British shoppers are entering a new era of grocery buying – less impulsive, more deliberate, and increasingly shaped by price. Grocery inflation rose to 3.5 percent in March, capping off two years of compounded cost pressure. Supermarket sales have softened, not because people are walking away, but because they’re buying fewer items and skipping anything that doesn’t feel essential.

Essentials are winning, volume is shrinking, and price has become the lead story. This shift isn’t just thrift – it’s agency. After months of rising bills and economic fatigue, shoppers are regaining a sense of control by editing their baskets. That often means skipping branded goods and sticking to private labels.

Discounters are reaping the gains. Aldi’s market share is up to 11 percent, and Lidl is outpacing rivals in sales growth. But this isn’t just about who’s winning – it’s about how. Shoppers aren’t compromising; they’re recalibrating. Value now means quality at the right price, not a badge name. What’s happening isn’t tactical – it’s behavioural.

What distinguishes this period from past inflation spikes is the speed and confidence of the switch. Brand loyalty, long considered a mainstay of British retail, is now a conditional contract. If a supermarket can’t justify its price point – through quality, loyalty perks, or convenience – shoppers will walk.

Retailers are moving fast to keep up: shrinking private-label ranges to what works, tuning promotions, and reframing value as a daily promise. On paper, it looks like a margin problem. In reality, it’s a permanent shift in how households define value – and there’s little reason to think it’ll snap back.

This isn’t a belt-tightening moment. It’s a consumer reorientation. People aren’t just buying less; they’re buying differently. And in doing so, they’re quietly forcing a reset in how the UK grocery industry defines, delivers, and earns loyalty.

Inflation at the Checkout: What’s Really Driving the Shift?

Walk through any UK supermarket right now, and the change isn’t just in the receipt – it’s in the way people are shopping. Labels are read more slowly. Own-brand products are picked up, put back, then chosen again. Familiar items suddenly feel like indulgences.

What’s happening at the checkout isn’t just about price increases. It’s a psychological shift. Shoppers aren’t just spending less – they’re thinking differently. The same budget now feels tighter, not only because of higher prices but because of how those prices are being perceived.

Anchoring is one reason. Consumers aren’t comparing this week’s price to last week’s – they’re comparing it to what they used to pay before “everything got expensive.” That reference point, even if outdated, sticks. When a block of cheese crosses the £3 mark, it doesn’t matter if it’s only a 5p rise – it’s crossed an invisible line. And that line reshapes everything around it.

Mental accounting adds another layer. People are rebalancing invisible budgets in their heads. Spend £2 more on milk, and that £2 has to come from somewhere else. They’re not just making trade-offs – they’re making calculations. Essentials stay, extras go, and even mid-tier items are under scrutiny if there’s a cheaper equivalent close by.

Then there’s price perception. It’s not what something costs – it’s what it feels like it should cost. That’s why a 10% rise might barely dent volume in one category but trigger a collapse in another. It’s not rational, but it’s real – and it’s guiding what goes in the basket.

For retailers and brands, this moment demands more than sharper pricing. It requires fluency in how shoppers frame value. That might mean pricing just below emotional thresholds or structuring offers that signal stability – even when costs are climbing. In this climate, perception can be as powerful as reality.

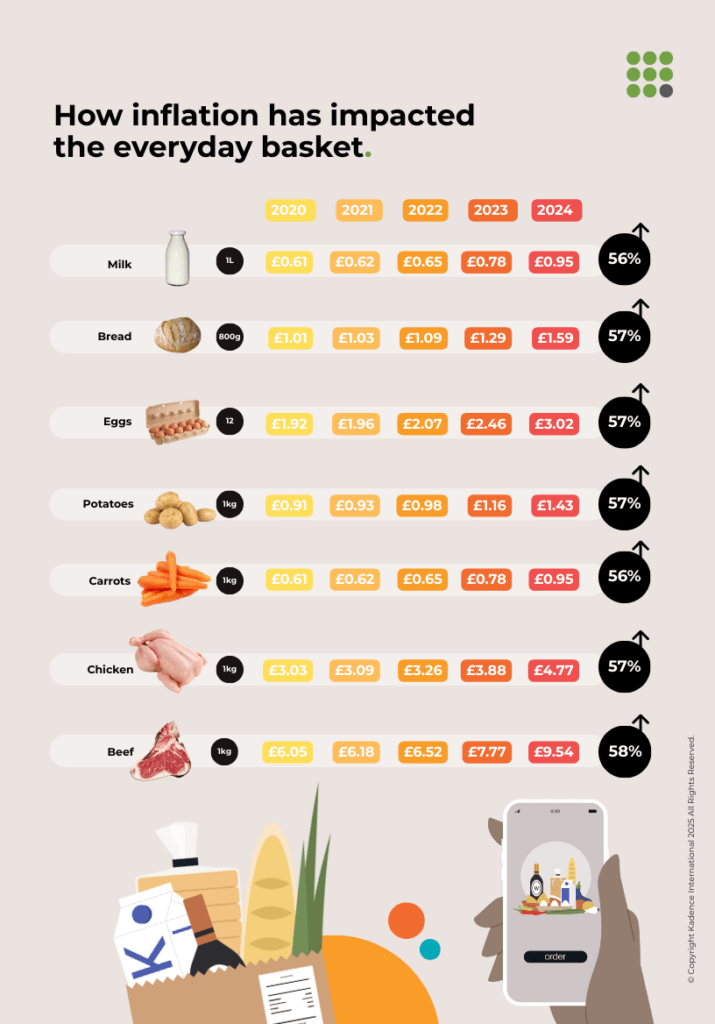

What does inflation feel like in real terms? The chart below shows just how much everyday items have risen since 2020.

Brand Erosion in the Era of the Basket Reboot

Brand loyalty isn’t dead – but it’s under review. Across the UK, what once felt automatic is now under scrutiny. Shoppers are looking at familiar labels, hesitating, and reaching for something cheaper – often store-brand, often good enough.

It’s not just trading down. It’s trading out. The basket reset happening now is exposing which brands still hold meaning and which were riding on habit. In categories like cereal, canned goods, and pasta sauces, private label has moved from backup plan to first choice. When shoppers feel squeezed, brand preference isn’t about awareness – it’s about justification.

The most vulnerable brands are the ones that rely on shelf presence and recognition without clearly articulating why they cost more. A fancy label or nostalgic logo doesn’t hold up when the price delta is visible, and the value isn’t. Own-label is no longer the compromise – it’s the baseline.

Supermarkets know this. That’s why they’ve built out three-tiered private label strategies: essential ranges for price-sensitive shoppers, core lines that match national brands on quality, and premium sub-brands designed to compete with legacy products on both taste and packaging. In many cases, they’re winning on all three fronts.

Branded suppliers are feeling the squeeze. Promotions are being pulled. Negotiations are tighter. Some products are being delisted entirely as retailers prioritise margin and private-label growth. Even in higher-margin categories like snacks and beverages, shoppers are experimenting more – and defaulting less.

This moment demands more than marketing. It demands a proposition that holds up under pressure. Brands that offer clear functional benefits – whether that’s health, sustainability, or convenience – still earn a place. But those that relied on emotional inertia are being quietly swapped out, one basket at a time.

The question for consumer goods companies isn’t just how to defend share. It’s how to rebuild relevance. Because if shoppers are open to changing their habits, they’re also open to forgetting the brands that no longer reflect how they want to spend.

Also, read our study on the UK’s Cost of Living Crisis here.

The New Class of Smart Shoppers

Frugality has rebranded itself – and fast. What used to be framed as a necessity or even a source of quiet shame has become a signal of control, intention, and in many cases, pride. The UK’s cost-of-living pressures have given rise to a new kind of grocery shopper: not just cost-conscious, but value-literate.

This isn’t driven solely by economics. It’s cultural. Discount shopping has moved out of the shadows and into the spotlight. TikTok is full of haul videos not from high-end retailers, but from Aldi and Lidl – highlighting bulk buys, dupes, and smart swaps. The tone isn’t apologetic. It’s instructional. Look what I saved. Look how much farther I stretched my budget. There’s a certain confidence in the captions: “You’d be mad to pay more.”

Digital tools have amplified the shift. Couponing, once a paper-based pursuit of extreme savers, has gone mobile and mainstream. Apps like Too Good To Go and supermarket loyalty platforms now offer real-time deals that reward flexibility, not just spending. Younger shoppers – especially millennials with families and Gen Z renters – are building grocery strategies around digital offers and flash pricing. Price matching isn’t a race to the bottom; it’s a form of skill.

What’s changed is the identity that surrounds all this. Saving money used to imply you didn’t have it. Now, it implies you’re informed. Especially among middle-income shoppers, there’s been a quiet erosion of stigma. Being a “deal hunter” no longer contradicts being design-conscious or health-focused. You can buy the store-brand canned tomatoes and still splurge on artisanal olive oil. You can track every penny and still care about the story behind your coffee.

This hybrid mindset – blending thrift and selectivity – is what many legacy brands are still struggling to read. Their customers didn’t disappear. They just rewrote the rules of what makes a product worth paying for.

It’s no longer enough to assume aspiration equals premium. In this landscape, brands have to justify every line of the receipt. They need to speak the language of value – but not just through lower prices. It’s about usefulness, quality, longevity, and emotional return on spend.

Smart shoppers aren’t waiting for brands to get it. They’re building baskets that reflect who they are now – pragmatic, digitally fluent, and empowered by information, not overwhelmed by it. The question isn’t whether this shift will last. It’s whether brands can keep up with customers who’ve stopped equating value with volume – and started defining it for themselves.

Retailers Rewrite the Rules

Retailers have stopped waiting for shoppers to come back to old habits. Instead, they’re adapting to new ones – fast. The traditional promotional cycle, once built around limited-time offers and seasonal spikes, has been replaced by something more fundamental: proving long-term value in real-time.

That shift is showing up everywhere. Tesco’s Clubcard Prices and Sainsbury’s Nectar Prices have moved from reward mechanics to central pricing strategies. What began as a loyalty tactic is now a core part of how these retailers compete with discounters. And it’s not just about price. It’s about visibility. Price tags on shelves now tell a story of what the customer is saving, not just spending.

Even premium grocers are adjusting. Waitrose, long associated with quality-first positioning, has expanded its Essentials range and emphasised value messaging in advertising. Its recent campaigns have spotlighted affordability without abandoning tone, suggesting that smart shopping doesn’t have to mean compromise.

But nowhere is the shift more aggressive than in private label. Across the sector, own-brand lines have become the innovation lab. Aldi and Lidl continue to lead, not just with price, but with product development that mirrors – and sometimes beats – national brands. The battleground isn’t just about matching flavor or format anymore. It’s about convenience, sustainability, and shopper emotion. A well-packaged ready meal that costs less and feels like a small win at the end of a long day? That’s more powerful than a deep discount.

Retailers are also experimenting with format. Smaller footprint stores are popping up in urban areas, designed around the grab-and-go shopper who wants efficiency, not abundance. Meal deals, shoppable recipes, “value hacks” – all of it engineered to speak the new shopper’s language: stretch, save, simplify.

Marketing has evolved in step. Circulars and point-of-sale have been replaced by in-app push notifications, hyper-local personalisation, and digital shelves that highlight time-sensitive offers. Messaging is less about indulgence and more about empowerment. You’re not just saving money; you’re being smart. You’re beating the system.

The result is a retail environment where success no longer comes from a breadth of range or deepest pockets. It comes from relevance – knowing who your customer is today, what trade-offs they’re willing to make, and how to meet them with the right balance of function, emotion, and frictionless value.

Case Study: How Aldi Became the Benchmark for Value With Purpose

Aldi’s rise in the UK has long been tied to price, but its current momentum speaks to something deeper: cultural relevance. While many retailers are reacting to consumer caution, Aldi has anticipated it – shaping not just how people shop but also how they think about spending.

Its private label dominance is no longer just about cost-cutting. Aldi has invested heavily in product development and packaging design that challenges branded equivalents, often earning accolades in blind taste tests. Shoppers aren’t settling – they’re discovering. Categories like wine, ready meals, and snacks now generate loyalty not as substitutes, but as preferred choices.

Where Aldi’s strategy truly stands out is in how it aligns with emerging shopper identity. The brand doesn’t apologise for low prices. It builds pride around them. Recent campaigns have leaned into humor and confidence, casting Aldi customers as smart, in-the-know shoppers rather than bargain hunters. The brand’s “Like Brands. Only Cheaper.” messaging isn’t defensive – it’s disruptive.

In-store, Aldi’s stripped-back format reinforces that every inch of shelf space must earn its keep. The tight range, fast checkout model, and curated promotions reflect a retailer that understands time, budget, and simplicity as core values – not just marketing points.

Aldi isn’t winning by chasing premium. It’s winning by reshaping what premium means in the mind of today’s value-driven consumer.

What Comes Next for Grocery, Brand Building, and British Retail

This isn’t just a cycle – it’s a structural shift. The current realignment in UK grocery is forcing a deeper redefinition of how brands are built, how value is communicated, and what kind of loyalty can actually be sustained in a low-growth, high-scrutiny environment.

The old model – premium equals quality, discount equals compromise – has fractured. What’s rising in its place is a hybrid mindset: shoppers who blend store brands and branded goods, who track savings as a personal KPI, and who want clarity in place of clutter. For brands and retailers, the challenge is no longer just about margin. It’s about meaning.

Products will still matter – but the story around them matters more. Why this? Why now? Why at this price? The brands that survive won’t just be better stocked or better known – they’ll be better understood. That means strategy rooted in real consumer behaviour, not assumptions. It means investing in insight before investing in shelf space.

We’ve entered an era where margins are thinner, decisions faster, and the consumer’s tolerance for noise almost nonexistent. The winners will be those who can decode the mindset behind the spend – what drives trust, what cues value, what kills interest – and adapt before the data shows up in declining sales.

For British retail, this could be a renaissance moment. But it will favor the precise, not the broad. Those who treat their audience as a living, evolving signal – not a static segment – those who invest in listening as much as launching.

Because the real growth ahead won’t come from pushing more into baskets. It will come from knowing what truly earns a place there.

A Market Redefined by Value Will Reshape the Industry

What’s happening in UK grocery right now isn’t a blip. It’s a reset. A recalibration of trust, relevance, and what constitutes a purchase worth making.

For brands, the margin for error has collapsed. Shoppers are not just selective – they’re strategic. They aren’t waiting to be impressed. They’re asking harder questions: Is this worth it? Is this credible? Does it deliver more than just a label?

Retailers that respond with nuance – not just price cuts – are the ones shaping the future. The discounter isn’t the disruptor anymore; it’s the new center of gravity. Traditional grocers that once competed on scale or loyalty must now compete on understanding. That means fewer assumptions, more clarity, and a sharper grasp on how value is perceived – not just priced.

Consumer behaviour isn’t snapping back. Once a shopper has built a new mental model of spending – one grounded in empowerment, not deprivation – it tends to stick. The post-abundance era doesn’t signal a withdrawal from consumption. It signals a new consciousness around it.

Over the next five years, British retail will be defined not by who shouts the loudest but by who listens best. That requires precision, pattern recognition, and real, ongoing intelligence on the evolving expectations of the people pushing the trolleys.

Smart brands won’t just ride this out. They’ll use it to rebuild better – on foundations that reflect today’s shopper, not yesterday’s playbook.

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Senior Marketing Executive

Senior Marketing Executive Sales & Marketing

Sales & Marketing General Manager PR -Internal Communications & Government Affairs

General Manager PR -Internal Communications & Government Affairs