Year-end sales numbers tell a reassuring story. Markets across the United States, the United Kingdom, and Asia appear steady, even buoyant in places. However, the surface resilience masks a more profound shift. Consumers are still spending — just not in the way headline figures suggest. Every choice is now filtered through a slower, more deliberate, more conditioned decision-making sequence.

Multiple global studies point to the same realignment. Shoppers enter the season with intent, yet proceed with far greater scrutiny. PwC finds that more than half of consumers say rising living costs have permanently altered how they spend, prioritising value and price over brand preference, even during peak promotions. This restraint is evident across regions, cutting through differences in market maturity and retail structure.

Digital behaviour makes this shift unmistakable. Adobe and Mastercard reporting shows shoppers researching more intensely, waiting longer, and concentrating spend within narrow windows. The season has become compressed and high-stakes: excitement may spark interest, but confidence drives conversion. In-store, the same discipline applies: tighter budgets, faster price comparisons, fewer impulse additions.

Consumers are not pulling back; they’re protecting themselves. They move through the season balancing celebration with caution, a behaviour that reveals how aspirations remain intact even as risk tolerance narrows, a defining characteristic of modern consumer spending.

Holiday Shopping Behaviour Shows Intent Remains High, but Commitment Is Delayed

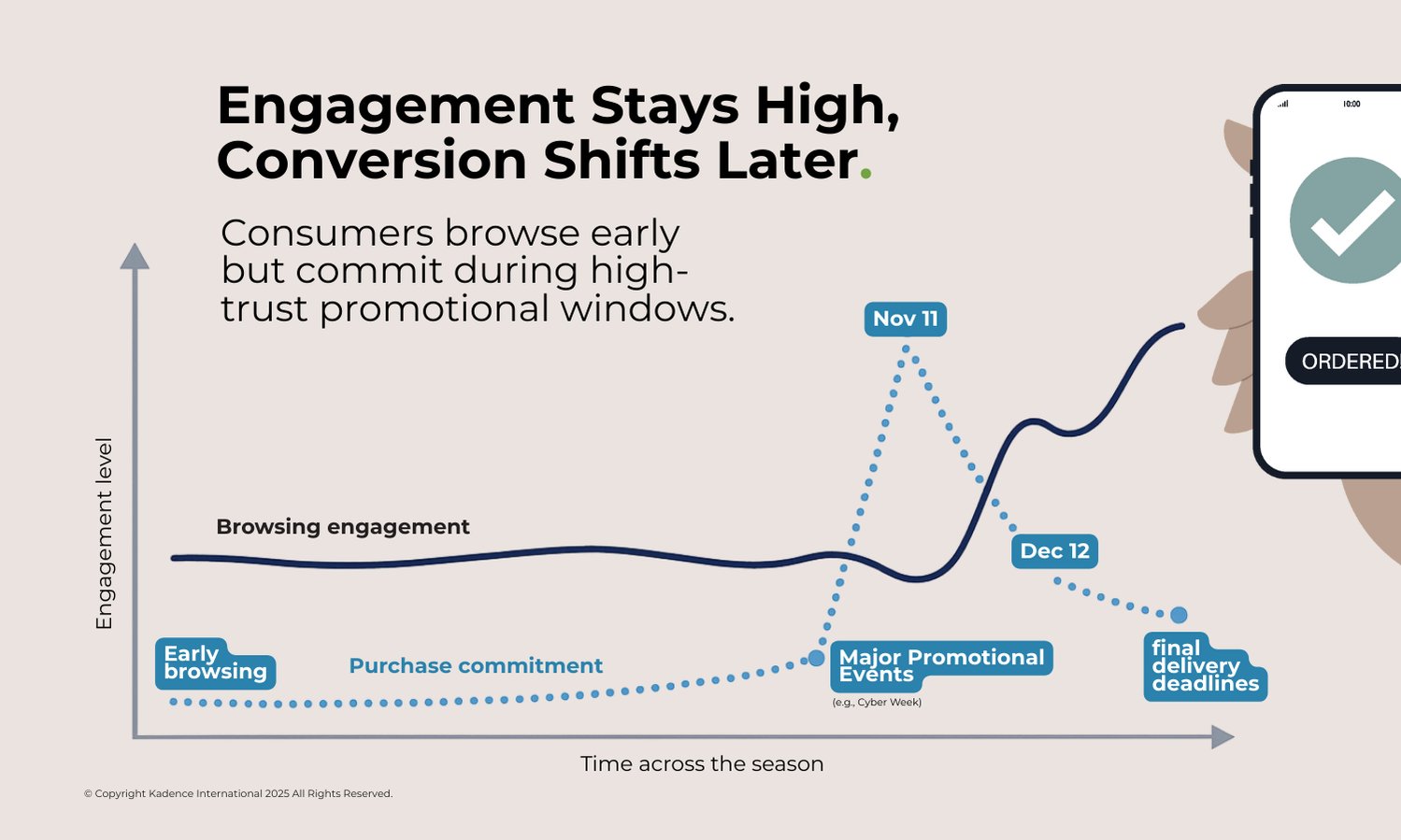

One of the clearest behavioural signals is the widening gap between interest and action. Consumers are engaging early but holding back until conditions feel right. Tracking studies across markets show rising pre-event browsing, open baskets left to monitor prices and alerts set for drops across multiple retailers. Engagement remains high throughout the season, yet conversions spike only within narrow promotional windows.

Adobe’s 2024 holiday data highlights how digital spending is becoming increasingly concentrated in short promotional periods. In the U.S. alone, Cyber Monday reached a record $13.3 billion in online sales, illustrating how prolonged research often culminates in brief, decisive buying moments. Mastercard SpendingPulse reinforces the same pattern, noting that much of holiday retail growth is driven by e-commerce and concentrated in digital event moments such as Cyber Week, when shoppers wait for clearer value cues. Salesforce data echoes this globally: more than 60 percent of online holiday sales occur during the top ten shopping days of the season, despite browsing beginning weeks earlier.

Strategic signal for brands: Forecasting must now model long consideration cycles and condensed conversion peaks, reshaping promotion calendars, inventory planning and last-mile operations.

Value Is Shaping Decisions More Than Volume

The most significant evolution in year-end behaviour lies not in how much consumers buy, but in how they assess worth. People are replacing casual additions with more intentional substitutions, guided by utility, longevity and perceived fairness.

Recent research points to consistent behaviours:

- Essential categories are protected, while non-essentials are evaluated more rigorously.

- Brand switching increases when price gaps widen.

- Consumers reduce quantity but stay engaged.

- Multi-use items outperform single-purpose purchases.

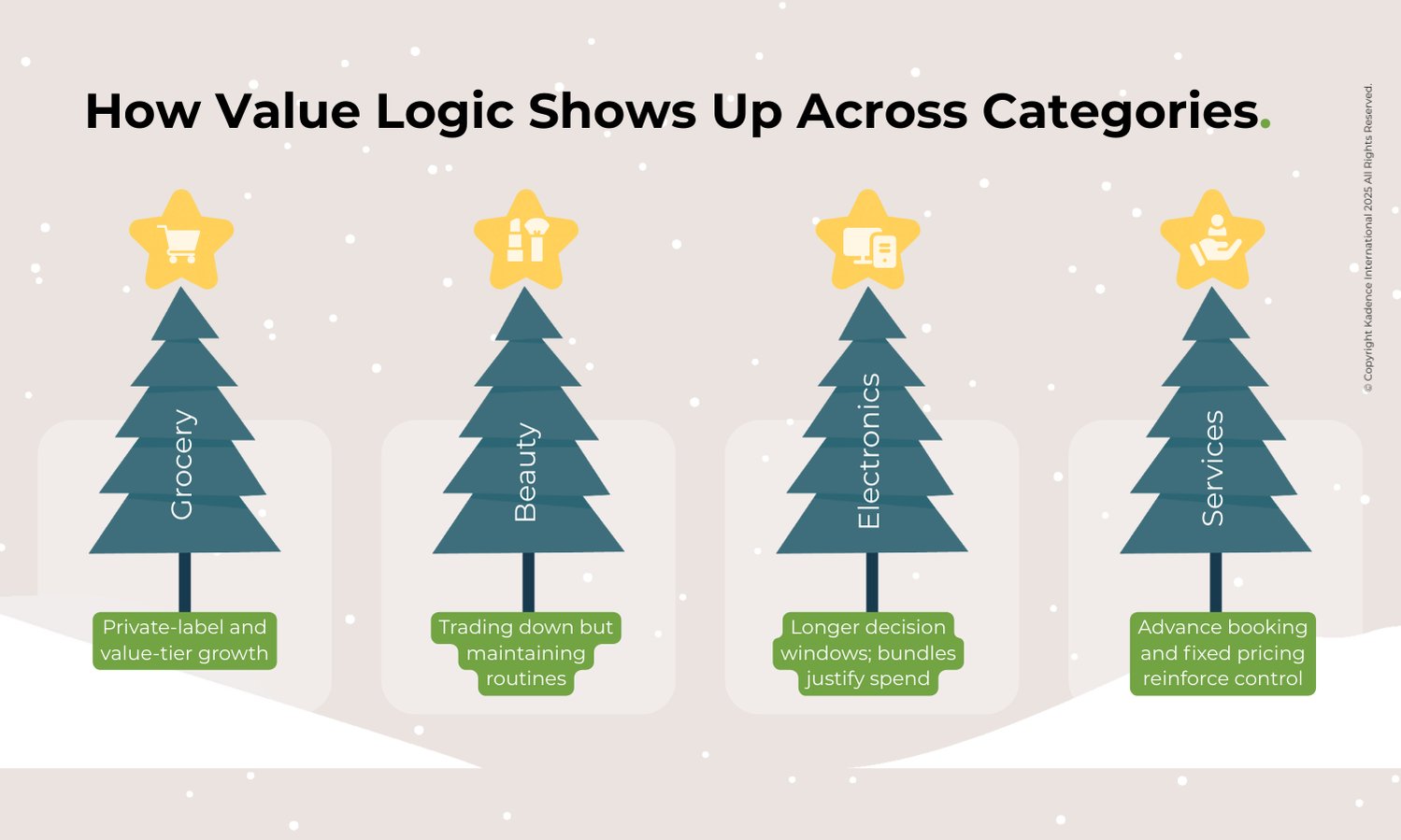

This shift is visible across categories:

- Grocery: In the UK, value-tier products and private labels continue gaining share as households prioritise predictability.

- Beauty and personal care: US consumers trade down within brands while maintaining routines, reflecting protection of emotional-value categories.

- Electronics: In India and Southeast Asia, decision windows are lengthening, and bundles or extended warranties are influencing purchasing decisions.

- Services: In travel and dining, consumers maintain participation but favour advance bookings, fixed bundles, and transparent pricing — extending the same value logic beyond retail.

People no longer evaluate purchases against seasonal norms; they evaluate against their own thresholds of reasonableness.

Strategic signal for brands: Novelty alone holds less influence. Transparent pricing, straightforward utility and credibility do more to secure a place in the consumer’s short list.

Promotions Now Function as Permission, Not Persuasion

Promotions still move the market, but their function has changed. Discounts serve less as incentives and more as signals that it is safe to act.

Global studies show consumers becoming increasingly sceptical of inflated reference pricing and constant markdowns. They respond most strongly to promotions that are:

- Clear

- Time-bound

- Linked to established shopping moments

- Supported by transparent price histories

This pattern appears in both high-frequency event markets and traditional retail environments. When discounting becomes ambient rather than exceptional, its signalling power weakens.

Strategic signal for brands: Promotions must act as confidence boosters, not noise. Timing, transparency and credibility matter more than the discount itself.

Flexible Payments Influence Timing More Than Total Spend

The expansion of instalment and buy-now-pay-later (BNPL) options is often interpreted as a sign of financial strain. Yet public data tells a more complex story. Adoption continues to rise. The Federal Reserve reports that around 15 percent of US adults used BNPL in the past year, but evidence on how these tools shape spending is mixed. Some studies link BNPL to higher-order values, while others show that consumers use it selectively to manage affordability and timing.

What is clear is the psychological role instalments play. Spreading payments into predictable increments lowers the immediate burden associated with a purchase, making the transaction feel more manageable, even when the total spend remains unchanged. For households navigating tight affordability thresholds, this reassurance can be the difference between postponing and converting.

Patterns vary across regions. In Southeast Asia, where super-app ecosystems have normalised instalments for years, payment flexibility is woven into everyday commerce. In Western markets, BNPL tends to function as a budgeting tool for specific purchases rather than a wholesale replacement for credit; however, regulators and researchers continue to monitor potential risks, such as late payments or loan stacking.

The behavioural signal is not about increased spending but about increased need for control. Consumers are using flexible payments to align purchases with their internal sense of affordability, smoothing the moment of commitment rather than enabling unchecked demand.

Strategic signal for brands: Framing instalment options as clarity tools, not as incentives, will better align with how consumers use them. Payment flexibility provides reassurance at the point of decision and supports conversion, but it should not be viewed as a means to expand demand artificially.

Caution Has Become a Global Baseline, Expressed Through Local Habits

While cultural and structural differences persist, the year-end season shows convergence in the underlying emotional posture: consumers are managing risk, not abandoning consumption.

- United States: Caution manifests in timing — delayed action, heightened price checks, and tactical switching across channels.

- United Kingdom: Prioritisation is sharper, with households protecting essentials and substituting readily when prices exceed tolerance.

- China, India and Southeast Asia: Digital engagement remains strong, but purchases concentrate on high-trust campaign days, bundles and formats that optimise efficiency and value.

- Latin America and the Middle East: High engagement but a preference for clear event days and transparent pricing, reinforcing the broader global shift.

Across all regions, confidence recovers slowly and unevenly. People respond to lived cost realities more than macroeconomic signals.

Strategic signal for brands: Global strategy must reflect a universal desire for control. Messaging and timing should align with risk-managed decision-making.

What the Year-End Season Reveals About the Future Consumer

The year-end period has become a compressed preview of how consumers behave under sustained uncertainty. Early information gathering, delayed commitment, value filtering and compressed demand are now structural behaviours, not seasonal anomalies.

Consumers operate through a confidence-gated decision cycle, evaluating purchases through four thresholds:

- Relevance — Does it matter now?

- Fairness — Is the price defensible?

- Timing — Is this the right moment to act?

- Risk — Will I regret this later?

This cycle allows aspiration to coexist with discipline. Rituals of celebration remain intact, but consumers are less willing to carry uncertainty on behalf of brands.

As economic pressures persist, these frameworks will likely become more rigid. Brands that rely on habitual loyalty or constant stimulation will see diminishing returns; those built on clarity, reliability, and value-backed propositions will gain ground.

Strategic signal for brands: As these behaviours settle, companies may need to redesign promotional calendars, rethink how value is communicated and reassign inventory cycles to accommodate sharper peaks and longer evaluation phases. The future consumer is no less ambitious; they are more deliberate in their approach.

Understanding when consumers hesitate is now as important as knowing what they want. At Kadence International, we partner with brands globally to decode the decision-making pressures shaping behaviour across markets and moments. To explore how these shifts are unfolding in your category or region, get in touch.