1992, Taco Bell debuted in the country with ambitions just as bold. It launched with localised menu tweaks and a confident footprint, but the venture didn’t last. The brand ultimately withdrew, not because of a lack of visibility or investment, but because the offering didn’t quite land with local palates.

That chapter is often cited in business schools, but rarely for what it truly was: an early experiment in exporting food culture into a market that didn’t ask for it. The reaction underscored a gap between adaptation and resonance that modern market research now works to close.

Starbucks’ early entry into Australia offers a parallel lesson. Despite its global brand power, the company struggled to gain traction in a country with a deeply rooted, independent coffee culture. The issue wasn’t coffee quality; it was a misread of consumer behavior, expectations, and local identity. Like Taco Bell in Mexico, Starbucks in Australia became a case study in how even the most successful brands can stumble without cultural alignment.

It’s not a failure; it’s a framework, a snapshot of how global ambition once outran local alignment.

The Evolution of Market Entry Strategy

When Taco Bell opened in Mexico City in the early ’90s, global expansion followed a different playbook. Brands leaned on instinct, broad profiling, and the belief that what worked in the US would translate with minimal adjustment.

But exporting a concept doesn’t guarantee acceptance. Back then, cultural nuance often took a back seat to operational scale. Research was high-level. Brands made decisions based on economic opportunity, not emotional alignment.

That’s changed. Today, market entry starts with precision—predictive analytics to map taste profiles, behavioral segmentation to decode subcultures, and AI-powered simulations to test concepts before rollout. Tools like geo-targeted taste testing, cultural immersion labs, and brand mapping techniques that track real-time perception shifts are helping brands decode how products will land before they ever hit shelves.

In Chipotle’s case, these tools offer a sharper perspective on what Mexican consumers want and will not tolerate.

What Chipotle Brings to the Table

Chipotle isn’t entering Mexico as a fast-food chain. It is arriving as a brand that’s always walked a fine line: Mexican-inspired, never quite Mexican. Its menu leans into simplicity—burritos, bowls, and tacos built around a few core ingredients. This model resonated with US consumers seeking customisable, ingredient-forward meals. But in Mexico, where flavor, preparation, and regional identity are sacred, that same simplicity may land very differently.

Chipotle is partnering with Alsea to bridge that gap, a strategic move offering far more than logistics. Alsea operates Starbucks, Domino’s, and Burger King in Mexico. Its distribution networks, real estate expertise, and consumer insight pipelines offer Chipotle a turnkey path to localisation.

This isn’t Chipotle’s first time using a partnership-first approach. In 2023, the brand entered the Middle East through an agreement with Alshaya Group, opening restaurants in Kuwait and the UAE. There, too, Chipotle leaned on a local partner to navigate cultural preferences and consumer habits. The result? A thoughtful, localised rollout that aligned Chipotle’s “real food, responsibly sourced” ethos with regional values.

But even with the right partner, Chipotle must tread carefully. Mexican consumers know their cuisine – and they know when they’re being sold a version of it. For Chipotle, the win won’t come from mimicry. It’s not competing with Mexico’s beloved taquerias; it’s introducing a distinctly Americanised take on Mexican food. The challenge? Making that distinction matter.

It’s still unclear whether Chipotle will localise its menu for the Mexican market or keep its US offerings intact, which is an early test of how much flexibility the brand is willing to show. Will the Mexican consumer see Chipotle as a fresh alternative, or a foreign remix of something they already do better?

Chipotle’s international journey hasn’t been without its challenges. The brand has maintained a limited footprint in the UK, with around 20 locations, primarily in London, serving a niche but loyal customer base. While not a breakout success, its measured expansion offers lessons in pacing, positioning, and the importance of location strategy. That experience appears to have informed a more deliberate and partnership-driven approach in newer markets like the Middle East and now, Mexico.

Chipotle will also enter a market with an established and competitive fast-casual ecosystem. Local players like El Fogoncito and international chains like Carl’s Jr. and Subway already cater to urban consumers with varied prices and menu formats. However, the real competition may come from independent taquerias and fondas, neighborhood staples that offer affordable, regional fare with generational credibility. Chipotle must offer not just quality, but a reason to belong in Mexico’s culinary hierarchy.

Cultural Intelligence as a Competitive Edge

Culture isn’t a box to check—it’s the playing field.

The brands that succeed today don’t just bring a product; they bring a point of view. They understand how they’re seen, how authenticity is defined, and which signals matter. Cultural intelligence is the edge that separates a foreign brand from a familiar one.

For Chipotle, entering Mexico means navigating a minefield of expectations, where a single design choice or flavor decision could spark either loyalty or backlash. What looks neutral on paper can carry deep meaning on the plate.

Urban consumers in Mexico are increasingly drawn to brands that balance tradition with health-consciousness, speed, and sustainability – expectations that Chipotle must meet beyond just flavor.

This is where research evolves from insight to assurance. Ethnographic studies, in-market panels, and social listening help brands anticipate friction points before they go live. Cultural intelligence doesn’t guarantee success, but it’s often the only way to earn a second look in heritage markets.

Chipotle executives remain optimistic. The company points to the country’s familiarity with Chipotle’s ingredients and affinity for fresh food as key reasons for expansion. But that framing may miss the heart of the matter. Mexican consumers don’t reject American chains outright – Starbucks and Domino’s enjoy massive success. What they’re wary of is reinterpretation. When it comes to their culinary heritage, familiarity isn’t enough. It is identity. And that’s sacred ground.

All eyes will be on how Mexican consumers respond, because in markets where food is identity, perception can make or break the plan. Early commentary across Mexican business and food media has ranged from curiosity to skepticism, with some questioning whether Chipotle’s version of “authentic” will resonate or fall flat. That tension may be the most accurate test of the brand’s cultural fluency.

The New Rules of Global Brand Expansion

Chipotle’s Mexico debut isn’t just another store opening; it’s a bellwether moment. In markets steeped in cultural pride, success no longer hinges on menu tweaks or marketing spend. It hinges on mindset. Brands must listen, learn, and adapt before launch and long after the doors open.

Around the world, consumers are demanding transparency, local relevance, and cultural respect. They expect brands to reflect their values, not just satisfy their appetites.

The one-size-fits-all era is over. Whether entering heritage markets like Mexico, culturally complex ones like India, or hyper-digitised ones like South Korea, the strategy must start with ground-level intelligence. Brands need to know who their customers are, what they value, and when they feel seen.

In food-driven markets, that also means understanding how flavors, textures, and even aromas trigger emotional and cultural responses. Sensory research – testing taste profiles, mouthfeel, and multisensory experiences with local audiences – is emerging as a critical tool for brands looking to translate offerings across borders. It’s not just about what’s on the menu, but how it feels, smells, and satisfies in context.

The companies that thrive treat research not as a formality but as their competitive edge. Chipotle’s move into Mexico may be a test, but it could also be the new blueprint for global brand growth.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Food prices in Japan have surged since 2022, shifting consumer habits in ways that brands cannot afford to ignore. A nationwide study by our sister company, CMG Inc., reveals the extent of this shift, showing how inflation influences where, what, and how often people buy groceries.

Japanese consumers have long prioritised quality and brand loyalty, often paying a premium for fresh, locally sourced ingredients. However, inflation is shifting these behaviours. Our study shows that more shoppers seek discounts, adjust grocery lists, and change stores to cope with rising costs.

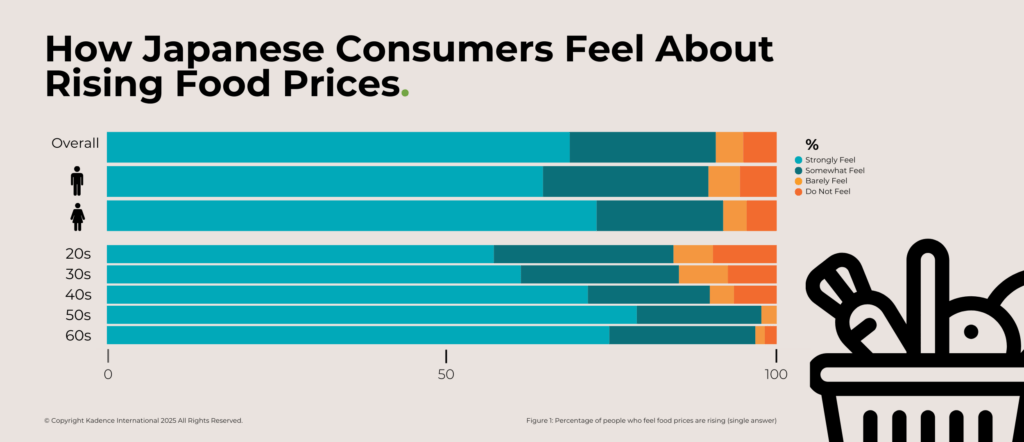

Our study of Japanese consumers aged 20 to 69 found that 90% feel the strain of rising food costs, with 70% experiencing it intensely. Prices for essential staples like rice, leafy greens, and eggs have surged, pushing shoppers toward lower-cost alternatives, bulk buying, and store-switching strategies.

Households are adjusting by choosing cheaper alternatives, relying on discounts, and carefully planning purchases to minimise costs. The findings reveal how inflation shapes the Japanese food market today and how brands must adapt to meet shifting consumer priorities.

Japanese consumers feel the weight of rising food prices

Inflation is hitting middle-aged consumers the hardest. Women and those aged 40 to 60 report the most strain as they juggle rising grocery bills alongside housing, childcare, and utility costs.

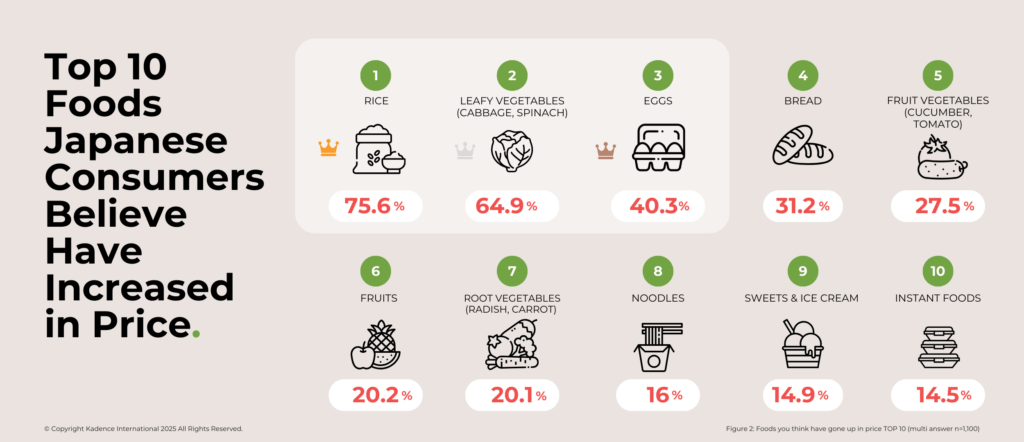

Rice tops the list, with three-quarters of respondents saying its cost has risen. Leafy vegetables, eggs, and fruits are among the most frequently cited items experiencing price hikes. The rising costs of these essentials are pushing consumers to reconsider their grocery lists, with many shifting to more affordable alternatives or cutting back on certain items altogether.

Consumer sentiment suggests inflation is not just a financial strain but an ongoing source of anxiety. Many households are adjusting broader spending patterns, cutting back on dining out and non-essential purchases as they prioritise their grocery budgets. This heightened sense of caution underscores the urgency for brands to meet evolving needs with adaptable solutions.

Implications for Brands

As inflation shapes consumer habits, brands operating in the food industry must rethink their strategies. Price sensitivity is now a dominant force in purchasing decisions, making affordability and value essential selling points. Companies that rely on staple food products may need to introduce smaller pack sizes, bulk discounts, or subscription-based models to maintain customer loyalty.

This shift presents an opportunity for brands that offer alternatives to high-cost staples. The surge in demand for lower-cost items like bean sprouts and tofu suggests that consumers are willing to make substitutions. Positioning these products as smart, affordable choices through targeted marketing and in-store promotions could help brands capture market share.

Retailers and food manufacturers must also recognise that Japanese consumers actively seek ways to save. Loyalty programs, digital coupons, and promotional bundles could play a more significant role in purchasing decisions as shoppers become more selective about where they spend their money. Companies that can balance pricing strategies with perceived value will be best positioned to navigate the evolving food market in Japan.

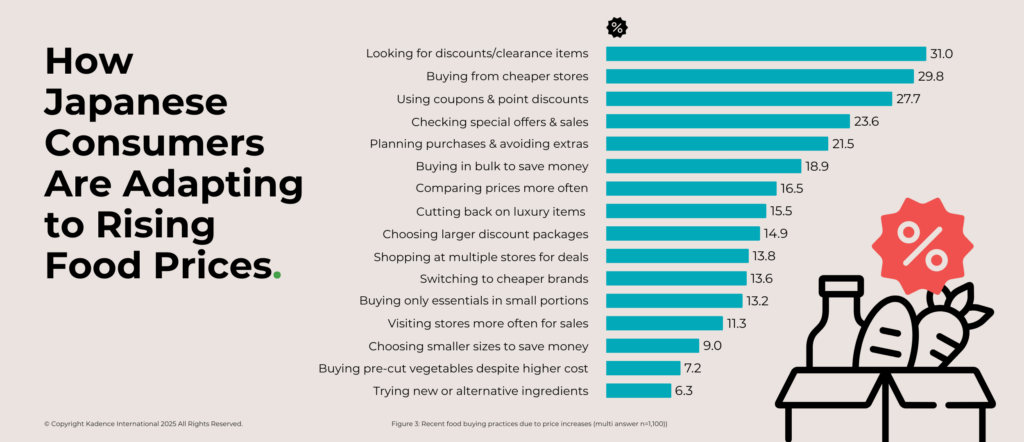

How Consumers Are Changing Their Shopping Habits

As prices climb, Japanese consumers are becoming more strategic. Nearly 30% are actively hunting for clearance deals, while an equal share is switching supermarkets in search of lower prices. Discount chains and bulk retailers see increased foot traffic as shoppers shift from premium stores to budget-friendly alternatives.

Beyond price-driven decisions, shoppers are becoming more disciplined in their purchasing habits. Many are researching deals in advance, planning their shopping lists, and buying only what is necessary. This shift suggests that impulse buying is declining, making it harder for brands to capture spontaneous purchases. Instead, consumers approach grocery shopping with a calculated mindset, weighing every purchase against cost and necessity.

Digital engagement is also playing an increasing role in consumer decisions. More shoppers use online price comparison tools, retailer apps, and e-commerce platforms to track discounts and find the best deals. Brands that integrate their promotions seamlessly into these digital channels will have a greater chance of influencing purchase decisions early on.

However, in-store promotions and point-based rewards in Japan remain highly influential, offering brands an alternative way to engage cost-conscious consumers. Brands that integrate their promotions seamlessly into digital and physical retail channels will have a greater chance of influencing purchase decisions before consumers even enter a store.

Implications for Brands

With price-conscious behaviour shaping the market, brands must adapt their pricing and promotional strategies. Offering flexible discounts and personalised promotions could help retain customers who might otherwise trade down to lower-cost alternatives. Brands traditionally relying on premium positioning may need to consider budget-friendly variations or value packs to stay competitive.

A prime example of a brand adapting to shifting consumer behaviour is Nissin Foods, the maker of Cup Noodles. The company has introduced new flavours and healthier options for health-conscious consumers while maintaining affordability. Its focus on sustainability through eco-friendly packaging and responsible sourcing has also helped sustain consumer loyalty despite economic challenges.

Retailers also need to rethink in-store and digital promotions. Placing high-demand items in visible areas, bundling products at competitive prices, and integrating discount offers into mobile shopping apps can help maintain customer engagement. As shoppers become more deliberate, brands must ensure they are part of the decision-making process before consumers reach the checkout counter.

What are people buying less and more often?

Rice, snacks, and cabbage are the top three foods that people buy less of due to price increases.

Rising prices are forcing consumers to rethink where they shop and what they buy. The survey reveals a clear pattern – high-cost staples are being purchased less frequently, while affordable alternatives are gaining traction. Since 2021, Japan has experienced a significant surge in rice prices. In 2023, the average selling price for a 60-kilogram bag of rice was approximately ¥15,310 (about $139 USD). By January 2025, this price escalated to ¥25,927, a 69% increase from the previous year. This equates to roughly $171 USD.

At the same time, lower-cost and versatile food items are seeing an uptick in sales. Bean sprouts and tofu, known for their affordability and adaptability in Japanese cuisine, are among the top foods people buy more often. Bread, another relatively inexpensive staple, has also gained popularity. The trend suggests consumers prioritise foods that offer more servings, opting for ingredients that stretch further and provide better value.

Implications for Brands

Understanding these shifts is critical for food manufacturers and retailers. Brands in high-cost categories need to rethink how they position their products. Offering smaller portion sizes, value packs, or price promotions could help retain consumers considering cutting back. For brands selling products that are growing in demand, this is a moment to strengthen their market position. Highlighting the versatility, nutritional benefits, and affordability of products like tofu and bean sprouts can reinforce their appeal in price-sensitive times.

Retailers should also adapt by ensuring budget-friendly items are well-stocked and prominently displayed. Promotional strategies should focus on cost-effective meal solutions, helping consumers maximise their grocery budgets. As inflation influences purchasing decisions, brands that align their offerings with consumer priorities will be best positioned to maintain loyalty and sales.

How Japan’s food inflation compares to the West

Rice isn’t just a staple in Japan—it’s a cultural cornerstone and an economic indicator. Unlike many Western nations where grains are heavily imported, Japan produces most of its rice domestically, meaning price fluctuations reflect deeper economic shifts. This inflation trend mirrors similar surges in other staple foods worldwide, such as wheat in the U.S. and soybeans in China.

Food prices are rising worldwide, but the impact varies from country to country. While Japan is seeing sharp increases in staples like rice, vegetables, and eggs, the US and the UK markets are grappling with their inflation-driven shifts in consumer behaviour. In Western markets, dairy products, meat, and processed foods have been among the most affected categories, driving consumers toward discount grocery chains, bulk buying, and private-label alternatives.

In the US, shoppers increasingly turn to wholesale retailers and discount supermarkets to cut costs. Many are switching from brand-name products to store-brand alternatives, with major retailers reporting a surge in private-label sales. Coupon usage once thought to be in decline, has made a strong comeback, mainly through digital platforms and loyalty apps. In the UK, where food inflation and the cost of living have been a persistent challenge, many households are scaling back on meat purchases and opting for frozen or tinned foods as a cost-saving measure.

Despite regional differences, the global trend is clear – consumers are becoming more intentional about how and where they spend their grocery budgets. The shift toward discount-driven shopping, meal planning, and strategic purchasing decisions redefines how food brands and retailers operate across markets.

While Japan sees a shift toward staples like tofu and bean sprouts, the US and UK consumer shifts lean toward private labels and bulk buying, highlighting different approaches to cost savings.

Implications for Brands

Brands must recognise that price sensitivity is no longer confined to specific regions. Inflation-driven purchasing habits are reshaping consumer expectations on a global scale. Affordability and value have become key decision-making factors, making it essential for brands to rethink their pricing and promotional strategies.

Companies that traditionally cater to premium or discretionary food categories may need to introduce flexible pricing structures, offering economy-sized packaging or subscription models to retain budget-conscious shoppers. Meanwhile, brands positioned in lower-cost categories have a unique opportunity to strengthen their appeal, emphasising the affordability and versatility of their products.

Japan’s beef bowl industry thrives despite multiple price hikes due to rising costs. Zensho Holdings, the parent company of Sukiya, a Japanese restaurant chain that serves gyudon (beef bowls), curry, and other dishes, has reported strong profit growth and increased customer numbers, highlighting how strategic pricing and strong brand equity can sustain demand even in inflationary times. This resilience reflects Japan’s unique consumer behaviour, where quality and convenience often precede purely cost-cutting measures.

Retailers, particularly those in markets where discount shopping is on the rise, should focus on making savings more accessible. Digital loyalty programs, targeted promotions, and clear communication around price advantages will be critical in maintaining consumer trust and engagement in a price-sensitive environment.

How brands can adapt to a cost-conscious market

Food inflation is not just reshaping consumer habits but redefining how brands must approach pricing, marketing, and product development. As shoppers prioritise affordability and shift toward lower-cost alternatives, companies must take a proactive approach to remain relevant in a rapidly changing market.

One of the most immediate strategies for brands is pricing flexibility. Offering a range of product sizes at different price points can help cater to varying consumer budgets. Smaller packaging options can attract shoppers looking to control their spending, while bulk discounts can appeal to those who prefer to stock up when prices are favourable. Subscription models that provide cost savings over time may also help retain customer loyalty, particularly for staple goods.

Product positioning is equally important. Brands that once relied on premium pricing must now justify their value through differentiation. Messaging focusing on nutritional benefits, sustainability, or versatility can encourage consumers to keep buying products even if prices increase. For brands in high-growth categories like tofu and bean sprouts, reinforcing affordability and multiple-use meal applications can strengthen market share.

Retailers have a crucial role to play in guiding purchasing decisions. Strategic in-store placements, meal-planning promotions, and digital tools that showcase the best value options can help shoppers navigate rising prices. Supermarkets that integrate personalised discounts, loyalty rewards, and digital coupons into their customer experience will be better positioned to retain price-sensitive consumers.

The brands that succeed in an inflationary market will listen to consumers, adapt to shifting priorities, and offer tangible value beyond price alone. As economic conditions continue to shape spending behaviour, remaining flexible and responsive will define long-term brand resilience.

Turning Challenges Into Opportunities

Rising food prices are forcing consumers to rethink their purchasing decisions, but they are also creating new opportunities for brands willing to adapt. The shift toward cost-conscious shopping is not a temporary adjustment; it reflects a more profound change in consumer behavior likely to persist even if inflation stabilises. Brands that recognise these shifts and respond strategically will retain their customer base and strengthen their market position in the long run.

Innovation will be key for companies in high-cost categories. Reformulating products to be cost-effective without compromising quality, offering flexible portion sizes, and introducing alternative ingredients can help brands navigate price sensitivity. For companies in growing categories, reinforcing the value of their products through effective messaging and promotions will be essential to sustaining momentum.

Digital engagement is also becoming more critical. Consumers increasingly rely on price-comparison tools, e-commerce discounts, and loyalty programs to make informed purchasing decisions. Brands that invest in personalised marketing, mobile-based promotions, and transparent pricing strategies will be better positioned to build long-term trust with their audience.

Food inflation is reshaping the competitive landscape but must not be a setback. Companies that approach this challenge with flexibility, creativity, and consumer-first thinking can turn market uncertainty into a moment of strategic growth.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Need to find the right sample size for your study? Our Sample Size Calculator delivers quick, accurate results.

What is a Sample Size Calculator?

A Sample Size Calculator helps you determine the number of people you need to survey for reliable results. By entering key details like population size, confidence level, and margin of error, you can calculate the ideal sample size for accurate research findings. For example, If you’re surveying 10,000 customers and want 95% confidence with a 5% margin of error, the calculator will tell you how many responses you need to ensure trustworthy insights.

Calculate your sample size

What Does the Result Mean?

The sample size calculation tells you how many people you must survey to get reliable results. If the calculator suggests 400 respondents, that means surveying at least 400 people will give you statistically reliable results within your chosen margin of error. A larger sample size increases accuracy, while a smaller one may produce less precise results. Use this number to plan your survey with confidence!

Tips: Want more precision? Lower the margin of error, but this will increase the required sample size. Not sure how many people to survey? Try different confidence levels and margin of error settings to see how they affect sample size.

Now that you have your sample size, what’s next? Need to check how precise your results are? Use our Margin of Error Calculator to measure the accuracy of your survey.

How to Use the Sample Size Calculator

Step 1:Enter your Population Size – This is not the total population of a country or city. It’s the specific group you want to study (e.g. school students between the ages of 10 to 16 in the U.S.). If you’re surveying customers of a particular store, the population size is the total number of customers who shop there, not the entire city.

Step 2: Choose your Confidence Level – Select how sure you want to be about your results (90%, 95%, or 99%). A higher confidence means greater certainty but requires more responses to reduce errors. For example, a 95% confidence level is the standard for most surveys, but if you choose 99%, you’ll need a larger sample size for higher accuracy.

Step 3: Select your Margin of Error – The range within which the true result may vary. Choose how much your results might vary from the true answer. ✔ Smaller margin (±3%) → More accurate results but requires more responses. ✔ Larger margin (±5% or more) → Less precise but needs fewer responses. For example, If 60% of people like a product and your margin of error is ±3%, the real number could be between 57% and 63%. A ±5% margin means it could be between 55% and 65%.

Step 4:View Your Sample Size – The tool will tell you how many responses you need for reliable data.

Step 5: Plan your survey: Use this number to ensure your research is accurate and meaningful before launching your survey.

Why Does Sample Size Matter?

Getting the right sample size is key to accurate and reliable results. Here’s why it’s important:

✔ Accuracy – Reduces errors and makes your survey results more reliable. ✔ Efficiency – Saves time and resources by collecting just the right amount of data. ✔ Trustworthy Insights – Ensures your findings reflect the whole population, not just random chance.

Want to ensure your qualitative research captures the right insights?

Explore how different approaches impact your study and discover best practices for gathering meaningful data in ourexpert guide on sampling methods.

Who Can Use This Calculator?

✔ Market Research and Businesses – Find the right number of customers to survey for product feedback and market trends. ✔ Academic & Social Research – Ensure studies accurately represent populations for research and policy analysis. ✔ Healthcare & Clinical Trials – Determine how many patients are needed for valid medical research. ✔ Employee & Workplace Surveys – Gather reliable employee insights for engagement and policy decisions. ✔ Government & Public Policy – Calculate voter research and census study respondents. ✔ Media & Advertising – Measure audience opinions and ad effectiveness with accurate sample sizes.

Now that you have your sample size get expert insights to maximize your survey’s design. We provide in-depth insights to drive better decisions as a leading market research agency.

Need to find the right sample size for your study? Our Sample Size Calculator delivers quick, accurate results.

What is a Margin of Error Calculator?

A Margin of Error Calculator helps you understand how much your survey results might change if you surveyed more people. It shows the possible difference between the results you got and what the true answer might be for the whole population. Example: If 60% of people say they like a product with a ±5% margin of error, the actual percentage could be anywhere between 55% and 65%. A smaller margin of error means more precise results, but it usually requires a larger sample size. This tool helps businesses, researchers, and marketers measure the reliability of their data before making important decisions.

Calculate your margin of error

What Does the Result Mean?

The margin of error tells you how much your survey results might change if you surveyed more people.

✔ Smaller margin of error (e.g., ±3%) → More accuracy, but requires more responses. ✔ Larger margin of error (e.g., ±5% or more) → Less precision but needs fewer responses.

Step 1: Enter your Sample Size—The number of people who completed your survey. More responses = better accuracy. For example, if 250 people answered your survey, enter 250 as your sample size.

Step 2: Enter your Population Size – This is not the population of a place. It is the total number of people in the group you want to study. If unsure, use an estimate. For example, if you’re surveying employees at a company with 5,000 staff members, your population size is 5,000.

Step 3: Pick your Confidence Level – How sure do you want to be about your results? Common choices are 90%, 95%, or 99%. A higher confidence level means more accuracy but requires more responses. For example, a 95% confidence level means that if you repeated the survey 100 times, you’d get similar results 95 times.

Step 4: View your Margin of Error—The tool will show your Margin of Error, the possible range by which your results may vary. For example, if 60% of people in your survey like a product and your margin of error is ±4%, the actual percentage could be anywhere between 56% and 64% in the full population.

Why Is It Important to Calculate the Margin of Error?

✔ Ensures Accuracy – Helps you understand how close your survey results are to the true population data. ✔ Builds Confidence – A lower margin of error means you can trust your findings when making important decisions. ✔ Guides Sample Size – Shows whether you need more responses to improve precision. ✔ Detects Meaningful Differences – Helps determine whether small survey result changes are real or just random variations. ✔ Essential for Business and Research – Used in market research, healthcare studies, polling, and decision-making to ensure reliable insights.

Want to create better surveys? Learn how to ask the right questions and get reliable answers in our market research survey guide.

Who Can Use This Calculator?

✔ Market Research and Businesses – Check customer surveys’ reliability before making decisions. ✔ Academic and Social Research – Ensure studies accurately represent populations for research and policy analysis. ✔ Healthcare and Clinical Trials – Determine how many patients are needed for valid medical research. ✔ Employee and Workplace Surveys – Gather reliable employee insights for engagement and policy decisions. ✔ Government and Public Policy – Calculate how many people are needed for voter research and census studies. ✔ Media and Advertising – Measure public opinion and ad effectiveness with accurate sample sizes.

Now that you know your margin of error, get expert insights to maximize your research!

Need help designing your survey or analyzing results? As a leading market research agency, we provide in-depth insights to drive better decisions. Contact us today to discuss your research needs!

Like many developing countries, Indonesia‘s economic liberalisation in the mid-1980s brought growth alongside inequality.

Urban centres thrived, attracting investment, jobs, and infrastructure, while rural areas lagged, widening the gap in living standards. This divide extends beyond income and development, shaping the distinct consumer behaviours seen today.

In urban areas, consumers are drawn to the convenience of modern retail formats like malls, hypermarkets, and e-commerce. Meanwhile, in rural regions, traditional markets and neighbourhood stores remain the preferred choice, rooted in community ties and local customs. Understanding these contrasting buying behaviours is essential for brands navigating Indonesia’s vast and diverse market.

The Urban Retail Landscape of Indonesia

Modern retail dominates Indonesia’s growing urban centres. Cities like Jakarta, Surabaya, and Bandung boast sprawling malls, hypermarkets, and a robust e-commerce ecosystem. Urban consumers, with higher incomes and better access to technology seek convenience, variety, and efficiency in their shopping.

Malls are more than just shopping destinations; they are social hubs where people gather for entertainment, dining, and leisure. The rise of hypermarkets, offering a one-stop shopping experience, has further driven urban consumers away from traditional markets. E-commerce, fueled by Indonesia’s increasing internet penetration, has also reshaped shopping habits, allowing urban dwellers to make purchases from the comfort of their homes, particularly for fashion, electronics, and household items.

Key data & insights about Indonesia’s urban consumers:

Infrastructure improvements and the growing middle class drive urban retail growth.

According to a 2023 Nielsen report, urban households spend nearly 30% of their monthly income on modern retail and e-commerce, compared to 8% in rural areas.

Platforms like Tokopedia, Shopee, and Lazada have experienced rapid growth in cities, capitalising on the shift toward digital purchasing and mobile payments.

Urban Consumer Behaviour

Urban consumers in Indonesia exhibit distinct characteristics shaped by rapid urbanisation, rising incomes, and a growing middle class. Key behaviour patterns include:

Emphasis on Convenience and Speed: Urban consumers prefer quick, seamless shopping. They gravitate toward one-stop shops like malls and hypermarkets, where they can find a variety of products under one roof. Time efficiency is essential for busy city dwellers.

High Adoption of Digital Channels: Urban Indonesians are increasingly comfortable with digital shopping. E-commerce platforms like Tokopedia and Shopee have transformed purchasing habits, especially in fashion, electronics, and household goods. McKinsey reports that urban households are more likely to experiment with online shopping and are heavy social media users, although full adoption of e-commerce still faces hurdles.

Brand Loyalty and Preference for Local Products: Despite exposure to global brands, Indonesian urban consumers strongly value local products, particularly in food and beverage categories. However, perception matters greatly—many consumers mistakenly believe international brands with localised marketing are Indonesian, giving global brands opportunities if they adapt effectively.

Mobile and Social Media Usage: Urban consumers are heavy users of smartphones and social media platforms. However, despite high engagement in social media, trust issues with online payment systems mean that urban Indonesians still often hesitate to fully embrace e-commerce.

Shift Toward Premium and Discretionary Spending: With rising disposable incomes, urban consumers are increasingly willing to spend on premium products and discretionary items such as travel, leisure, and personal electronics. This trend is expected to accelerate as more Indonesians join the consuming class by 2030.

Example: Tokopedia’s Urban Expansion Strategy

Image Source: KrASIA

Tokopedia, one of Indonesia’s leading e-commerce platforms, recognised the rapid shift toward digital purchasing among urban consumers and developed a targeted strategy to capitalise on this growing trend. Tokopedia invested heavily in its logistics network to ensure same-day or next-day delivery in urban centres like Jakarta and Surabaya. This fast fulfilment option was a key differentiator for time-sensitive urban shoppers, who value convenience above all.

Tokopedia also launched hyper-targeted promotions and partnerships with local urban retailers, blending e-commerce with brick-and-mortar stores. As a result, they managed to capture a significant portion of the urban retail market. From January to May 2023, Tokopedia saw an increase in inter-island shipments, with the farthest shipment happening from Medan (North Sumatra) to Merauke (Papua). In addition to helping people meet their physical product needs, Tokopedia makes it easier for people to access digital products.

Tokopedia’s success illustrates how e-commerce platforms can tap into Indonesia’s urban consumer base by focusing on fast delivery, localised strategies, and convenience—meeting the high expectations of tech-savvy urban shoppers.

The Rural Retail Landscape in Indonesia

In rural Indonesia, traditional markets and small neighbourhood stores, known as warungs, remain the cornerstone of daily shopping for most households. These informal retail channels offer essential goods and serve as key social hubs for rural communities. Rural buying habits are deeply rooted in cultural practices and community ties, differing significantly from urban shopping behaviours.

Key data & insights about Indonesia’s urban consumers:

According to McKinsey, over 60% of rural consumers still rely heavily on traditional markets, even though modern retail formats are gradually entering these areas.

Due to limited income and a cash-based economy, rural consumers are more likely to make frequent, small-value purchases. Cash transactions account for over 90% of retail purchases in these areas.

The role of neighbourhood stores remains significant because of limited access to larger, modern retail outlets and logistical challenges stemming from Indonesia’s geographical diversity, with thousands of islands and less-developed infrastructure.

Consumer Behaviour in Rural Indonesia:

Trust and Familiarity: Rural consumers tend to shop at stores with established trust with the vendor. Unlike urban consumers who prefer the efficiency of hypermarkets and e-commerce, rural buyers are more likely to develop long-term relationships with local shopkeepers.

Community-Centric Shopping: Rural shoppers often view traditional markets as social spaces where they can interact with friends and neighbours, making shopping a communal experience. The lack of infrastructure for larger retail chains often reinforces the need for these local markets to thrive.

Lower Brand Awareness: Rural consumers have lower brand awareness than urban consumers. Large marketing campaigns influence them to choose products based on price and familiarity.

Limited Adoption of Digital Transactions: E-commerce has not yet fully penetrated rural areas, with low levels of digital literacy and unreliable internet access being major barriers. Rural consumers typically prefer to see and touch products before purchasing, which challenges brands looking to expand online.

Example: Indofood’s Success in Rural Markets

Image source: Seeking Alpha

Indofood, Indonesia’s leading food company, has successfully navigated the rural market through its widespread distribution network and focus on affordable, locally adapted products. By focusing on everyday essentials like instant noodles and snacks, Indofood has built a strong presence in rural communities. The company’s strategy involved partnering with local vendors and warungs, ensuring its products reached even the most remote regions.

Indofood’s localised pricing and packaging, such as smaller, affordable portions, have catered to the economic realities of rural consumers. The brand’s deep integration into the rural retail landscape showcases how companies can thrive by tailoring products and pricing to local needs.

Drivers Behind the Urban-Rural Divide in Indonesia

The stark differences in consumer behaviour between Indonesia’s urban and rural populations are shaped by a complex interplay of geographic, economic, and cultural factors. These underlying drivers help explain why urban areas lean towards modern retail formats while rural areas prefer traditional markets and local stores.

Geographical and Infrastructure Barriers

Fragmented Geography: Indonesia’s vast archipelago of over 17,000 islands creates logistical challenges for modern retail expansion in rural areas. Remote villages often lack the infrastructure needed for large retailers or e-commerce to penetrate these markets effectively. As a result, rural consumers continue to rely heavily on nearby traditional markets.

Access to Technology and Internet: Urban centres enjoy better internet connectivity and mobile coverage, fostering the growth of e-commerce and digital payments. However, rural regions suffer from unreliable connectivity, limiting the adoption of online shopping and digital transactions.

Economic Disparities

Income Levels: Urban households typically enjoy higher incomes, enabling them to spend more on premium goods and services. McKinsey reports urban consumers account for 55% of Indonesia’s GDP, driven by the increasing affluence of middle-class families. In contrast, rural areas have lower purchasing power, driving consumers to prioritise affordability and essential goods.

Discretionary vs. Essential Spending: Urban consumers allocate a significant portion of their income to discretionary spending, including fashion, electronics, and leisure, while rural households focus more on essentials like food and daily necessities. This leads to differences in the types of products available in rural traditional markets versus urban malls and hypermarkets.

Cultural Preferences

Community and Trust: In rural areas, shopping is a community-centric activity, where trust in local vendors is crucial. Consumers prefer to buy from people they know and have established relationships with, reinforcing the role of neighbourhood stores and traditional markets.

Modern vs. Traditional Lifestyles: Urban consumers, influenced by globalisation and digital media, are more open to adopting modern lifestyles and shopping habits. This includes using mobile wallets, loyalty programs, and online promotions. Meanwhile, rural consumers tend to stick to long-standing traditions and purchase behaviours that are less affected by global trends.

Emerging Trends in Both Markets

Urban Retail: There is a clear trend toward premiumisation in cities, with more urban consumers willing to pay for high-end products. Rising disposable incomes and greater exposure to international brandssupport this trend. E-commerce is also rapidly growing, especially among younger, tech-savvy urbanites prioritising convenience and speed.

Rural Shift: While traditional markets dominate, rural areas are starting to see the introduction of small-scale modern retail formats such as convenience stores. Brands are beginning to explore hybrid models that combine modern convenience with the local, community-driven experience that rural consumers value.

Bridging the Divide: Opportunities for Brands in Indonesia

The urban-rural divide presents both challenges and opportunities for brands. Successfully navigating these markets requires a tailored approach that recognises each consumer base’s unique needs and preferences. Brands that can adapt their strategies to cater to urban and rural shoppers stand to gain significant traction in Indonesia’s rapidly growing economy.

Strategy for Urban Markets

Digital Transformation and E-Commerce: In urban centres, brands must strengthen their digital presence. This includes investing in e-commerce platforms, mobile apps, and digital marketing strategies to meet the expectations of tech-savvy urban consumers. Offering features such as personalised shopping experiences, app-based promotions, and fast delivery services are key to success.

Premiumisation and Loyalty Programs: As urban consumers shift toward premium products, brands should leverage loyalty programs, exclusive online offerings, and partnerships with premium retailers to capture this growing segment. Creating a seamless omnichannel experience where physical and digital stores complement each other can enhance customer engagement.

Strategy for Rural Markets

Local Trust and Personalisation: Brands targeting rural markets should prioritise building trust and offering personalised, localised experiences. Partnering with traditional market vendors and warungs can help reach rural consumers who rely on these familiar channels. Smaller packaging and affordable pricing, tailored to the spending power of rural buyers, will also resonate with this demographic.

Adapting Modern Retail Formats: Introducing modern retail formats, such as mini-marts and convenience stores, in rural areas can bridge the gap between traditional markets and modern trade. These stores should balance modern convenience and local appeal, offering products that rural consumers trust at prices they can afford.

Hybrid Retail Models

Blending Traditional and Modern: A hybrid retail model may be key to succeeding across Indonesia’s urban and rural markets. Brands that combine the convenience of modern retail with the trust and familiarity of traditional channels can win over consumers from both demographics. For instance, local brands could experiment with smaller physical stores in rural areas offering e-commerce options for urban dwellers, creating an integrated shopping experience.

Final Thoughts

Indonesia’s urban-rural divide presents a unique landscape where brands must balance modern retail innovations with deep-rooted traditional practices. While urban areas are hubs of growth, driven by rising incomes, digital adoption, and a shift toward premium products, rural areas remain anchored in trust, familiarity, and community-oriented commerce. The key to navigating this divide lies in developing nuanced strategies that respect these differences while capitalising on the evolving retail dynamics in both markets.

Brands that succeed in Indonesia will be those that can not only cater to urban consumers’ demand for convenience and digital integration but also engage rural shoppers through personalised, trust-based relationships. Bridging this gap requires a hybrid approach—leveraging e-commerce, modern retail formats, and mobile technologies in urban regions while maintaining localised, affordable, and culturally relevant offerings in rural areas.

By aligning their strategies with these consumer behaviours and considering the economic and infrastructural challenges, brands can create a strong presence across both urban and rural markets. In doing so, they can secure a competitive edge in one of Southeast Asia’s most diverse and fast-growing markets, ensuring long-term success and customer loyalty.

When executed with precision and cultural sensitivity, this tailored, dual-market approach can unlock significant growth potential, allowing brands to thrive amidst Indonesia’s diverse and rapidly transforming retail environment.

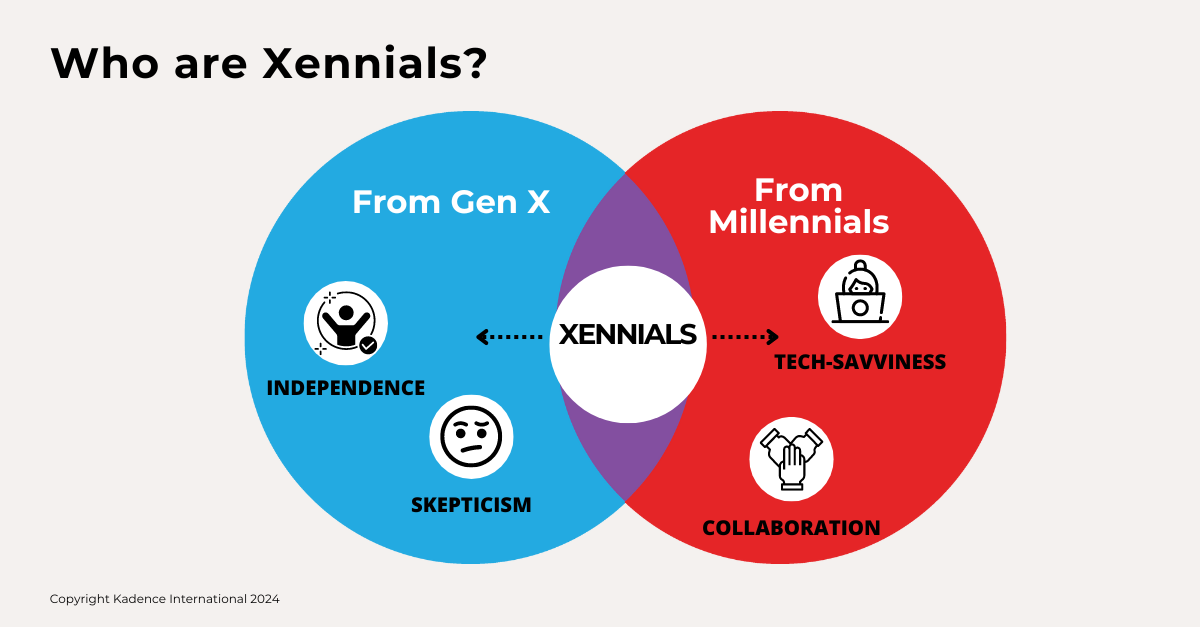

Too young for MTV Unplugged and too old for Snapchat, Xennials find themselves in a unique generational sweet spot. Born between 1977 and 1985, this micro-generation bridges the gap between Gen X’s analogue childhood and Millennials’ digital-first upbringing. They’re old enough to remember life without the internet yet young enough to have embraced social media, smartphones, and streaming services.

Often overlooked, Xennials carry significant cultural and economic influence, blending Gen X’s scepticism with Millennials’ optimism. Understanding Xennials is crucial for global brands crafting nuanced, cross-generational strategies. Brands and market researchers must prioritise them, especially across key Western and Asian markets.

Definition and Origin of Xennials

The term ‘Xennials’ refers to those born between 1977 and 1985. Sitting between Generation X and Millennials, this micro-generation was shaped by societal and technological shifts, having grown up in a world transitioning from analogue to digital. Xennials experienced life before the internet, yet they were among the first to adopt it. This unique combination gives them a distinctive perspective—blending traditional values with modern technological comfort.

Unlike Gen X, often characterised by scepticism and individualism, Xennials tend to have a more optimistic, adaptive outlook, closer to Millennials. However, they’re less digitally dependent than Millennials, maintaining a balance between tech-savviness and pragmatic realism.

Key Characteristics of Xennials

Xennials are known for several traits that make them a standout consumer group:

Adaptability: Xennials are highly adaptable, seamlessly transitioning from landlines and paper maps to smartphones and GPS. This adaptability makes them early adopters of new technologies without the digital dependency seen in younger generations.

Technological Savviness: Growing up alongside the rise of the internet, Xennials are fluent in digital technologies but maintain caution, balancing their online and offline lives.

Value-Driven Purchases: Xennials prioritise quality, longevity, and sustainability, focusing more on value-driven purchase decisions than brand loyalty.

Global Insights on Xennials

While Xennials share core characteristics globally, cultural and economic contexts influence their behaviours:

United States: Xennials in the US tend to be financially cautious, particularly after the 2008 crisis, with spending directed toward practical purchases like home improvement and wellness.

United Kingdom: Similar to the US, UK Xennials value sustainability and ethical business practices, balancing digital literacy with technological scepticism.

China: Chinese Xennials are highly tech-savvy but remain deeply rooted in family values, often investing in property and education.

India: In India, Xennials are a bridge generation, embracing mobile technology and e-commerce while maintaining strong ties to community and family.

Singapore: Xennials in Singapore are highly urbanised and focus on quality over novelty, especially in areas like education and technology.

The Xennial Consumer

Xennials blend digital savviness with caution. Learn how behavioural economics, personalisation, and ethical marketing can help brands connect with this generation.

Xennials’ buying behaviours are shaped by their pre-internet childhood and fully digital adulthood. This unique positioning influences their preference for quality over quantity, brand loyalty with caution, and a focus on experiences over possessions.

Quality Over Quantity: Xennials prefer products with durability and long-term benefits, choosing to invest in items that last over fleeting trends.

Brand Loyalty with Caution: While they exhibit brand loyalty, Xennials are discerning consumers. They prioritise brands that align with their sustainability and ethical sourcing values, making loyalty contingent on transparency and authenticity.

Experiences Over Possessions: Like Millennials, Xennials prioritise experiences—travel, wellness, and personal development—over material goods, but with a more practical, less impulsive approach.

Spending Power

These cautious yet value-driven behaviours translate directly into their spending power across key industries. In their late 30s and early-to-mid 40s, Xennials hold significant economic power, balancing family obligations with career advancement. Xennials are notable for spending on home renovations and family services, reflecting their dual roles as professionals and parents.

Global Insights

Brands that successfully engage Xennials understand the importance of aligning with their values of practicality, quality, and social responsibility:

United States: Apple’s long-lasting products and seamless ecosystem resonate with Xennials, who appreciate functionality and durability.

United Kingdom: Waitrose taps into Xennials’ preference for ethically sourced, high-quality products that support sustainability and reduce plastic.

Japan: Muji’s minimalist, functional, and sustainable goods appeal to Xennials, who value durability and ethical consumption.

Indonesia: Tokopedia has successfully targeted Indonesian Xennials, focusing on reliability, trust, and seamless online shopping experiences.

The Role of Technology in Xennial Lives

Technology Adoption

Xennials approach technology with caution and balance. Unlike Gen X, who were slower to adopt new technologies, and Millennials, who embraced it without hesitation, Xennials strike a middle ground. Their comfort with both analogue and digital worlds makes them adept at using modern tools, but they remain pragmatic about integrating technology into their lives.

Impact of Social Media and E-Commerce

Xennials use social media and e-commerce strategically rather than impulsively. They use platforms like Facebook and LinkedIn to network and stay informed while avoiding viral challenges and performative content. When it comes to online shopping, Xennials prefer trusted platforms that prioritise transparency and authenticity.

Singapore: Platforms like Lazada and Qoo10 cater to Xennials’ desire for affordable, high-quality products.

Vietnam: Social commerce is growing in Vietnam, and Xennials prefer established brands like Tiki, emphasising transparency and reliability.

Real-Life Examples

Tata CliQ (India): This e-commerce platform appeals to Xennials with a focus on premium, branded products, clear product descriptions, and transparency.

Decathlon (Global): Decathlon combines affordability with eco-friendly initiatives, appealing to Xennials’ practicality and commitment to sustainability.

FairPrice (Singapore): FairPrice’s mix of digital and offline experiences, sustainability focus, and personalised recommendations resonate with tech-savvy Xennials.

Brand Strategies for Reaching Xennials

Personalisation and Value-Driven Marketing

To effectively engage Xennials, brands must go beyond traditional marketing approaches and focus on personalised, value-driven strategies. Xennials gravitate towards brands offering more than just a product—authenticity, sustainability, and quality are key. This group is particularly discerning, preferring brands that align with their ethical values and offer practical benefits.

AI-Powered Personalisation: Using AI-driven predictive models, brands can create hyper-targeted campaigns based on Xennial preferences. This data-driven approach allows for tailored recommendations and individualised experiences.

Sustainability and Ethics: Xennials gravitate toward brands emphasising sustainability, fair trade, and corporate transparency. Highlighting long-term value and social impact can build trust.

Behavioural economics provides deeper insights into the psychological drivers behind Xennials’ purchasing decisions, offering brands a more nuanced way to influence their choices. By understanding principles like loss aversion, social proof, and present bias, brands can craft strategies that resonate with Xennials’ values and decision-making processes.

Loss Aversion: Xennials are risk-averse, having experienced economic uncertainties. Brands can frame their products as long-term investments to help Xennials avoid potential future losses.

Social Proof: Authentic reviews and community endorsements build the trust Xennials seek before committing to a purchase. Leveraging this can strengthen brand relationships.

Present Bias: Xennials value long-term quality but are also motivated by immediate rewards. Limited-time offers and personalised discounts can appeal to this bias while aligning with their demand for quality.

Anchoring Effect: Brands can present premium product versions to set higher reference points, making their standard offerings seem like better-value alternatives.

Ethical Framing: Xennials are drawn to brands that highlight ethical practices. Framing product choices around social or environmental benefits appeals to their preference for ethical consumption.

By integrating these behavioural principles, brands can create campaigns that resonate deeply with Xennials’ motivations, driving trust and loyalty.

Marketing to Xennials Across Regions

Global brands must adapt to regional contexts while maintaining consistency. Here are some examples:

Thailand: Unilever has built strong connections with Xennials through sustainability-focused campaigns in personal care products.

The Philippines: Globe Telecom targets Xennials through its digital services and messaging around environmental conservation and digital education.

United Kingdom: John Lewis & Partners focuses on ethical sourcing and sustainability, resonating with Xennials who value quality and longevity.

Actionable Insights for Senior Leaders

Leverage Data for Personalisation: Use AI and CRM systems to deliver personalised experiences.

Emphasise Long-Term Value: Focus on quality and sustainability to build trust and loyalty.

Maintain Global Consistency with Local Sensitivity: Adapt strategies to different cultural contexts while staying true to core brand values.

Final Thoughts

Xennials represent a unique micro-generation that bridges the gap between Gen X and Millennials. Straddling both the analogue and digital worlds, Xennials showcase adaptability, technological savvy, and value-driven purchasing habits. They prioritise quality, sustainability, and authenticity in their consumer choices and have become influential across various markets. As they continue to age into leadership and decision-making roles, Xennials hold significant spending power, making them a critical demographic for brands to understand and engage.

Actionable Recommendations to Engage Xennials

For brand managers and CMOs, integrating Xennial-specific strategies into global marketing plans can create a lasting impact.

Here are clear steps to consider:

Focus on Personalisation: Use data-driven insights to deliver highly personalised experiences that resonate with Xennials’ preferences and values.

Emphasise Longevity and Quality: Ensure your products offer lasting value and practical benefits. Xennials are more likely to invest in quality over fleeting trends.

Align with Values of Sustainability and Ethics: Communicate your brand’s sustainability initiatives and ethical practices. This generation is drawn to brands that reflect their desire for positive social and environmental impact.

Balance Digital and Offline Channels: While Xennials are fluent in digital technology, they still appreciate offline touchpoints and real-world experiences. Offer a balanced approach catering to their preferences online and offline channels.

Adapt Regionally: While maintaining core brand consistency, tailor your marketing strategies to suit the local context in different regions, especially in Asia and Western markets, to fully engage Xennials.

As Xennials age into their 40s and beyond, their influence on consumer behavior will grow. With their increasing presence in leadership roles, Xennials are poised to drive trends in sustainability, technology adoption, and value-driven purchasing. Brands that successfully engage this generation today will position themselves to benefit from their long-term loyalty and advocacy, shaping consumer markets for years to come.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

What’s more critical in international marketing—relevance or global consistency?

For global brands, this question defines the core of strategic decision-making. Global consistency safeguards a unified brand identity across all markets, while relevance allows a brand to adapt its message to local cultures and consumer behaviours. As international markets become increasingly interconnected, brands must navigate the delicate balance between the two.

Striking this balance is among the most complex challenges facing multinational marketing leaders. While global consistency helps reinforce brand trust and recognition, relevance ensures a brand connects deeply with the local audience. So, how do global consistency and cultural relevance coexist to drive international growth?

Defining Local Relevance in International Marketing

Local relevance in international marketing requires more than surface-level localisation or simple translation. While global consistency provides the foundation, relevance ensures your message resonates with cultural nuances.

This understanding can make the difference between success and failure in highly fragmented and competitive markets. Brands that tailor their strategies to fit regional preferences and cultural norms create stronger consumer connections.

Today, relevance is not a choice; it’s a necessity. Consumers aren’t just seeking products; they want brands that understand and align with their cultural contexts. Brands that successfully adapt their message while maintaining core values tend to outperform those that adopt a uniform, one-size-fits-all approach across regions.

L’Oréal is agreat example. The brand faced this challenge when entering Japan’s beauty market. Their traditional messaging, which worked well in Western markets, wasn’t resonating with Japanese consumers, who prioritise skincare over makeup. To connect with this audience, L’Oréal shifted focus from makeup to skincare, positioning it as foundational to beauty, in line with Japanese cultural values. A highly successful localised campaign strengthened L’Oréal’s market position without compromising its global brand identity. This campaign shows how local relevance can thrive without compromising global consistency when executed with care.

The Importance of Global Consistency in Brand Campaigns

Global consistency is essential for maintaining a recognisable and trustworthy brand identity across multiple markets. While relevance allows for local adaptation, global consistency ensures the brand’s core message and values remain intact. Consumers increasingly expect a stable brand experience, whether they interact with the brand in New York, Shanghai, or Jakarta.

Consistency is particularly critical in sectors like luxury goods or technology, where consumers seek assurance of high quality and reliability. A fragmented brand identity can confuse consumers, erode trust, and ultimately weaken brand equity. Consistency creates a stable foundation upon which localised adaptations can be built without compromising the brand’s essence.

Apple’s Global Consistency

Apple has mastered the balance between consistency and relevance. Across all its markets, Apple’s brand identity remains focused on innovation, premium design, and simplicity. However, it still adapts to local market preferences when necessary. For example, in China, Apple introduced larger screen sizes and enhanced camera functions for mobile gaming and selfies—key preferences among Chinese consumers—without diluting its global brand message of quality and innovation. This approach has allowed Apple to grow its market share in China without sacrificing the consistency of its brand identity.

Apple’s strategy demonstrates that true global consistency doesn’t require uniformity. It requires clarity of brand promise adapted across cultures.

The Global Challenge: Balancing Relevance and Global Consistency

Balancing global consistency with regional relevance is no longer optional; it’s a consumer expectation. Too much emphasis on relevance risks diluting brand identity, while rigid consistency can alienate local consumers. The key is to view relevance and consistency not as opposing forces but as complementary strategies that, when effectively managed, can drive both local and global success.

A recent Nielsen survey highlights this balancing act: 72% of global consumers expect brands to understand local preferences, but 68% still want a consistent global experience. This demonstrates consumers expect brands to adapt where necessary but without compromising the unified message that defines the brand.

Dove’s #RambutAkuKataAku Campaign in Indonesia

Image Source: INMOBI

Unilever’s Dove brand provides a perfect example of balancing relevance and consistency in Indonesia. Dove is globally recognised for its messaging around real beauty and body positivity, resonating with women worldwide. However, when Dove entered Indonesia, it realised that local cultural values and modesty required a more nuanced approach.

Campaign Idea:

In celebration of Kartini Day, Dove launched the #RambutAkuKataAku (My Hair My Say) campaign to empower Indonesian women to embrace their authentic selves through personal expression, particularly with their hair choices. Recognising the cultural significance of modesty in Indonesia, Dove tailored the campaign to respect traditional values while promoting self-confidence and real beauty. The campaign optimised nano influencers to submit their content in Kartini’s day and divided them into three main categories, Hijab, Normal hair and Unique Hair.

Approach: The campaign encouraged women across Indonesia to share stories about embracing their natural beauty, specifically through their choice of hairstyle and colour. Dove partnered with InMobi to amplify this message, using mobile platforms as the primary engagement channel. This strategy allowed women to easily participate by sharing their experiences, reinforcing Dove’s message of empowerment in a culturally sensitive way. The campaign resulted in 254 tweets, 400 photos submitted, 4,996,154 followers, and a 5.06% engagement rate.

Strategies for Achieving Relevance While Maintaining Global Consistency

Balancing relevance and consistency requires a strategic framework for flexibility within defined boundaries. Brands must develop a strong global identity while enabling local teams to make data-driven adaptations that resonate with their market.

To achieve both local effectiveness and global consistency, marketing leaders must take a structured yet adaptive approach. Here are some effective strategies for achieving this balance:

Establish a Clear Global Brand Identity: Define your brand’s non-negotiable elements—values, tone, and visual brand identity. These should remain consistent across all markets.

Empower Local Teams: Local marketing teams have critical insights into regional preferences, trends, and consumer behaviours. Empowering them to tailor campaigns within the global brand framework ensures relevance without fragmenting the brand.

Leverage Data for Smart Localisation: Predictive analytics and consumer sentiment analysis can guide brands on when to adapt versus stay consistent. Data can inform strategic decisions on how far to localise while keeping the core brand message intact.

Create Tiered Campaigns: Develop tiered marketing strategies, allowing for varying degrees of localisation. Global campaigns maintain consistency, regionally adapted campaigns reflect cultural differences, and highly localised campaigns address unique market needs.

Case Study: The “Thanda Matlab Coca-Cola” Campaign

Campaign Idea: Coca-Cola sought to maintain its global message of happiness and unity while adapting to the unique cultural contexts of India and China. In India, the brand launched the “Thanda Matlab Coca-Cola” campaign, positioning Coca-Cola as a refreshing drink shared with loved ones, aligning with the country’s strong cultural emphasis on family and togetherness. In China, Coca-Cola adapted its messaging to reflect the significance of the Lunar New Year, associating the drink with celebrations and family reunions.

Approach: In both markets, Coca-Cola localised its marketing to resonate with cultural norms while maintaining the consistency of its global brand message. In India, Coca-Cola used colloquial language and imagery to make the brand feel familiar and deeply connected to local traditions. In China, the brand aligned with the national celebration of the Lunar New Year, a major cultural event, by emphasising joy and family gatherings, key pillars of the holiday.

By tailoring messaging to local values while preserving its brand voice, Coca-Cola exemplifies how global consistency can accommodate cultural diversity.

When to Prioritise Relevance and When to Prioritise Global Consistency

Knowing when to prioritise relevance or consistency is key for international brand marketing. In emerging or culturally distinct markets, local relevance should take precedence. For example, launching new products in markets like Vietnam or Thailand requires an understanding of local values, such as ethical consumption or family-oriented themes.

However, in industries like luxury goods or technology, where global recognition is paramount, consistency should be prioritised. Consumers in markets like the US and UK expect the same high standards of quality and experience. During global crises or product recalls, consistent messaging is essential to preserve brand integrity and prevent confusion.

In the Philippines, for instance, brands that align with local values of family and community, such as food brands emphasising communal dining, outperform those that don’t.

However, in Thailand, where luxury consumers expect the same quality experience from brands like BMW or Mercedes-Benz, consistency in messaging and product experience is key to maintaining perceived value. The ability to recognise when to lean into relevance or consistency is critical to success.

In international marketing, success doesn’t come from choosing local relevance over global consistency. The most successful global brands strategically integrate both. Relevance allows brands to connect with local consumers by aligning with cultural preferences, while consistency ensures the brand remains recognisable and trustworthy across all markets.

For senior marketing leaders, the actionable takeaway is clear: define your core brand elements that should remain consistent globally and empower local teams to tailor campaigns for cultural relevance where they make the most impact. Use data-driven insights to guide these decisions, ensuring your brand stays relevant in diverse markets without losing its global identity.

As global consumers grow more connected, brands that master the balance between relevance and consistency will continue to thrive. It’s not about choosing one over the other, but about finding that equilibrium that creates a cohesive, trusted, and culturally resonant brand.

As a global market research agency with offices in ten countries, Kadence International is well-equipped to help you navigate the complexities of international expansion. Whether you need insights into local consumer behaviour, guidance on maintaining brand consistency, or support in crafting culturally relevant campaigns, we have the expertise to ensure your brand’s success. With our deep understanding of Western and Asian markets, we can provide the strategic insights you need to grow your brand globally. We help global brands achieve consistency in voice and identity while enabling the local relevance required to succeed in culturally diverse markets.

A recent McKinsey report states that global markets are responsible for over 80% of business growth. As companies expand their reach, the challenge of creating a value proposition that resonates across diverse cultural landscapes becomes increasingly critical.

A value proposition is a clear and concise statement explaining why customers should choose your product or service over others. It is the cornerstone of your brand’s messaging and positioning. In international markets, however, a poorly crafted value proposition can quickly fall flat, leading to misaligned messaging, cultural missteps, and, ultimately, lost revenue. The stakes are high, and businesses must precisely navigate these complexities to succeed globally.

Understanding the Cultural Landscape

The Influence of Culture on Consumer Perception

Cultural factors play a decisive role in shaping consumer perceptions, behaviours, and purchasing decisions. What appeals to consumers in one market may not resonate in another due to deeply ingrained cultural differences. For instance, a value proposition centred on individuality and self-expression might thrive in the United States, where individualism is highly valued. However, the same message could fall flat in markets like Japan or China, where collectivism and harmony with others are more culturally significant.

A prime example is IKEA’s entry into the U.S. market. Initially, IKEA’s minimalist, space-saving furniture resonated well in Europe, where smaller living spaces are common. However, in the U.S., where larger homes and more substantial furniture are preferred, IKEA had to adapt its value proposition by offering larger, more traditional furniture options. This adjustment allowed them to align better with American cultural expectations and consumer preferences, ultimately contributing to their success in the market.

Image credit: IKEA USA

Key Cultural Dimensions to Consider

To craft a value proposition that resonates across cultures effectively, it’s essential to consider key cultural dimensions. Hofstede’s cultural dimensions—such as individualism vs. collectivism, power distance, and uncertainty avoidance—offer a framework for understanding how different cultures interpret messages.

For example, in high-power-distance cultures like India, consumers may respond more positively to a value proposition emphasising authority and status. Conversely, in low-power-distance cultures like Denmark, where egalitarianism is valued, a proposition highlighting equality and community might be more effective.

Understanding these cultural dimensions allows businesses to tailor their value propositions to align with local values and norms. For instance, McDonald’s adapts its menu and marketing strategies to reflect local tastes and cultural preferences. In India, where a significant portion of the population is vegetarian, McDonald’s successfully introduced a range of vegetarian options that align with local dietary practices, ensuring its value proposition remains relevant and appealing.

Steps to Crafting a Global Value Proposition

Conducting Cultural Market Research

Thorough market research is the foundation of crafting a value proposition that resonates across different cultures. Understanding cultural differences and consumer preferences in your target markets is essential for creating messaging that connects authentically with local audiences.

To begin, gather qualitative and quantitative insights into the cultural landscape. Start with qualitative methods like focus groups and ethnographic research to gain a deep understanding of local consumer behaviours, values, and preferences. Surveys can provide quantitative data on consumer attitudes and purchasing patterns, helping you identify trends and potential areas of misalignment in your current value proposition.

Tools and resources are invaluable in this process. Consider working with international market research agencies, like Kadence International, who can provide on-the-ground insights. Cultural consultants can offer expertise in navigating complex cultural dynamics, ensuring your messaging is accurate and respectful. Additionally, online databases and tools like Statista can provide valuable data to inform your strategy.

Identifying Universal Needs and Pain Points

While cultural nuances are important, identifying universal consumer needs and pain points that transcend these differences is crucial. Successful global brands often find common ground by focusing on core human needs—such as convenience, safety, or quality—that appeal to consumers regardless of their cultural background.

However, balancing this universal appeal with localised messaging is critical. For example, Apple’s value proposition emphasises innovation and simplicity, which are universally appealing. Yet, Apple also tailors its marketing to reflect local cultural values. In China, where face and status are significant, Apple highlights the prestige associated with owning their products, while in Western markets, the focus might be more on individuality and creativity.

Tailoring the Message for Different Markets

Adapting your core value proposition to different cultural contexts without losing brand consistency is a delicate balancing act. Language, imagery, and messaging must align with local cultural norms and values to ensure the message resonates effectively.