Emerging economies now drive 59% of global GDP growth, with markets like India, Indonesia, and Nigeria reshaping the global economic order. But these opportunities come with a complexity that global brands often underestimate. Success depends on navigating fragmented data systems, informal economies, and fast-changing consumer behavior.

Digital adoption is one of the most transformative forces in these regions. Sub-Saharan Africa’s internet penetration, for instance, is growing at 23% annually—outpacing many developed markets, according to the World Bank. This growth opens vast new consumer bases but also demands a deeper understanding of local dynamics, where cultural and economic factors vary even within individual countries.

Traditional market analysis falls short in these settings. Established methods often miss the realities of unstructured data and regulatory shifts. In these unpredictable ecosystems, innovation is not just an advantage—it’s a necessity for brands that want to thrive.

The Landscape of Emerging Economies

Emerging economies, often defined by their rapid industrialization and growing middle classes, are increasingly driving global economic activity. According to the United Nations Conference on Trade and Development (UNCTAD), these markets accounted for 54% of global foreign direct investment inflows, underscoring their attractiveness to international investors.

What sets these economies apart is their high growth potential, fueled by urbanization, expanding labor forces, and technological adoption. India is on track to surpass Germany as the world’s fourth-largest economy by 2027, powered by a digital revolution that has brought over 700 million people online. Brazil remains a linchpin in global agriculture, supplying essential commodities like soybeans and coffee to sustain global supply chains.

Yet, growth in these economies comes with hurdles. Regulatory environments often shift rapidly to keep pace with economic changes. In Nigeria, efforts to diversify beyond oil have fostered a thriving fintech sector, now attracting nearly a quarter of Africa’s venture capital funding. Indonesia, Southeast Asia’s largest economy, has capitalized on its demographic advantage—65% of its population is of working age—to expand its manufacturing and services industries.

Consumer diversity adds another layer of complexity. By 2030, McKinsey estimates that 1.4 billion people in emerging markets will join the middle class, transforming consumption patterns. However, these consumers vary widely in preferences, shaped by cultural traditions, income disparities, and unequal access to technology.

The interplay of rapid growth, evolving regulations, and consumer diversity makes emerging markets both an opportunity and a challenge. Navigating these landscapes requires businesses to adapt their strategies with precision and agility.

Challenges in Conducting Market Analysis

Data Accessibility and Quality

In many emerging economies, reliable data remains elusive. Only 15% of countries in sub-Saharan Africa conduct regular household surveys, leaving brands to navigate blind spots in understanding consumer behavior and economic trends. To bridge these gaps, companies are turning to alternative methods like satellite imagery to estimate agricultural yields and AI-driven tools to analyze social media sentiment.

These technologies offer promising solutions but come with limitations. Satellite data can provide high-level insights but lacks the granularity needed for local market decisions. Similarly, AI tools often rely on digital footprints, which may underrepresent rural or offline populations, creating an incomplete picture. Bridging these gaps requires not only technological innovation but also localized research to ground findings in reality.

Local Nuances and Cultural Complexity

Cultural, linguistic, and regional differences across emerging economies pose significant challenges. Markets like India, for instance, are not monolithic; purchasing behaviors in urban Delhi differ drastically from those in rural Maharashtra. Failure to recognize such nuances can lead to costly missteps.

Consider the case of a global fast-food chain attempting to enter the Indian market. Its initial menu offerings largely ignored vegetarian preferences and regional tastes, leading to underwhelming sales. Only after revamping its menu to include paneer-based items and more vegetarian options did it see success.

Local partnerships can play a crucial role here. Partnering with local firms or cultural experts grounds strategies in local realities, minimizing cultural missteps.

Rapidly Evolving Consumer Behavior

The pace of change in emerging markets is unparalleled. Urbanization and digital adoption are driving rapid shifts in how consumers engage with brands. For example, Indonesia has seen a 32% increase in e-commerce sales year-over-year, driven by a growing middle class and smartphone penetration.

These shifts, while promising, complicate long-term predictions. Trends can emerge and fade faster than companies can adapt. A product that thrives in one year might lose relevance the next as consumer preferences evolve. To mitigate this, companies are leveraging predictive analytics and real-time monitoring to stay ahead of emerging trends.

Regulatory and Economic Instability

The regulatory landscape in emerging economies is often in flux. Tariffs, trade policies, and tax structures can change overnight, leaving businesses scrambling to adjust. In 2021, Nigeria’s sudden ban on Twitter disrupted digital marketing plans for numerous brands, illustrating the risks of relying on volatile platforms or policies.

Economic instability, including currency fluctuations, adds another layer of unpredictability. Argentina’s inflation rate, for instance, exceeded 100% in 2023, making it difficult for companies to maintain consistent pricing strategies.

To manage these challenges, brands are incorporating contingency planning into their market analysis. Diversifying supply chains, hedging against currency risks, and building agile operations are becoming standard practices for those operating in these unpredictable environments.

Coca-Cola’s investment in sub-Saharan Africa during the 1990s highlights the rewards of entering emerging markets early. By building local bottling plants and distribution networks, the company secured its dominance, leaving late-arriving competitors struggling to catch up.

Identifying similar opportunities today requires advanced tools like predictive analytics to track demographic shifts, urbanization, and emerging consumer trends. Data from international organizations such as the IMF and localized surveys provide the insights necessary for decisive action.

Harnessing Local Partnerships

Collaborating with local businesses is another key to success. Unilever’s expansion in India illustrates this approach. By working with regional distributors and offering sachet-sized product packaging tailored to price-sensitive consumers, Unilever extended its reach into rural areas where global brands often faltered.

Procter & Gamble’s success in Vietnam offers another example. By tailoring its supply chain to the country’s fragmented retail sector, P&G ensured its products were widely available, reinforcing brand loyalty among consumers.

Tech-Driven Insights

In regions where traditional data collection methods fall short, technology is filling the gap. AI and machine learning are helping brands analyze massive datasets, uncover patterns, and make real-time decisions. For example, mobile data in Africa has become a critical resource for understanding consumer behavior, with telecom companies providing anonymized insights to brands.

E-commerce platforms are also reshaping how brands gather intelligence. In Indonesia, where 68% of the population is active on social media, companies monitor conversations to refine products and marketing strategies. Platforms like India’s Flipkart and Southeast Asia’s Shopee reveal regional purchasing trends, helping brands identify emerging opportunities with precision.

Advanced Techniques for Effective Market Analysis

Granular Segmentation and Personalization

In emerging markets, broad demographic categories often fail to capture the intricacies of consumer behavior. Effective market analysis requires breaking down populations into more actionable segments, considering factors such as income brackets, urban versus rural distinctions, and cultural influences. For instance, in India, the rural affluent consumer—a group often overlooked in global strategies—represents a significant portion of the purchasing power outside metropolitan areas.

Creating accurate consumer personas tailored to these nuanced segments involves leveraging regional and behavioral data. Platforms like Tableau and Statista provide businesses with tools to analyze trends at a granular level, from age-specific purchasing patterns to localized preferences. For instance, a consumer persona for Brazil’s northeastern region may differ substantially from that of São Paulo due to disparities in income levels and product accessibility.

Personalization, driven by this segmentation, is key to gaining consumer trust. Brands like Spotify have succeeded in emerging markets by tailoring their offerings, such as creating locally relevant playlists and price tiers that cater to diverse income groups.

Predictive Analytics and Scenario Modeling

The dynamic nature of emerging economies makes it essential for businesses to anticipate trends and prepare for uncertainties. Predictive analytics uses machine learning and advanced statistical techniques to identify potential future scenarios, helping companies refine their strategies.

For example, platforms like SAS and IBM Watson enable businesses to model scenarios such as currency fluctuations, supply chain disruptions, or sudden policy changes. When Nigeria introduced a ban on certain imports in 2020, companies that had prepared alternative sourcing strategies using scenario modeling were able to adapt quickly, avoiding significant losses.

This proactive approach also allows businesses to stay ahead of emerging consumer trends. In Indonesia, predictive tools have been used to track the growth of the online grocery market, enabling companies to invest in logistics infrastructure ahead of competitors.

Incorporating Human-Centered Design

Emerging markets often include underserved segments whose needs are not met by mainstream products. Human-centered design (HCD) bridges this gap by placing consumers at the heart of product development. Ethnographic research—a key component of HCD—focuses on observing and understanding consumer behavior in real-life contexts, providing insights that quantitative data might miss.

For instance, Unilever’s development of low-cost, single-use shampoo sachets in India was inspired by observing how consumers in rural areas managed tight household budgets. Similarly, Procter & Gamble’s design of water purification packets addressed the lack of clean drinking water in underserved African communities, creating a product that was both impactful and profitable.

By focusing on practical, locally relevant solutions, human-centered design not only improves product adoption but also fosters a deeper connection between brands and consumers.

Case Studies: Success and Lessons Learned

Success Story: Xiaomi’s Rise in India

Xiaomi’s entry into India showcases the power of understanding local markets. By tailoring its smartphones to balance affordability with premium features, Xiaomi tapped into the price-sensitive demands of Indian consumers. Partnering with e-commerce platforms like Flipkart, it leveraged flash sales to create buzz and drive demand. Today, Xiaomi dominates India’s mid-range smartphone market, outperforming established competitors such as Samsung.

Success Story: Grab’s Southeast Asia Expansion

Grab’s success across Southeast Asia highlights the value of adapting to regional realities. Recognizing the prevalence of motorcycles over cars, Grab prioritized motorbike ride-hailing in countries like Vietnam and Indonesia. It also integrated cash payments to accommodate regions with low credit card penetration. By combining local partnerships with agile strategies, Grab became a dominant player in the region’s ride-hailing and food delivery markets.

Lesson Learned: Walmart’s Struggles in South Korea

Walmart’s failure in South Korea underscores the risks of applying global strategies without considering local consumer behavior. By focusing on bulk purchases and low prices, Walmart overlooked cultural preferences for smaller, frequent shopping trips and premium local products. Competing against entrenched local retailers like E-Mart, Walmart exited the market in 2006, having failed to adapt its approach to meet South Korean expectations.

Takeaway

These examples reveal a common thread: success in emerging markets hinges on deep local insight and adaptability. Whether through tailored product offerings, strategic partnerships, or cultural sensitivity, companies that invest in understanding regional realities gain a decisive edge. Conversely, missteps like Walmart’s serve as a cautionary tale of the pitfalls of imposing one-size-fits-all strategies on diverse markets.

Practical Framework: Building a Market Analysis Toolkit

1. Grounded Local Insights

Effective market analysis begins with deep local insights. In countries like Indonesia, where consumer preferences vary sharply between urban and rural areas, on-the-ground research is non-negotiable. Partnering with local market research agencies can transform broad observations into actionable strategies, helping brands tailor products and campaigns to specific demographics. For instance, understanding that rural consumers prioritize affordability while urban buyers value convenience can shape product pricing and distribution strategies.

2. Hybrid Methodologies for a Complete Picture

A blend of quantitative and qualitative research provides a clearer view of emerging markets. Large-scale surveys and sales data reveal trends, but qualitative methods like focus groups and ethnographic studies add context to the numbers. For example, in Vietnam’s e-commerce sector, surveys may highlight the growth in online shopping, but interviews can reveal trust issues with digital payment platforms—critical insights for building effective strategies. Collaborating with agencies that specialize in these hybrid approaches ensures a balanced and comprehensive analysis.

3. Adapting Global Strategies to Local Realities

Global strategies rarely succeed without local adaptation. Products designed for Western markets often fail in regions where cultural expectations and economic realities differ. In Southeast Asia, for instance, durable, affordable goods resonate more than premium branding. Partnering with local distributors or cultural experts ensures that global visions align with regional needs, whether through modified packaging, pricing adjustments, or localized marketing campaigns.

4. Continuous Monitoring and Agile Adjustments

Emerging markets evolve rapidly, making real-time monitoring essential. Trends like the rise of digital wallets in India or live-stream shopping in China require businesses to adapt quickly or risk irrelevance. Regular data collection, combined with ongoing analysis, allows brands to refine strategies as conditions change. Partnering with agencies for market monitoring services can help brands stay ahead of these shifts and capitalize on new opportunities as they arise.

Bottom Line

In emerging markets, the key to success lies in preparation and adaptability. Companies that invest in granular research, hybrid methodologies, and real-time strategy adjustments position themselves to navigate complexity and drive growth. Without these tools, businesses risk being outpaced by competitors who better understand the local landscape.

The Future of Market Analysis in Emerging Economies

As digital infrastructure connects billions of people in emerging markets, these regions are poised to reshape global business. Expanded mobile and internet access is unlocking new consumer bases and accelerating innovation. For instance, the GSMA predicts that by 2025, more than 60% of sub-Saharan Africa will have mobile internet access, driving demand for digital services and e-commerce.

However, the rapid pace of change means businesses face a critical choice: adapt or risk irrelevance. Success in these markets will depend on striking the right balance—leveraging global expertise while remaining deeply attuned to local realities. Agility, investment in data-driven tools, and partnerships with regional experts will be essential.

The next decade will belong to companies that can seamlessly integrate global strategies with localized execution. Emerging economies are more than growth opportunities; they are the proving grounds for businesses to test innovation, refine strategies, and lead in an interconnected world.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Establishing a global brand is complex. Companies looking to expand internationally must contend with significant challenges, including varying consumer behaviors, cultural differences, and economic disparities. These factors make maintaining a consistent brand identity complicated while adapting to local demands. However, the rewards for getting it right are substantial. Brands that successfully navigate these complexities can tap into new markets, increase their global presence, and achieve sustained growth.

Understanding Local Market Dynamics

Successfully expanding into a new market requires more than just introducing an existing product or service to a different audience. This requires a deep understanding of the local environment, where cultural nuances, consumer behavior, and economic factors are crucial for a brand’s success. Brands that fail to consider these elements often struggle to gain traction because what works in one region may not translate effectively to another.

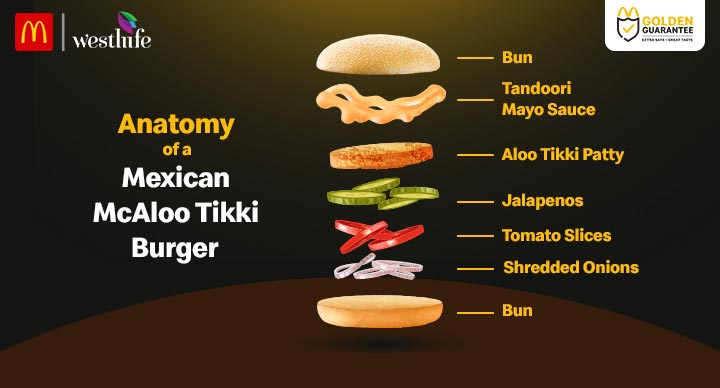

Take McDonald’s as an example. The fast-food giant’s success in markets like India highlights the importance of adapting to local tastes and preferences. Recognizing that much of the population avoids beef, McDonald’s reimagined its menu, introducing vegetarian options like the McAloo Tikki, a potato-based burger that quickly became a local favorite. This adaptation wasn’t a simple change; it resulted from extensive market research that provided insights into local dietary habits, preferences, and cultural sensitivities. By leveraging this in-depth understanding of the Indian market, McDonald’s maintained its brand identity while catering to local tastes, leading to its widespread acceptance and success in the region.

Image credit: McDonald’s blog

Adapting Global Strategy to Regional Needs

Maintaining a global identity while adapting to regional markets is a delicate balancing act. Brands must ensure their core values and messaging remain consistent across all markets. Yet, they must also be flexible enough to meet the specific needs and preferences of local consumers. This balance is crucial for sustaining a coherent brand image while being relevant in diverse regions.

Coca-Cola exemplifies how a global brand can achieve this balance. The company has consistently maintained its brand identity through its iconic logo, packaging, and overarching messaging centered around happiness and togetherness.

However, Coca-Cola also customizes its marketing strategies to resonate with local audiences. In Japan, for instance, Coca-Cola introduced a range of products that cater specifically to Japanese tastes, such as green tea-flavored beverages and smaller, more convenient packaging sizes. The brand also tailored its advertising campaigns to align with local cultural values and traditions, reinforcing its relevance.

This approach allows Coca-Cola to retain its global identity while remaining adaptable to regional preferences. The result is a brand that feels familiar and relevant to consumers worldwide, demonstrating the effectiveness of a flexible global strategy that accommodates local needs.

Image credit: Coca-Cola Japan

Leveraging Technology for Global Reach

Technology is a critical asset for brands aiming to expand their presence globally. Digital platforms, data analytics, and artificial intelligence (AI) offer the tools necessary to understand and engage with consumers across different regions. These technologies allow brands to collect real-time insights, personalize their offerings, and deploy targeted marketing strategies that resonate with diverse audiences.

Netflix exemplifies how technology can drive global success. The streaming service uses data analytics and AI to deeply understand viewer preferences in various markets. By analyzing viewing patterns, Netflix can tailor content recommendations to individual users, making the experience more relevant and engaging for audiences around the world.

Additionally, Netflix’s investment in local content further enhances its appeal in specific regions, demonstrating how technology can be leveraged to achieve global reach and local relevance.

Image Credit: Netflix

Building Brand Trust Across Borders

Building trust is fundamental to a brand’s success, particularly when expanding into new markets. Trust is not just about delivering a quality product; it’s about transparency, adhering to ethical practices, and forging strong local partnerships. Consumers across the globe are increasingly discerning, and they expect brands to act responsibly and authentically, especially when they enter their local markets.

Unilever is a strong example of a brand that has effectively built trust across borders. The company’s commitment to ethical practices and corporate responsibility is evident in its Sustainable Living Plan, which aims to improve health and well-being, reduce environmental impact, and enhance livelihoods worldwide. Unilever has successfully integrated these principles into its operations across different regions, tailoring its initiatives to address local challenges.

For instance, in India, Unilever has partnered with local organizations to promote hygiene and sanitation through its Lifebuoy soap brand. By educating communities about the importance of handwashing, the company not only enhances public health but also strengthens its reputation as a responsible and caring brand. This approach has earned Unilever significant trust and loyalty from consumers in diverse markets, proving that ethical branding and corporate responsibility are crucial to establishing long-term relationships with global audiences.

Image credit: Unilever

Navigating Regulatory and Competitive Landscapes

Expanding into new markets often means navigating a complex web of regulations and facing stiff competition from established local players. Regulatory requirements can vary significantly from one country to another, covering areas such as product standards, advertising restrictions, and data privacy laws. For global brands, the ability to adapt to these regulations while maintaining a competitive edge is crucial for success.

Apple’s entry into the Chinese market illustrates how a brand can overcome regulatory challenges to establish a strong presence in a highly competitive environment. China’s strict regulations on data storage, internet censorship, and local partnerships posed significant hurdles for Apple. To comply with Chinese laws, Apple made strategic decisions, such as partnering with local companies like China Mobile and setting up a data center in China to store user data locally. These moves ensured that Apple met regulatory requirements without compromising its product offerings.

Moreover, Apple’s approach to navigating the competitive landscape in China involved understanding and responding to local consumer preferences. Apple differentiated itself from local competitors by offering localized content and services and developing features tailored to Chinese users. Despite the challenges, Apple’s ability to adapt to the regulatory environment and stay attuned to local market dynamics has allowed it to maintain a strong foothold in one of the world’s most challenging markets.

Image credit: Apple Store China

Common Pitfalls and How to Avoid Them

Expanding into international markets presents numerous opportunities but comes with its share of risks. Many brands make critical mistakes that can hinder their success or even derail their expansion strategy. Understanding these pitfalls and how to avoid them is essential for any brand looking to establish a global presence. Below is a list of common mistakes brands often make during worldwide expansion and practical solutions to navigate these challenges effectively.

Underestimating Cultural Differences

Conduct thorough cultural research to understand local customs, values, and consumer behaviors.

Tailor your product offerings, marketing messages, and customer interactions to align with these cultural nuances.

Ignoring Local Competition

Analyze and understand the competitive landscape in each market.

Identify major local competitors and their strengths and weaknesses, and adjust your strategy to offer something unique that resonates with local consumers.

Failing to Comply with Local Regulations

Engage local legal experts to ensure full compliance with local regulations, including product standards, advertising restrictions, and data protection laws.

Review regulatory changes regularly and adapt quickly to stay compliant.

Inconsistent Brand Messaging

Develop a flexible yet consistent global strategy that maintains your brand’s core identity while allowing for regional adaptations.

Ensure all marketing materials and communications align with global standards and local expectations.

Overlooking Supply Chain Challenges

Plan for logistical challenges specific to each region, including shipping, distribution, and inventory management.

Establish reliable local partnerships and consider setting up regional hubs to streamline operations.

Inadequate Customer Support

Provide customer support tailored to the local market, including language preferences and cultural expectations.

Invest in training local customer service teams to ensure they can address issues effectively and empathetically.

Underestimating the Importance of Local Partnerships

Cultivate strong relationships with local businesses, distributors, and influencers who can help you navigate the market and build credibility.

Local partnerships can provide valuable insights and resources that enhance your brand’s market entry and growth.

Rushing the Market Entry

Take the time to conduct thorough market research and develop a solid entry strategy.

Avoid rushing into a market without fully understanding the local dynamics, leading to costly mistakes and setbacks.

Neglecting Long-Term Strategy

Don’t focus solely on short-term gains. Develop a long-term strategy that includes continuous market research, adaptation to evolving consumer needs, and investment in local relationships.

Regularly revisit and refine your strategy to ensure sustained success.

Case Study Deep Dive: Tesla’s Global Expansion Success Story

Image credit: Tesla

Tesla, Inc. is a prime example of a brand that has successfully navigated the complex landscape of global expansion. From its early days as a niche electric vehicle (EV) manufacturer in the United States to becoming a dominant global force in the automotive industry, Tesla’s journey offers valuable insights into the strategic decisions, challenges, and results that have shaped its international success.

Initial Strategy: Establishing a Strong Foundation

Tesla’s entry into the global market was built on a foundation of innovation and strategic foresight. The company’s initial focus on producing high-performance electric sports cars, such as the Tesla Roadster, helped establish its reputation as a pioneer in EV technology. This positioning attracted early adopters and generated significant media attention, laying the groundwork for Tesla’s future growth.

One of Tesla’s earliest and most critical decisions was its Initial Public Offering (IPO) in 2010. The capital raised through the IPO provided the financial resources necessary to fund the development of additional vehicle models, expand manufacturing capabilities, and begin entering international markets. This move was instrumental in positioning Tesla for global expansion.

Market Entry: Targeting Europe and China

Tesla’s first significant international push came in 2013 with its entry into the European market. The company began selling the Model S in Europe, strategically opening service centers and stores in key cities across the continent. Europe’s strong interest in sustainability and green technology provided a receptive market for Tesla’s vehicles. Tesla invested heavily in building its Supercharger network to further support its European customers, ensuring EV owners had access to reliable charging infrastructure across the region.

China represented another significant milestone in Tesla’s global expansion. Recognizing the growing demand for electric vehicles in China, Tesla entered the market in 2015 with the Model S. China’s strict regulations on foreign ownership and data storage posed challenges. However, Tesla navigated these hurdles by forming partnerships with local companies and committing to building a Gigafactory in Shanghai. This strategic move allowed Tesla to localize production, reduce costs, and better serve the Chinese market, quickly becoming one of Tesla’s largest sources of revenue.

Tesla’s global expansion has not been without its challenges. The company has had to navigate various regulatory environments, each with its own set of rules and requirements.

In China, Tesla faced significant hurdles in data localization and foreign ownership. To comply with local laws, Tesla established a data center in China and became the first foreign automaker to wholly own its factory, thanks to changes in Chinese regulations.

In Europe, Tesla encountered challenges related to manufacturing and logistics. The decision to build Gigafactory Berlin was a direct response to these challenges. By establishing a manufacturing presence in Europe, Tesla could reduce production bottlenecks and streamline the delivery of vehicles to European customers, thereby enhancing its competitiveness in the region.

Results: A Global Automotive Leader

Today, Tesla is a global leader in the automotive industry, with a presence in major markets across North America, Europe, and Asia. The company’s commitment to innovation, sustainability, and strategic market entry has paid off, with Tesla consistently ranking as one of the world’s most valuable automakers.

Tesla’s success in international markets is evident in its sales figures and market share. The company’s ability to localize production through Gigafactories in China and Europe has significantly increased its manufacturing capacity and reduced costs, making its vehicles more accessible to a global audience. Additionally,

Tesla’s continued investment in its Supercharger network and local partnerships has strengthened its brand’s reputation for reliability and customer satisfaction.

Key Takeaways from Tesla’s Global Expansion:

Strategic Market Entry: Tesla’s careful selection of markets and timing of entry were crucial to its success. The company prioritized regions with strong demand for EVs and supportive regulatory environments.

Localization of Production: Tesla could localize production, reduce costs, and meet the specific needs of local markets by building gigafactories in China and Europe.

Regulatory Compliance: Tesla’s proactive approach to navigating regulatory challenges, such as data localization in China, ensured its continued growth and success in key markets.

Innovation and Adaptation: Tesla’s commitment to innovation, from its vehicle technology to its charging infrastructure, has allowed it to stay ahead of competitors and continuously adapt to changing market conditions.

Checklist for International Expansion

Expanding into global markets requires careful planning and execution. Below is a practical checklist to guide brands through the complexities of international expansion:

Conduct Comprehensive Market Research:

Analyze local consumer behaviors, cultural nuances, and economic conditions.

Identify the demand for your product or service and understand the competitive landscape.

Determine the local market’s potential for growth and profitability.

Assess and Adapt to Regulatory Environments:

Understand and comply with local regulations, including product standards, advertising laws, and data protection policies.

Engage with local legal and regulatory experts to ensure compliance and mitigate risks.

Develop a Flexible Global Strategy:

Create a strategy that maintains global brand consistency while allowing for regional adaptations.

Tailor marketing campaigns, product offerings, and messaging to resonate with local audiences.

Leverage Technology for Localization:

Utilize data analytics and AI to gather real-time insights on local consumer preferences.

Implement digital tools to personalize the customer experience in different markets.

Ensure your digital platforms are optimized for local languages and cultural contexts.

Build Strong Local Partnerships:

Collaborate with local businesses, distributors, and influencers to enhance market entry and brand credibility.

Consider joint ventures or partnerships to navigate local markets more effectively.

Prioritize Ethical Practices and Corporate Responsibility:

Uphold transparency and ethical practices in all markets to build trust with consumers.

Engage in corporate social responsibility initiatives that resonate with local communities and reflect your brand values.

Prepare for Operational Challenges:

Plan for logistics, supply chain management, and distribution networks tailored to local market needs.

Ensure your customer service and support are equipped to handle regional languages and issues.

Continuously Monitor and Adapt:

Regularly assess your performance in each market and adjust strategies as needed.

Stay attuned to global market trends and local developments that may impact your business.

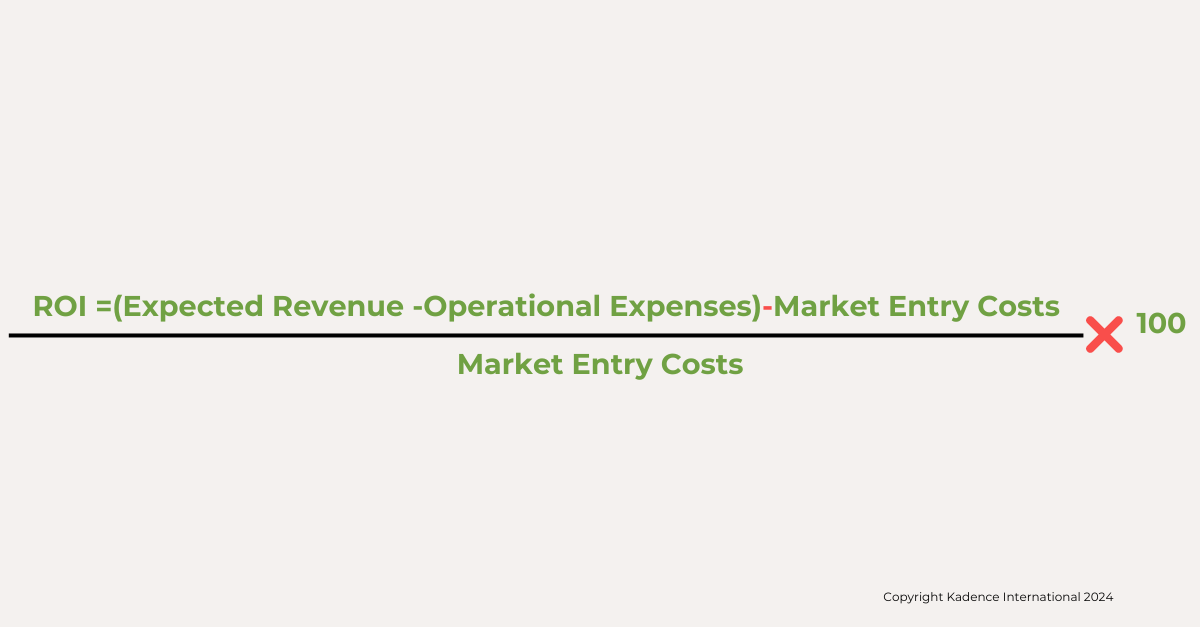

Global Expansion ROI Calculator

The Global Expansion ROI Calculator provides a framework for estimating the financial outcomes of entering new markets, allowing brands to assess the viability of their global strategies. This tool considers factors such as market entry costs, expected revenue, and operational expenses, offering a practical guide to evaluating the potential profitability of international expansion.

Key Components of the ROI Calculation:

Market Entry Costs:

Initial Investment: Include costs associated with market research, legal fees, and setting up operations (e.g., offices, supply chains).

Marketing and Localization: Factor in the cost of marketing campaigns, localization of products, and adaptation of branding to fit local tastes and regulations.

Expected Revenue:

Sales Projections: Estimate potential revenue based on market size, target audience, and expected market share.

Pricing Strategy: Consider how local economic conditions and consumer behavior influence pricing and sales volume.

Operational Expenses:

Ongoing Costs: Include expenses related to staffing, logistics, regulatory compliance, and customer service tailored to the local market.

Technology and Infrastructure: Account for investments in digital platforms, supply chain management, and local partnerships.

Simplified ROI Formula:

Expected Revenue: Projected income from sales in the new market.

Operational Expenses: Ongoing costs of running the business in the new market.

Market Entry Costs: Initial investment required to enter the market.

Conceptual Guide:

Conduct Thorough Market Research:

Understand the size of the market, customer demand, and competition.

Use data to project realistic sales figures and potential market share.

Estimate Costs Accurately:

Include all potential costs, both one-time and ongoing, in the calculation.

Consider possible variations in costs due to local economic conditions or regulatory changes.

Adjust for Local Variables:

Tailor your pricing strategy to local consumer expectations and purchasing power.

Anticipate fluctuations in revenue based on seasonality, economic trends, or political stability.

Calculate and Compare:

Use the ROI formula to estimate the potential return from each market.

Compare these estimates across regions to prioritize markets with the highest potential return.

Review and Reassess:

Regularly revisit your calculations as market conditions evolve.

Adjust strategies based on real-world performance and emerging opportunities or challenges.

Final Thoughts

Expanding internationally is not a one-size-fits-all endeavor; it requires a deep understanding of local markets, the flexibility to adapt strategies, and the strategic use of technology to connect with diverse audiences.

Brands that succeed on the international stage prioritize local insights, ensuring their offerings resonate with cultural nuances and consumer preferences. They balance global consistency with regional relevance, leveraging technology to gather real-time data and personalize their approach. Trust and reputation, built through transparency and ethical practices, are equally crucial as they foster long-lasting consumer relationships across borders.

The critical lesson for brands looking to expand globally is clear: adaptability is key. As markets continue to evolve, brands must remain agile, continuously refining their strategies to meet consumers’ shifting demands and expectations worldwide. Success in global markets isn’t just about entering new regions; it’s about sustaining that presence by staying attuned to each market’s unique challenges and opportunities. Those who can do so will thrive today and be well-positioned for long-term success in an increasingly interconnected world.

Have you ever wondered why obtaining a bank loan isn’t as easy as shopping online? Or why selecting a health insurance policy isn’t as quick as booking a hotel?

The modern consumer has higher expectations and is increasingly asking these questions. Brands that cater to these expectations stand to beat the competition and garner customer loyalty.

So, if you think you know your competition, think again.

A senior executive at IBM once captured the modern consumer’s needs: “The last best experience anyone has anywhere becomes the minimum expectation for the experience they want everywhere.”

This statement challenges most executives’ understanding of competition —that they’re limited to major players or emerging brands in their industry. However, what if the real competition extends beyond your industry? How do brands craft a winning strategy when they’re not just competing with industry peers but also with ever-evolving customer expectations shaped by their best experiences in other sectors?

In the past,, brands gauged their competition based on rivals within their industry. A car dealership compared itself to other car dealers, a bank to other banks. This approach, while logical, is increasingly becoming outdated. In a connected world where consumers can instantly compare services and products across sectors, their expectations are no longer siloed within industry lines.

A coffee shop isn’t just competing with the café next door but also with the fast, personalized service of tech firms or the immersive experience of a luxury retailer. This broader perspective on competition compels brands to innovate continually, not just in their product or service offerings but in customer experience, convenience, and reliability.

The story of Amazon epitomizes this change. Once an online bookstore, Amazon became a colossal e-commerce platform, challenging bookstores and retailers across countless sectors. Their competitive edge? Understanding and setting new benchmarks in customer expectations.

Most recently, Dubai International Airport set new benchmarks in its sector by introducing a new biometric system that allows travelers to Dubai to travel without a passport, which makes the experience more pleasant.

Rethinking competition means brands must now consider how they stack up against the best experience a customer has had anywhere, not just against their traditional industry competitors. It’s a move from industry-focused to customer-experience-focused competition, a transition that requires a deep understanding of customer expectations far beyond industry boundaries.

Role of Market Research in Revealing True Competitors

Market research is integral to identifying a brand’s opportunities. It helps companies understand who they compete against and their customers’ evolving expectations. For instance, a fast-food chain might find its real competition lies not only with other fast-food outlets but with the expected experience whenever or whatever they buy.

Chick-fil-A, a U.S. fast-food chain known for its chicken sandwiches, redefined its customer service by looking beyond its immediate competitors in the fast-food industry. This venture was initiated through a partnership with Horst Schulze, the COO of Ritz-Carlton at the time, as the hotel chain is synonymous with luxury and exceptional customer service.

The Challenge:

Chick-fil-A was already performing well against its direct fast-food competitors. However, Schulze’s assessment that they were the “best of a bad lot” challenged them to aim higher, to compete not just with other fast-food chains but also with sit-down and fine-dining restaurants known for their superior customer service.

Market Research and Strategy:

To bridge this gap, Chick-fil-A executives thoroughly analyzed these higher-end dining experiences. They conducted surveys and customer feedback sessions to understand the most valued service elements in these settings. The result was the creation of the “Core 4” principles of customer service, focusing on creating eye contact, sharing smiles, using an enthusiastic tone, and personalizing customer interactions.

Image Courtesy: Chick-fil-a

Further Consultation with Danny Meyer:

Chick-fil-A didn’t stop with the insights from Ritz-Carlton. They also consulted with Danny Meyer of Union Square Hospitality Group, who is renowned for his hospitality expertise. Meyer, who later founded the popular fast-casual chain Shake Shack, worked with Chick-fil-A to deepen their understanding of hospitality, emphasizing the importance of going the extra mile in service, a relatively uncommon fast food concept.

Impact and Results:

Implementing these strategies led to a significant transformation within Chick-fil-A’s service model. As a Chick-fil-A executive noted, the impact on sales, profits, and overall customer engagement was profound. The adoption of “second-mile service” became a hallmark of Chick-fil-A, noticeably differentiating them from their traditional fast-food competitors.

Competitive Analysis Across Industries

Conducting a competitive analysis beyond your immediate industry is crucial. This broader approach can uncover valuable insights and innovative practices from various sectors, offering a more comprehensive view of the competitive terrain.

How to Conduct a Cross-Industry Competitive Analysis

Identify Key Competitors in Other Industries: Identify companies in other sectors admired for customer service, innovation, or efficiency. These could be organizations your customers frequently compare you to, even if they are outside your direct line of business.

Gather Information: Utilize public resources like company websites, press releases, case studies, and industry reports to gather information about these competitors. Pay attention to their business models, customer engagement strategies, marketing approaches, and operational efficiencies.

Analyze Customer Reviews and Feedback: Look at customer reviews and feedback for these companies. Platforms like social media, online forums, and review sites can provide insights into what customers value in their experiences with these brands.

Study Their Service Delivery and Processes: Examine how these companies deliver their services or products. What makes their process stand out? How do they handle customer service, and what are their operational efficiencies?

Benchmark Against Best Practices: Compare these findings against your practices. This benchmarking should cover customer experience, service speed, technological adoption, and innovation.

SWOT Analysis: Conduct a SWOT (Strengths, Weaknesses, Opportunities, Threats) analysis for both your company and the companies in other industries. This comparison can highlight areas for improvement and potential opportunities for your brand.

Learning from Best Practices in Different Sectors:

Adopting Technological Innovations: Look at how tech companies use technology to enhance customer experience and consider how you could implement similar technologies in your sector.

Customer Service Excellence: Study the customer service strategies of companies known for outstanding customer care, like luxury hotels or high-end retailers, and integrate applicable elements into your customer service approach.

Efficiency Models: Analyze the operational efficiency of companies in industries like manufacturing or logistics. Their practices could offer insights into streamlining your processes.

Innovative Marketing Strategies: Observe companies’ marketing tactics in creative industries or those that have successfully tapped into new customer segments.

Sustainability Practices: Learn from companies leading in sustainability and environmental responsibility. For instance, even if you are a beverage brand, you can learn from Patagonia, a clothing brand that is leading in sustainability. This could improve your company’s environmental impact and enhance your brand image.

Using Market Research to Adapt to Market Conditions and Customer Expectations

Continuous Market Monitoring: Regularly monitor market trends and consumer behavior to stay ahead of changes and adapt strategies accordingly. Through constant market research and monitoring, Nike remains innovative with new product lines. In recent years, Nike introduced athleisure wear in response to the growing fitness and casual lifestyle blending trend.

Feedback Loops: Establish mechanisms for continuous customer feedback to gauge the effectiveness of the implemented strategies and make adjustments as needed. For example, Xiaomi, a Chinese consumer electronics brand, utilizes a unique business model that heavily relies on customer feedback. They regularly update their smartphones and other electronic products based on consumer suggestions gathered through online forums and social media, ensuring they stay closely aligned with user needs and preferences.

Agility in Strategy Execution: Be prepared to quickly alter or refine strategies in response to market feedback or shifts in the competitive landscape. Faced with unprecedented challenges in the restaurant industry due to lockdowns and restrictions during the pandemic, McDonald’s swiftly adapted its approach. They expanded contactless ordering and delivery options, simplified their menu to streamline operations, introduced promotions, implemented rigorous safety measures for employees and customers, and engaged in community support efforts. This rapid response allowed McDonald’s to maintain its customer base, ensure employee safety, and serve as a dependable source of affordable food during a crisis, showcasing its ability to pivot and succeed in a changing market landscape.

Incorporating Technology: Leverage technology to enhance customer engagement, streamline operations, and gather data for ongoing market analysis. For example, Amazon has continuously leveraged technology to improve customer engagement and streamline operations. From its recommendation algorithms to the use of AI and robotics in its warehouses, Amazon uses technology to improve efficiency and the customer experience.

Sustainability and Social Responsibility: Integrate sustainable practices and social responsibility into business strategies, aligning with the increasing consumer emphasis on ethical and environmental considerations. For instance, Toyota has long been a leader in sustainability, particularly with its development of hybrid and electric vehicles like the Prius. Their commitment to reducing environmental impact through sustainable practices is a core part of their business strategy, aligning with global concerns about climate change.

Final Thoughts —Use Customer Expectations as a Competitive Benchmark

Working with global brands across industries and geographies, we have uncovered a critical insight: many brands may not fully realize who their competitors are. As we’ve seen through various successful brand examples, your competitors may sometimes be different from the ones you’ve traditionally considered. Instead, they could be any brand or service that sets the expectations for your customers, often from entirely different industries.

Customers today are exposed to a wide range of services and products, from online retail giants to high-tech consumer electronics. The quality of service and efficiency they experience in one sector invariably shapes their expectations of others. This shift means a brand is no longer just competing within its industry but also against the best practices of sectors far removed from its own.

Market research emerges as a powerful tool in this scenario. It helps you understand what your customers expect based on industry standards and their best experiences in any sector. These expectations become your competitive benchmark. Whether it’s the seamless convenience of an app, the personalized service of a luxury hotel, or the efficiency of a tech giant, these are the standards against which your customers are measuring you.

Therefore, brands must engage in market research and competitive analysis continuously. This ongoing process will help you stay abreast of current market trends and customer expectations and allow you to anticipate future changes. Understanding and adapting to these evolving benchmarks allows your brand to remain competitive in a market reshaped by new players, technologies, and consumer behaviors.

Look beyond your industry, learn from the best in all sectors, and use these insights to refine and enhance your business strategies. This continuous market research and competitive analysis is essential for sustained success and growth in a rapidly changing market.

For more information on how to conduct a competitive analysis, contact us here.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Share

Sun Tzu once said, “Know thy self, know thy enemy. A thousand battles, a thousand victories.” Though written with war in mind, the wisdom still holds in today’s boardrooms, brand strategy meetings, and investor updates. To win in business, you must understand the players around you—how they operate, where they excel, and where they fall short. That’s the foundation of competitive analysis.

With global e-commerce expected to surpass $6.3 trillion in 2024, the margin for error is shrinking. Standing still means falling behind. Whether you’re entering a new category or protecting share in a mature one, competitive market research is not optional. It is the lens through which successful businesses assess threats, discover unmet demand, and build strategies that work in real time—not just in quarterly reviews.

This guide breaks down what competitive and market analysis looks like today: how to identify your true competitors, how to analyze the competition effectively, and how to turn research into decisions that matter. From benchmarking product features and pricing to decoding marketing tactics and customer sentiment, we’ll show you how competitive research goes beyond guesswork—driving growth, relevance, and market fit. If you’re serious about market intelligence, it starts here.

Pinpointing Market Competitors: The First Step in Competitive Analysis

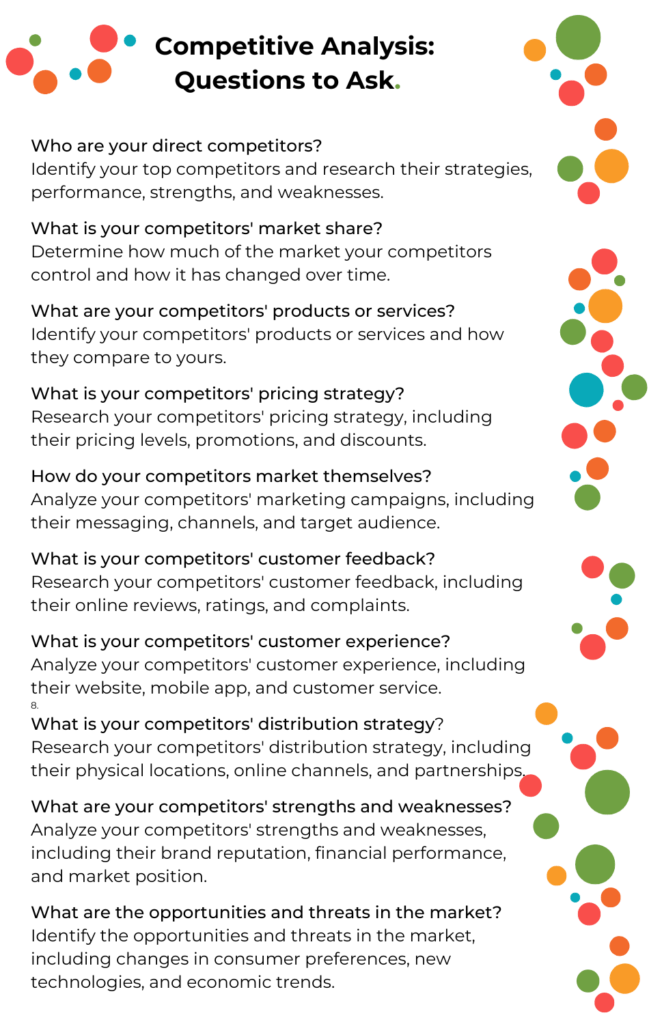

Before you can outperform the competition, you need to know exactly who you’re up against. Identifying market competitors is the foundation of any competitive analysis. This process involves more than just listing similar companies—it requires understanding the competitive dynamics of your category, including both direct and indirect threats.

Direct competitors offer similar products or services and target the same customer base. Think of Nike and Adidas, both vying for the same audience of athletes and lifestyle consumers with nearly identical product lines. These are the companies most likely to impact your market share directly.

Indirect competitors, by contrast, offer alternative solutions to the same customer need. Uber and public transport, for instance, serve the same end goal—getting people from point A to B—but via very different models. Indirect competitors often go unnoticed, yet they can steal share through convenience, pricing, or disruption.

To conduct effective competitive research, start by mapping the landscape. Look at your industry, your product category, and your customer segment. Who else is solving the same problem? Use a mix of methods—customer interviews, online reviews, and digital tools like SEMrush, Similarweb, and Google Trends—to uncover both obvious and less visible players.

Classification matters. Tag each competitor based on proximity to your offering and influence in the market. This will help you prioritize analysis efforts and allocate strategic focus. A niche disruptor in your category may pose a greater threat than a giant in a parallel space.

Don’t stop at naming your competition. Start analyzing competitors in depth: their pricing models, product features, brand voice, marketing channels, and audience engagement strategies. This isn’t just about watching what they do—it’s about learning how they think and how they win.

As Harvard Business Review once noted, “It’s not enough to know who your competitors are. You need to know how they think, what drives them, their goals and values, and their strengths and weaknesses.” That’s the mindset of a modern competitor analysis—and it’s where meaningful strategic differentiation begins.

Analyzing the Competition

Once you’ve identified the key players in your market, the next step in competitive analysis is to examine how those competitors operate. Understanding their market strategies, product offerings, and overall positioning allows you to evaluate your own brand in context. This is the core of competitive market research—and it goes beyond simply watching what others are doing.

Start by assessing the public-facing aspects of each competitor’s business. Visit their websites and review the layout, messaging, and user experience. Are their product or service pages clear and compelling? What pricing models do they use? How are they communicating value? Now extend this evaluation to social media channels. Take note of how often they post, what kind of content they share, and whether customers are engaging. Social listening tools can be helpful in tracking sentiment and spotting shifts in customer perception over time.

To take your competitor market analysis further, immerse yourself in the experience they offer. If applicable, buy their product or sign up for their service. This gives you insight not just into what they sell, but how they onboard, support, and retain customers. This kind of competitive shopping analysis is especially effective in consumer goods, retail, and subscription-based models.

A more structured approach involves conducting a SWOT analysis—mapping each competitor’s strengths, weaknesses, opportunities, and threats. Strengths might include brand loyalty or innovative features, while weaknesses could be inconsistent service or limited product range. This exercise helps you pinpoint where the market is underserved and where your business can stand out.

For example, if you run a productivity software startup and your primary competitor offers a more robust feature set but requires a high subscription fee, you might position your product as a more accessible, streamlined alternative. Or, if you operate a regional restaurant chain, competitor analysis might reveal a gap in healthy, locally sourced menu options—an opportunity to differentiate your brand.

It’s also important to identify what stage of maturity each competitor is in. Are they well-established brands with stable market share or agile newcomers disrupting the space with aggressive pricing or unique offerings? The type of threat each presents requires a different response.

Ultimately, analyzing the competition isn’t about copying what others are doing. It’s about identifying gaps in the market, benchmarking your performance, and uncovering new ways to deliver value. Companies that master competitor analysis aren’t just reacting—they’re positioning themselves to lead.

Assessing Your Competitive Market Position

Once you’ve gathered insights from your competitor research, the next step is to evaluate where your brand stands in comparison. This internal reflection is crucial to understanding not just how you stack up against the competition, but what unique value you offer in the broader competitive landscape.

Start with a fresh SWOT analysis—not of your competitors this time, but of your own business. Identify your strengths: Do you have a loyal customer base? A patented process? A faster delivery time? Then, look at your weaknesses: Are your price points too high? Is your product range limited? Are there gaps in customer service or digital experience? Mapping out your opportunities and threats completes the picture and allows you to build a more realistic and grounded market strategy.

But don’t stop at internal reflection. Turn to your customers. What are they saying in reviews, surveys, and support tickets? What themes emerge on social media or in app store feedback? Positive comments can reaffirm your brand strengths, but more importantly, criticism can uncover blind spots. Customer perception is a critical component of competitive market analysis—especially when you’re trying to out-position other brands in a crowded field.

From there, analyze the foundational elements of your go-to-market strategy. Does your pricing reflect your value proposition in a way that resonates with your target market? Are your marketing channels reaching the right audience—or are you competing in digital spaces your customers no longer frequent? This is where competitive marketing analysis becomes valuable: by understanding how your tactics compare to the broader market, you can realign efforts that may no longer be delivering results.

Here’s a practical example: imagine you’re the founder of a time-tracking app. You’ve identified that your main competitors offer feature-rich platforms, but with steep learning curves and enterprise-level pricing. If your product is intuitive, fast to onboard, and significantly more affordable, this becomes your core positioning. By highlighting simplicity and accessibility in your messaging—while maintaining the right price point—you carve out space in the market that others have overlooked.

Assessing your competitive position isn’t a one-time audit. It’s a continual process that feeds directly into product innovation, pricing strategy, customer experience, and brand communications. As strategist Jay Abraham observed, “Your competitors can teach you everything you need to know about your own customers.” By evaluating both your position and theirs, you build a clearer, more actionable roadmap for sustainable growth.

Turning Insights Into Strategy

“The key to success in competitive analysis is to turn insights into action,” Forbes once noted. It’s a fitting reminder that research is only as valuable as the decisions it shapes. After identifying your competitors and assessing your position in the market, the next step is to develop a clear, actionable roadmap that moves your brand forward.

An effective competitive analysis strategy doesn’t end with observation—it culminates in implementation. That begins by prioritizing the findings from your research. If your analysis reveals a pricing gap that puts you at a disadvantage, this might become your first point of correction. If a new audience segment shows signs of high potential, you may choose to shift messaging or launch a targeted campaign to reach them directly.

Next, translate those priorities into measurable goals. Vague ambitions like “increase visibility” won’t cut it. Instead, define what success looks like. This might mean raising brand awareness by improving your share of voice on social media, increasing product trial rates by 20% over the next quarter, or improving your customer satisfaction score by two points on a verified rating system.

Assigning accountability is equally important. Determine who is responsible for what. Does the marketing team need to refresh positioning across all digital channels? Is product development in charge of building out new features that meet unmet customer needs? Set timelines and budget allocations so expectations are clear and progress can be tracked.

While agility is essential, your strategy also needs consistency. Resist the urge to shift direction with every new data point. Instead, create regular review cycles to evaluate performance and refine your approach. This helps you maintain focus while staying responsive to changing dynamics in the market.

Above all, keep your strategic lens wide. A good action plan doesn’t just respond to current challenges. It anticipates what’s next, drawing from trends uncovered during competitive market research. Whether it’s emerging technology, shifting consumer behavior, or regulatory changes in your industry, an effective action plan positions your brand to lead, not just react.

Turning competitive intelligence into impact requires planning, ownership, and a bias for execution. The insights you’ve gathered should not remain in decks and dashboards—they should show up in your messaging, your pricing, your product roadmap, and ultimately, your market performance.

Why Competitive Analysis Must Be Ongoing

A one-time competitor review is no longer enough. Markets shift rapidly, new entrants emerge with disruptive models, and customer expectations continue to evolve. That’s why competitive market analysis should be a continuous discipline, not a periodic activity. Companies that treat it as an ongoing process are better positioned to anticipate change, spot market gaps early, and respond with agility.

Tracking your competitors regularly allows you to detect patterns across their pricing strategies, product developments, and go-to-market messaging. Monitoring these changes helps your team avoid surprises—whether that’s a sudden price drop, a product feature leap, or a new campaign that shifts customer sentiment.

But the benefits go beyond defending market share. Frequent competitor analysis also uncovers opportunities to lead. It helps you fine-tune your own marketing and positioning based on real-world data, not assumptions. It can reveal underserved segments, emerging industry trends, and even potential partnerships. Done right, it keeps your strategy dynamic and data-informed.

To make competitive research sustainable, businesses should build a monitoring system into their operations. This can include dashboard alerts for pricing changes, regular audits of content and messaging across competitors’ websites, social media sentiment tracking, and quarterly war rooms for strategic recalibration. Several tools—like SEMrush, Similarweb, and Sprout Social—can help automate parts of the process, but the insights still need to be interpreted through your company’s strategic lens.

For companies operating in fast-evolving sectors like tech, energy, or travel, the cadence of competitive reviews might be monthly or even continuous. For those in more stable sectors, a quarterly deep dive may suffice. The key is to never let too much time pass between reviews. The cost of missed signals in a crowded market can be steep.

Airbnb vs. Traditional Hotels: A Case Study in Disruption

The battle between Airbnb and the global hotel industry offers one of the clearest illustrations of how competitive analysis—or the lack of it—can shape market outcomes.

When Airbnb launched in 2008, it didn’t look like a threat. It positioned itself as a community-based travel platform offering affordable stays in local homes. Hotels barely noticed. But by the mid-2010s, Airbnb had become a preferred choice for millions of travelers across the world. Hotels, many of which failed to recognize Airbnb’s distinct value proposition early on, were slow to respond.

Let’s break this down using a simplified competitive SWOT analysis for each side.

Airbnb’s Competitive Advantages:

Lower costs for travelers compared to many hotels.

Unique, authentic experiences in residential neighborhoods.

Flexible inventory without the capital cost of owning properties.

Strong personalization through user profiles, reviews, and recommendations.

Global scalability powered by a digital-first, mobile-native experience.

Airbnb’s Weaknesses and Risks:

Inconsistent guest experiences across hosts.

Ongoing battles with local regulators over zoning, taxes, and permits.

Limited amenities compared to full-service hotels.

Hotels’ Competitive Strengths:

Brand recognition and trust, especially for business and luxury travelers.

Consistency in service and amenities.

Extensive loyalty programs and partnerships with travel platforms.

Hotels’ Key Vulnerabilities:

High overhead and fixed costs.

Slower adaptation to digital booking preferences.

Limited capacity for local flavor or flexible inventory.

By the time traditional hotel brands began adjusting, Airbnb had already reshaped consumer expectations. But some leaders adapted quickly. Marriott International, for example, launched Homes & Villas by Marriott Bonvoy in 2019, combining the flexibility of home rentals with the consistency and perks of a hotel chain. The brand emphasized premium properties with vetted standards and layered on loyalty rewards—tapping into what Airbnb offered but with a hospitality backbone.

This move was the result of competitive research that went beyond copying tactics. Marriott identified a segment—high-end travelers who liked home rentals but wanted trusted service—and built a model around that insight.

What Brands Can Learn From the Airbnb-Hotel Shift

This case isn’t just about travel. It’s a reminder to all industries that your next competitor may not look like you—and that market leadership is fragile without vigilance. Here are the most important takeaways:

1. Early competitive blind spots can be costly. The hotel industry initially viewed Airbnb as a fringe offering. By the time consumer behavior had shifted, major players had to react from behind.

2. Competitive research must expand beyond product parity. Analyzing features is useful, but understanding why customers switch—or stay—is more powerful. Airbnb wasn’t just cheaper; it aligned with a new definition of what meaningful travel looked like.

3. Agility depends on readiness, not speed. The brands that rebounded most effectively had already begun rethinking their models. Marriott’s move wasn’t overnight. It was the result of long-term scenario planning and competitor monitoring.

4. Innovation often starts outside your category. Many brands think competition only exists within their vertical. But real threats—and real opportunities—often emerge at the edges. Disruption can come from companies solving different problems in adjacent markets.

5. Market analysis and competition tracking must include sentiment. Beyond metrics, it’s important to understand how consumers feel about your competitors. Airbnb’s story was not just about supply, but about emotional resonance—belonging, autonomy, and exploration.

Case Studies in Competitive Market Analysis

Effective competitive analysis has shaped some of the most important business victories of the last few decades. When done well, it does more than track rival brands. It reveals market shifts, identifies consumer preferences, and helps companies reimagine their position in the market. The following examples highlight how detailed competitor research can lead to transformative strategy changes and long-term dominance.

Coca-Cola vs. Pepsi: A Lesson in Brand Positioning

The rivalry between Coca-Cola and Pepsi is one of the most well-known in marketing history. By the early 2000s, the competition had reached a point where both brands needed to do more than release new flavors or launch celebrity endorsements. Coca-Cola embarked on an extensive competitor analysis, not only examining Pepsi’s advertising tactics but also evaluating market data, pricing models, and emerging youth culture trends.

What Coca-Cola discovered was that Pepsi had gained a younger audience by leaning into pop culture and positioning itself as a modern, rebellious brand. In response, Coca-Cola pivoted with a nostalgia-based campaign that reinforced its identity as a timeless, family-oriented classic. Rather than mimic Pepsi’s tone, Coca-Cola chose to double down on what made it unique. This approach helped the company stabilize its market share and protect its legacy, proving that competitive research is as much about refining your own voice as it is about watching others.

Netflix vs. Blockbuster: Timing and Tech Disruption

In the early 2000s, Netflix was a relatively obscure DVD-by-mail service. Blockbuster, with its thousands of storefronts, appeared untouchable. But Netflix studied its competitor’s weaknesses closely, especially its reliance on late fees, store-based inventory, and a one-size-fits-all business model. Through a combination of customer surveys, market trend analysis, and behavioral research, Netflix identified a clear consumer pain point: people disliked the inconvenience of driving to stores and paying penalties for returns.

Instead of going head-to-head with Blockbuster on physical rentals, Netflix shifted its strategy toward digital streaming. The data pointed to a growing appetite for on-demand content and greater flexibility. While Blockbuster clung to its retail footprint, Netflix invested in technology and content licensing. By the time Blockbuster attempted to pivot, Netflix had already secured customer loyalty and brand equity in the new streaming model.

This is a classic example of how competitive market research can uncover a strategic inflection point. Netflix did not win by outspending Blockbuster. It won by observing customer frustration and using competitor inertia to its advantage.

Amazon vs. Barnes & Noble: Scaling Beyond Books

Barnes & Noble once held the title of the largest bookseller in the United States. With expansive retail stores, in-house cafés, and curated selections, it offered an immersive experience that seemed difficult to replicate online. However, Amazon did not just aim to sell books more cheaply. It used competitive analysis to understand the limitations of the traditional bookstore model.

By closely examining Barnes & Noble’s inventory costs, supply chain, and reliance on physical locations, Amazon identified opportunities for disruption. The company recognized that a broader product range, faster delivery options, and algorithmic recommendations could address consumer needs more efficiently than in-store browsing.

Amazon’s early strategy involved expanding categories, reducing prices through scale, and optimizing logistics. As e-commerce adoption accelerated, Barnes & Noble’s decision to focus on in-store traffic and physical expansion left it vulnerable. Although it eventually developed an online store and e-reader, the delay in response cost it significant ground.

What sets this case apart is the scope of the analysis. Amazon was not just competing for book sales. It was mapping out the future of retail. By monitoring its competitors and adapting to digital behaviors quickly, Amazon moved from niche player to global marketplace leader.

What These Case Studies Reveal About Competitive Research

Each of these companies—Coca-Cola, Netflix, and Amazon—used competitive intelligence not just to react, but to lead. Their success was not based on mimicry. It stemmed from a clear understanding of the market, the gaps left by competitors, and the willingness to act on those insights.

Whether you are a legacy brand defending your market share or a challenger brand looking for an entry point, competitive analysis can serve as a compass. It highlights what to emulate, what to avoid, and where to innovate. These examples also demonstrate that success often comes from framing competition in terms of consumer behavior rather than just product features.

For businesses investing in competitive and market analysis today, the stakes are even higher. Markets evolve faster, customers are more informed, and technology shortens the life cycle of strategic advantages. By studying competitors through multiple lenses—pricing, positioning, experience, and sentiment—you give your brand the insight it needs to not only survive, but shape the future of its category.

Tools and Resources to Power Your Competitive Market Analysis

Conducting a competitive analysis is not simply about observing rivals. It requires a structured approach supported by the right tools and resources. Whether you are assessing the competition to inform pricing, product development, marketing, or strategic planning, using up-to-date methods and insights is essential for success. Below are some of the most effective tools and approaches available for brands aiming to conduct sophisticated competitor and market analysis.

1. Competitive Analysis Templates For those starting out or standardizing their internal process, templates provide an essential structure. Many marketing platforms and consultancy websites offer free or paid templates designed to guide companies through competitive market analysis. These include SWOT matrices, competitor profiling sheets, and comparison dashboards. A good template will help ensure you consider key components such as target audiences, pricing, value proposition, customer experience, and digital footprint.

2. Industry Reports and Market Research Publications Reliable market research is the foundation of any credible competitor analysis. Reports from sources like Statista, IBISWorld, and Mintel provide valuable insights into market share, consumer trends, macroeconomic factors, and competitive shifts across industries. For businesses looking to understand the broader competitive landscape or benchmark their performance, subscribing to these reports—or working with a market research agency—is often worth the investment.

3. Digital Competitive Intelligence Tools Tools like SEMrush, SimilarWeb, Ahrefs, and SpyFu allow brands to track digital marketing performance. You can compare domain traffic, keyword rankings, paid advertising spend, backlink strategies, and content effectiveness. These platforms are indispensable for digital-first companies and are increasingly being used by traditional players to stay competitive in online markets.

4. Social Media and Sentiment Analytics Platforms such as Brandwatch, Hootsuite Insights, or Sprout Social can help assess public perception and monitor engagement metrics. Social listening tools give a real-time view of how customers are responding to competitors’ campaigns, product launches, and customer service efforts. This type of insight goes beyond what traditional surveys can capture and feeds into a more dynamic understanding of your competitors’ brand health.

5. Competitive Shopping and Product Audits One form of competitive research often underused is mystery shopping or competitor product testing. This includes evaluating customer journeys, delivery experiences, product quality, and post-sale support. It is particularly relevant for companies conducting competitive shopping analysis in retail, ecommerce, and hospitality.

6. Market Research and Competitor Analysis Agencies If your business needs deeper insight or lacks in-house capacity, working with a specialist competitor analysis agency can add substantial value. These firms offer customized competitor research, consumer segmentation, trend forecasting, and benchmarking tailored to your strategic goals. They can also assist in conducting market analysis and competition reviews that are specific to geographic regions or industry verticals.

Whether you’re in B2B or consumer markets, these tools and approaches offer scalable options to make your competitor intelligence more actionable and accurate.

Strategies for Staying Ahead in a Competitive Market

Competitive analysis is most valuable when it leads to clear actions. The true benefit of assessing competition is not only understanding where you stand, but also using those insights to stay ahead. Below are five practical ways companies are maintaining their edge in 2024 and beyond.