In 2023, more people moved to Charlotte, North Carolina than to New York City. Once known primarily as a banking hub, Charlotte is now among the fastest-growing metropolitan areas in the United States, with its population increasing by over 15% in the past decade. Its rising appeal is part of a larger pattern: a quiet but powerful migration away from megacities to what demographers call “secondary cities.”

This isn’t just an American phenomenon. Across global markets, from India to the UK to Southeast Asia, mid-sized cities are absorbing growth once concentrated in capital centres. In India, cities like Coimbatore and Ahmedabad are drawing IT investments and retail developments. In China, Chengdu has added more new retail space than many first-tier cities, and consumer spending in tier-2 urban areas is growing at a faster pace than in Beijing or Shanghai.

Affordability is a clear driver. As housing prices and costs of living continue to rise in the world’s biggest cities, residents and businesses are seeking out more livable alternatives. But what’s notable is that consumption isn’t declining as people move. In fact, recent data from McKinsey shows that residents of US secondary cities are just as likely to spend on premium goods and services as their peers in larger cities. The same is true in markets like Vietnam and Indonesia, where new urban enclaves are seeing surging demand for fast fashion, electronics, and beauty products.

This shift challenges a long-standing assumption: that consumer growth follows the gravitational pull of megacities. Instead, smaller urban centres are establishing themselves as independent engines of demand. They are not satellite economies or overflow markets—they’re increasingly self-sustaining hubs with distinct consumption patterns, retail ecosystems, and growth trajectories. Understanding these evolving dynamics isn’t just about tracking migration. It’s about recognising where the next wave of market opportunity is taking shape.

The Urban Migration Redrawing Consumer Behaviour

The reasons behind this urban realignment are pragmatic. In the United States, the average rent for a one-bedroom apartment in New York City now exceeds $3,000 a month. In contrast, cities like Raleigh or Nashville offer not only lower housing costs but also rising job opportunities and improved quality of life. Remote work has made this trade-off possible for millions. According to US Census data, more than 8.2 million people relocated across state lines in 2023, and the majority moved away from the country’s most expensive urban centres.

In the UK, London saw net domestic outflows in every quarter of 2023, as younger workers and families opted for cities like Birmingham and Manchester, where housing is more affordable and infrastructure investments have been accelerating. A similar pattern is unfolding across Europe and parts of Southeast Asia, driven by both economic necessity and post-pandemic lifestyle recalibrations.

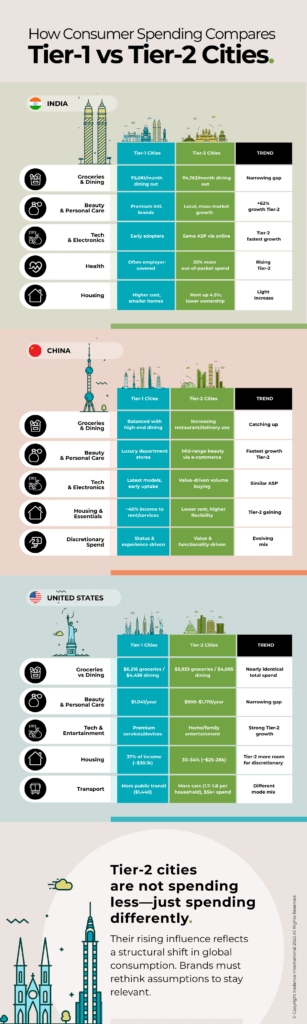

China’s urban development offers a sharper example. For over a decade, the central government has actively promoted growth in tier-2 and tier-3 cities as a way to reduce overreliance on Beijing, Shanghai, and Shenzhen. Chengdu and Hangzhou have emerged as digital and cultural hubs in their own right, attracting tech startups, luxury retailers, and young professionals seeking lower living costs and less congestion. Between 2010 and 2020, Chengdu’s GDP more than doubled, and consumer spending rose in parallel.

India’s Smart Cities Mission, launched in 2015, is another case study in how policy can redirect population and spending patterns. The initiative, aimed at improving infrastructure and governance in 100 mid-sized cities, has already resulted in faster retail expansion in places like Indore and Bhubaneswar than in Mumbai or Delhi. According to the India Brand Equity Foundation, consumer electronics sales in tier-2 cities grew by 23% year-on-year in 2023, outpacing metropolitan areas.

What links these movements is not a retreat from consumption but a reshaping of it. Consumers in secondary cities aren’t pulling back; they’re reallocating their spending. Travel, home improvement, wellness, and personal tech are among the categories seeing strong growth. Rather than dining out five nights a week, they may invest in premium groceries or upgrade their living space. Rather than fast fashion hauls, they’re choosing higher-quality basics from emerging local brands.

The geography of consumer demand is no longer centred on a few megacity powerhouses. It’s diffusing across a wider map—one defined by affordability, connectivity, and rising expectations. This new distribution isn’t temporary. It reflects a deeper recalibration in how people want to live and what they choose to prioritise when they have more control over where they are.

Rising Cities to Watch Across Global Markets

The rebalancing of population isn’t just reshaping where people live—it’s altering the architecture of consumption. Cities that once played a secondary role in national economies are now driving demand across key categories, from beauty and electronics to groceries and home improvement. These are not temporary trends. They reflect long-term investments, shifting demographics, and the redistribution of growth across geographies.

In India, urban expansion is no longer confined to Delhi, Mumbai, or Bangalore. Mid-sized cities like Ahmedabad, Kochi, and Coimbatore are seeing a surge in both population and retail development. Ahmedabad, now part of India’s key freight and industrial corridor, is drawing major logistics and manufacturing investment, boosting both employment and disposable income. Kochi, a port city historically associated with trade, is evolving into a service economy with rising demand for consumer goods, even as its organised retail recovery lags behind some peers. In Tamil Nadu, Coimbatore’s industrial economy has been buoyed by its emergence as a textile and engineering hub, contributing to increased uptake of electronics, fast fashion, and D2C brands among its aspirational middle class.

In China, government-backed decentralisation has helped elevate cities like Chengdu, Wuhan, and Hangzhou into powerful regional markets. Chengdu’s GDP surpassed 2 trillion yuan in 2023, underpinned by thriving sectors such as tech services, gaming, and high-end dining. Wuhan, long known for its manufacturing base, is diversifying into optoelectronics and biotech, helping shift consumer demand toward health and wellness products. Meanwhile, Hangzhou—home to Alibaba and a growing number of innovation hubs—continues to drive premium consumption, particularly among younger professionals seeking upgraded personal care, fitness tech, and lifestyle products.

In Southeast Asia, a cluster of cities is quietly gaining ground. Da Nang, once considered peripheral to Hanoi and Ho Chi Minh City, has logged annual growth over 6% on the back of a booming service economy and increased tourism-linked retail. Surabaya, Indonesia’s second-largest city, saw retail sales top $100 billion in 2023, as more middle-income households gained access to modern trade and e-commerce. In the Philippines, Cebu posted a 6% increase in GDP last year, with infrastructure and tourism projects spurring demand for beauty, packaged food, and mobile tech.

In the US and UK, the shift away from megacities is most visible in cities like Charlotte and Austin, where population growth and GDP expansion have outpaced the national average. Charlotte has attracted a steady influx of residents and companies, with population now nearing 3 million and median retail prices having risen more than 50% over the last decade. Austin led US metro areas in GDP growth in 2023–24, thanks in part to its dual reputation as a tech and cultural capital. Across the Atlantic, Birmingham has attracted new retail entrants and commercial investment, while Bristol—one of the UK’s fastest-growing core cities—is seeing a younger demographic drive e-commerce and convenience spending trends.

What unites these cities is not their size, but their trajectory. They’re absorbing the momentum once monopolised by megacities, and in doing so, are becoming primary battlegrounds for brands competing across FMCG, luxury, and tech. Each reflects a different facet of a global shift toward distributed growth—one that rewards those who understand the nuances of local demand, not just national averages.

How Consumption Patterns Differ from Megacities

What’s emerging in these secondary cities isn’t just a new geography of growth—it’s a different style of consumption. While the megacities have long been the testing grounds for innovation, image-driven luxury, and niche categories, smaller urban markets are shaping demand through a blend of aspiration and pragmatism. Consumers in these cities are not necessarily spending less; they’re spending differently—guided by function, value, and a growing sense of local identity.

In these rising hubs, premiumization often takes on a more practical form. Rather than high-concept luxury or limited-edition drops, there’s stronger traction for what might be termed “everyday upgrades.” Products that offer quality, longevity, and status without signalling excess are gaining ground. In the US, for example, Uniqlo’s decision to expand into cities like Austin and Charlotte aligns with this mindset. The brand’s clean aesthetic, moderate price point, and reputation for functional basics resonate in markets where value is prized, but style isn’t overlooked. These are not anti-fashion cities—they simply reject the transience and markup that characterises fashion in New York or Los Angeles.

In China, L’Oréal has tailored its go-to-market strategies accordingly. The company segments its product lines and retail mix not just by income level, but by geography. In tier-1 cities, its high-end lines dominate marketing spend, while in tier-2 and tier-3 locations, there’s more emphasis on skincare basics with scientific credibility and accessible pricing. Offline retail formats also shift—with pop-up stores and mobile beauty trucks seeing greater success in secondary cities where e-commerce growth hasn’t yet plateaued, and where physical presence still builds trust.

One factor that consistently shapes behaviour in these markets is the multi-generational household. In many Indian and Southeast Asian cities, discretionary income is often pooled across family units. That influences purchasing decisions across categories—from appliances to packaged food—prompting brands to market not just to individuals, but to households as collective consumers. There’s also a preference for products that serve dual or extended purposes: tech gadgets that function across work and leisure, food brands that cater to both tradition and convenience, and beauty products positioned around self-care rather than indulgence.

There is, however, no uniform pattern. In the Philippines, the growth of Korean skincare brands in cities like Cebu is as much about digital influence as affordability. In Birmingham, the return of legacy department stores is tied to nostalgia and civic pride as much as retail demand. And in Chengdu, the rise of lifestyle cafés and boutique gyms reflects a younger population that wants access to the symbols of metropolitan living—without the daily grind of Beijing.

These cities are not diluted versions of their larger counterparts. They are developing their own consumer signatures, shaped by local infrastructure, employment patterns, and cultural nuance. For brands and strategists, the challenge lies in abandoning the notion of a one-size-fits-all urban consumer. The goal is no longer just market entry—it’s market fluency. And increasingly, fluency in these smaller, faster-growing cities may prove more valuable than reach in the capitals.

Implications for Brands

The changing face of urban demand calls for more than just expansion—it requires recalibration. As secondary cities gain economic influence, many of the assumptions that once shaped brand strategy are no longer reliable. Markets that were once considered peripheral now demand bespoke planning, grounded in the specifics of place rather than the generalities of national averages.

One immediate shift is the need for greater geographic precision in research. National surveys and tiered segmentation models often flatten regional nuance, failing to capture the complexity of cities like Coimbatore or Chengdu. For companies reliant on trend forecasting or demand modelling, that means moving from regional sampling to localised data capture, often city by city.

Product development and inventory planning are also evolving. In India, brands like Mamaearth and Plum are adjusting their SKUs for tier-2 and tier-3 cities, shifting from large-format products to smaller, trial-sized offerings that match local price expectations. In the US, national retailers like Target have refined their assortments in cities like Charlotte and Nashville, prioritising core everyday goods while reducing premium or seasonal inventory that underperforms outside the major metros.

Media planning is undergoing a parallel transformation. As digital access expands in emerging urban centres, traditional broadcast budgets are giving way to city-level targeting across mobile platforms and social commerce channels. Short-form video, regional influencers, and WhatsApp-based promotions are becoming more effective in places where ad fatigue hasn’t set in and trust in peer-to-peer recommendations remains high. In markets like Vietnam, TikTok is now the primary discovery channel for beauty and electronics purchases in cities outside Hanoi and Ho Chi Minh City, according to recent industry data.

Even logistics, often treated as an operational concern, is now central to brand reputation in smaller cities. The rise of same-day and next-day delivery expectations—previously confined to tier-1 cities—is now common in places like Cebu or Bristol. For many brands, the challenge isn’t reaching these markets, but reaching them reliably. That’s led to increased partnerships with regional fulfilment services, and in some cases, internal investments in micro-warehousing and localised dispatch.

This redistribution of consumer power is forcing brands to move beyond scale and standardisation. The era of national uniformity in messaging, product lines, and delivery models is fading. In its place is a more fragmented but arguably more dynamic landscape—one where understanding the pulse of smaller cities is becoming essential to staying relevant in the broader market. Brands that treat these urban centres as strategic priorities, not afterthoughts, will be the ones best positioned to grow as the next wave of consumer demand continues to take shape outside the old capitals.

The Future Is Smaller, Faster, and Closer Than You Think

The cities driving the next era of global consumption won’t always be the ones on postcards. They won’t host the Olympics or top the rankings for financial centres. But they will be where new preferences are formed, where loyalty is won, and where growth happens quietly until it isn’t quiet anymore.

This is not a temporary correction or a cost-of-living workaround. It’s a structural shift. In many ways, secondary cities are better attuned to the values shaping modern consumerism: access, flexibility, and balance. These are places where people can afford to live and choose how they spend, not just how much.

For brands, the path forward lies in proximity—not just geographic, but cultural. Success will depend less on scale than on sensitivity. Less on dominating share of voice in capital cities, and more on understanding how tastes evolve in places that rarely make headlines but increasingly make markets.

The middle is no longer a middle ground. It is the next frontier. And those who invest in it early will not just meet new demand—they’ll define it.

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Senior Marketing Executive

Senior Marketing Executive Sales & Marketing

Sales & Marketing General Manager PR -Internal Communications & Government Affairs

General Manager PR -Internal Communications & Government Affairs