Food and beverage leaders continue to prioritise younger consumers, even as the real spending power sits elsewhere. Overlooking that shift now carries real strategic risk. Generation X commands roughly USD 15.2 trillion in global expenditure, with regional spending power visible across markets from rising middle-income households in the Asia Pacific to Gen X’s position as the highest-spending generation in the UK and the strongest CPG spenders in the US across grocery categories. Their influence is increasing even as they remain largely absent from brand agendas.

Economic and demographic forces explain their weight. Gen X is entering its peak earning years while supporting multi-generational households, giving them a steady and diversified presence across food, beverages, household care, and pet categories. Their choices, rooted in routine and reliability, generate predictable demand and contrast sharply with the faster, less consistent swings in younger cohorts.

Yet they remain under-represented in product development and channel strategy. Innovation continues to skew toward Millennials and Gen Z. At the same time, many of the formats where Gen X shows strong penetration — club stores, mainstream grocery, convenience retail, and digital content channels — do not always receive investment proportionate to this cohort’s economic weight. As inflation, cost pressures, and shifting meal routines reshape margins, the gap between their importance and their visibility has become increasingly difficult to justify.

For global food and beverage brands, the goal is not to reduce focus on younger consumers but to correct the persistent underweighting of the generation with the most resilient spending fundamentals. Understanding Gen X’s habits, motivations, and channel patterns will be essential for unlocking growth over the next decade.

How Gen X Shops for Food and Beverage Products

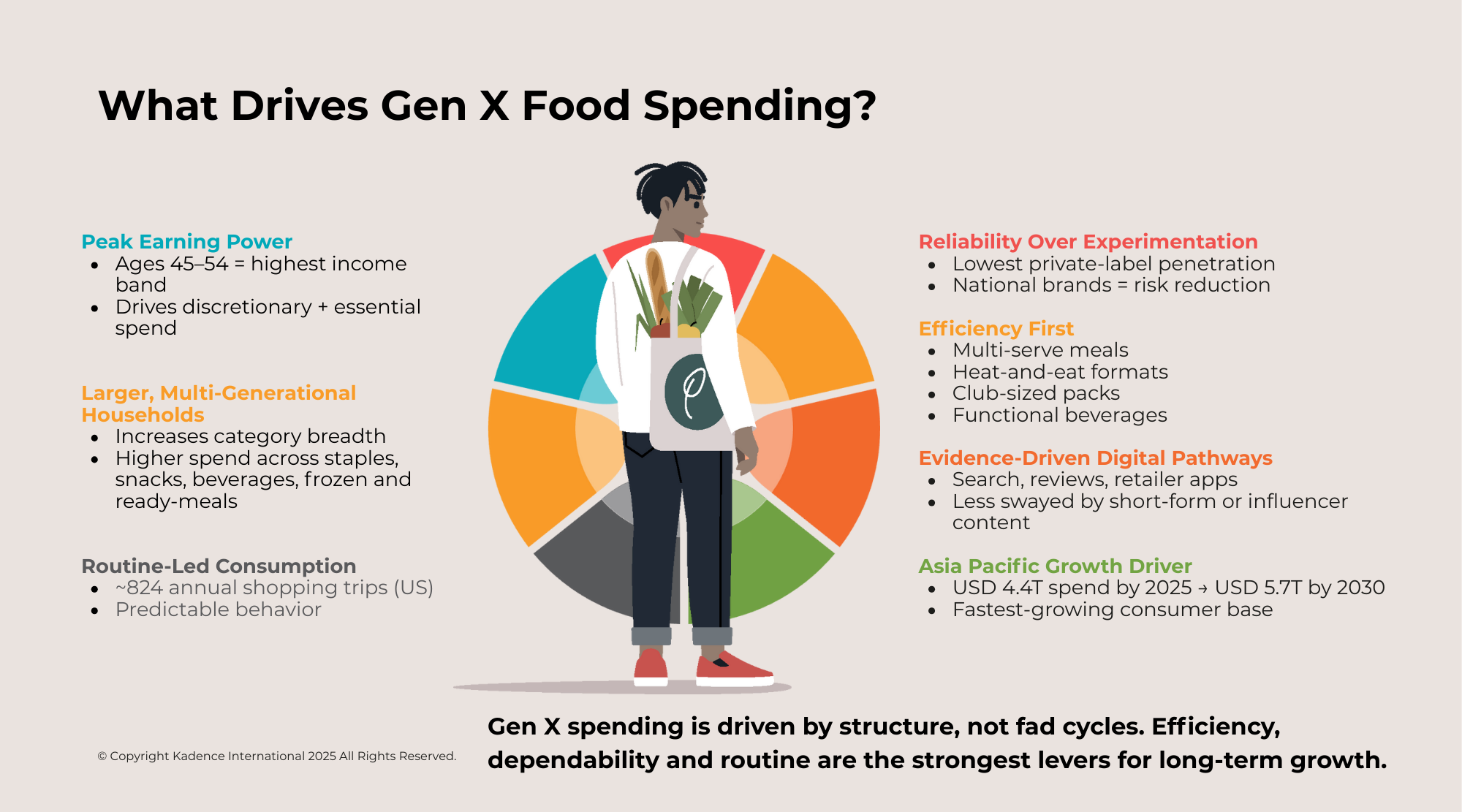

Gen X’s food and beverage decisions diverge clearly from both younger and older cohorts. One distinct signal is the breadth of their shopping activity. A US study reveals that Gen X households undertake approximately 824 CPG shopping trips per year, a routine that combines planned stock-ups with frequent top-ups across various channels. This surpasses all other generations on a per-household basis.

Their brand selection behaviour is another point of differentiation. In the US, Gen X shows the lowest private-label penetration of any generation, favouring national brands for their consistency and reduced trial-and-error risk, especially in categories where failed purchases cause household disruption, such as children’s snacks, ready meals, beverages and pet food.

Category engagement underscores a tilt toward practical optimisation. Compared to Millennials, Gen X allocates a larger share of its spend to items that reduce operational load, such as multi-serve frozen meals, heat-and-eat formats, functional beverages, and club-sized staples. These choices are less about narrow convenience and more about reducing the day-to-day burden of managing a household.

Digital behaviour further distinguishes the cohort. They use online grocery and retail platforms extensively, but their discovery pathways differ: search, reviews, and retailer recommendations carry greater influence than influencer-led or short-form content. As a result, their purchase patterns are more evidence-driven and less responsive to rapid shifts in platform culture.

Across markets, one theme stands out: Gen X buyers make decisions rooted in efficiency, dependability, and clear product value. These behaviours create a broad and stable demand base, reinforcing their role as a core engine of volume and repeat purchasing for food and beverage companies.

Gen X Food Spending Trends That Will Shape the Next Decade

Gen X’s position at the top of global food and beverage spending reflects durable structural forces rather than temporary shifts.

Income distribution is the first. Across developed markets, earnings peak between ages 45 and 54, placing Gen X at the highest point of the wage curve and giving them more discretionary and non-discretionary spending power than both Millennials and Boomers.

Household composition is the second driver. While younger generations trend toward smaller households, Gen Xers often maintain larger units that span multiple age groups, especially in many Asian markets. This structure increases consumption across staples, snacks, beverages, and meal solutions in a manner that is less sensitive to economic fluctuations. Between 2025 and 2030, Gen X is projected to contribute USD 507 billion to global food and non-alcoholic beverage spending, with the Asia Pacific accounting for more than half of that growth.

Geography further amplifies their role. Gen X comprises a significant share of middle- and upper-middle-income consumers across North America, Western Europe, and key Asian markets. In the Asia Pacific, the cohort is projected to spend USD 5.7 trillion by 2030. In rising middle-income markets such as Southeast Asia, Gen X is expanding spending faster than other cohorts, giving the region a balanced global footprint.

Cost structure completes the picture. Categories with recurring purchase cycles, such as staples, packaged meals, and functional beverages, depend on consumers with consistent shopping patterns. Gen X’s high shopping frequency and broad category participation provide a foundation of predictable revenue that stabilises manufacturers and retailers during inflationary or supply-volatile periods.

Taken together, these forces make Gen X the most economically consequential cohort for the sector over the next decade. Their leadership stems not from trend-driven surges but from durable economic and demographic conditions that underpin category stability and long-term growth.

Asia Pacific

The Asia Pacific region is crucial for this cohort, as 61% of the global Gen X population resides there, with 37% being in China alone. In these markets, Gen X anchors rising middle-income households, especially in Indonesia, Vietnam, and the Philippines, where income mobility has accelerated over the past decade. This cohort drives packaged food growth, ready-meal adoption, and functional beverages, categories where convenience and reliability carry substantial weight.

Japan illustrates the impact of demographic structure on spending. Government household expenditure data shows that Gen X households spend around 12% more on packaged foods than the national average, reflecting the need to balance long working hours with domestic routines.

.png?width=2000&height=1111&name=Japan%20Gen%20X%20Households%20Spend%20More%20on%20Packaged%20Foods%20Than%20the%20National%20Average%20(1).png)

Southeast Asia shows a different dynamic: Gen X’s willingness to pay for quality when it reduces daily friction. Convenience chains in Taiwan, South Korea, and Thailand report sustained growth in fresh bento, ready-to-eat meals, and premium snack categories among consumers in their forties and fifties, driven by work-centric routines and multi-stop shopping behaviour.

Case Study: FamilyMart Taiwan and Fresh Meal Expansion

Image credit: Vending Times

FamilyMart Taiwan’s expansion of its fresh meal and ready-to-eat programme illustrates how urban Gen X drives quality-led convenience across Asia. Company disclosures for 2024 reveal growth in sales of fresh bentos and ready meals. The company attributed overall sales increases to strong performance in ready-to-eat meals. It noted that Taiwan’s bento and buffet sector grew by 22 percent from January to September 2024, signalling a broad market shift toward convenient, quality-driven formats.

FamilyMart Taiwan’s total consolidated revenue for the year ending December 31, 2024, showed a 5.5 percent increase from the previous year. Net profit more than doubled. The company highlighted its differentiated fresh food strategy and cross-category collaborations as central to meeting consumer demand and sustaining growth. These attributes map to Gen X decision logic: predictable flavour profiles, transparent ingredients, and reliable availability. The programme’s performance demonstrates how convenience formats that combine quality and efficiency can secure sustained demand from this cohort across the region.

North America and Western Europe

In Western markets, Gen X anchors the most dependable share of grocery spending. Panel data indicate high annual expenditure on staples, packaged meals, snacks, and beverages, reflecting entrenched household responsibilities and long-standing shopping patterns.

New evidence from the UK reinforces this pattern. In commentary and regional forecasts, NIQ and World Data Lab note that in high-income markets, including the UK, Gen X’s spending dominance is likely to persist longer than in lower-income countries.

In the US, Gen X plays a decisive role in club stores, mass retailers, and mainstream grocery, favouring multi-pack value, recognisable brands, and efficient environments. In the UK and Germany, similar patterns emerge, with Gen X remaining a core segment for supermarket chains, where upgraded staples and mid-premium pantry items exhibit steady growth.

Case Study: Costco and Gen X Basket Strength

Image Credit: LinkedIn

Costco’s membership and transaction data show that members aged 45 to 59 maintain some of the highest renewal rates, above 90 percent, and the largest average basket sizes. Their preferences for bulk packs, established brands, and predictable product quality strengthen warehouse formats dependent on repeat purchasing, explaining Gen X’s central role in mass retail performance across North America and parts of Europe.

What Gen X Wants from Food and Beverage Brands

Gen X’s expectations are grounded in practical constraints rather than identity-led consumption. Their decisions consistently reward products and experiences that remove friction from daily life.

Reduce operational load.

Multi-serve meals, heat-and-eat formats, frozen items, and club-sized staples help streamline meal routines without sacrificing outcomes.

Deliver consistent quality.

For Gen X, quality means reliability: stable formulations, predictable performance, and products that work the same way every time.

Support balanced eating without complexity.

Better-for-you snacks, functional beverages, and fortified staples resonate when they integrate seamlessly into daily routines.

Price with logic.

Gen X rejects pricing detached from functional value. Transparent unit economics and multi-occasion utility outperform promotional churn.

Across categories, Gen X rewards brands that simplify everyday consumption and reduce uncertainty. Their logic is grounded in clarity, proven performance, and functional benefits rather than novelty.

Brand Strategies That Win with Gen X

These strategies translate Gen X’s expectations into commercial action for food and beverage brands.

Prioritise value-driven innovation.

Innovation resonates when it improves efficiency or dependability. Upgraded staples, functional beverages, and practical meal solutions outperform novelty-led launches that require behavioural change.

Strengthen high-concentration channels.

Club stores, mass retail, mainstream grocery, and functional digital pathways — such as search, retailer platforms, and long-form product reviews — are where Gen X demonstrates clear buying intent.

Use clear, functional messaging.

Messaging should highlight predictable outcomes, time-saving advantages, and ingredient clarity. Over-stylised or aspirational narratives carry less weight without tangible proof of value.

Build for repeatability and long-term value.

Stable formulations, reliable availability, and pricing structures that reward larger pack sizes increase retention and lift lifetime value.

Balance price and performance.

Gen X prioritises practicality, durability, and household suitability over symbolic premiums. Premiumisation is effective when tied to functional improvement.

Key Takeaways for Brands

For F&B product leadership teams navigating inflation, supply variability, and shifting meal habits, these priorities offer a disciplined framework for aligning near-term gains with long-term growth. These priorities translate Gen X’s behaviours and strategic value into leadership guidance.

Gen X is the most stable demand base in a fragmented landscape.

Routine-led purchasing and broad category participation drive predictable revenue across the sector.

Value-led product design should guide innovation pipelines.

Efficiency, reliability, and multi-occasion use deliver higher repeat purchasing and more durable returns.

Channel precision is essential.

Strengthening assortment, availability, and messaging across preferred formats — including club stores, mass retail, mainstream grocery, and functional digital pathways — generates disproportionate commercial impact.

Gen X has become the driving force of the global food and beverage sector. As the industry confronts volatile supply chains, rising cost structures, and increasingly fragmented consumer demand, this cohort remains the only source of stable, repeatable growth at scale. Leaders who reorient strategy toward Gen X will strengthen their ability to plan, price, and innovate with confidence. Those that continue to prioritise younger consumers at the expense of the generation with the most resilient spending fundamentals will face growing pressure on share, loyalty, and long-term profitability. In a market where predictability is quickly becoming a competitive advantage, Gen X will distinguish between the brands that endure and those that fall behind.