The global health and wellness industry is booming. Already a top priority for many consumers pre-Covid, health and wellness has come into even sharper focus as a result of the pandemic. Research from McKinsey estimates that the global wellness market is worth $1.5 trillion and is growing fast – at a rate of 5-10% per year. But what are the big health and wellness trends for 2021 that brands need to watch?

Four key health and wellness trends for 2021

This blog post summarises 4 key trends from our latest report: Health and wellness trends for 2021. These are:

- My health on my terms. Advances in tracking and testing are facilitating personalized health and nutrition recommendations on demand

- Mental fitness. Consumers will take a more proactive and preventative approach to mental health

- The science of sleep. The global sleep economy shows no signs of slowing down, but innovation in the category will be driven by a new focus on circadian health.

- Function at the fore. No longer limited to just physical health, brands are focusing on products to better the body and the mind.

Read the summary below or download the full report to learn more about these trends and how brands can respond. It contains inspiring cases studies of companies across the world who are innovating to capitalize on these trends.

My health on my terms

One of the most significant developments in health and wellness has been the rapid advances in tracking and testing, which are facilitating personalised health and wellness recommendations on demand.

Wearables are becoming ever more sophisticated. The models on the market now allow consumers to track more granular metrics than ever before, with Mind Body Green hailing this a new era of “micro-tracking”. Not only are wearables collecting a wider range of data, they’re using this to better empower their users. Oura, for instance, the world’s first wearable ring, provides a “readiness score” to help users understand when they are at their best – both mentally and physically – as well as when they should focus on recovery.

Similar developments are happening in the world of testing, with companies springing up that allow users to complete a series of tests at home, and then personalise their recommendations based on this. We profile the best of these in the full report but the really interesting thing about these examples is that, for the first time, they have real potential to enter the mainstream. In the past, in-home testing has been a barrier to personalised health and nutrition, but now, greater familiarity with the concept as a result of the pandemic could open the door to new services which combine tracking with testing to create hyper personalised recommendations at speed.

There’s certainly interest in these kinds of services, with 88% of consumers in the US, UK and Germany prioritising personalisation in health and wellness as much as, or more than, they did in the past two to three years, according to the McKinsey study.

Mental fitness

Over the last decade, mental health has become an increasingly important part of the conversation when it comes to health and wellness. This has come into even sharper focus as a result of the pandemic. The impact of the virus and the resulting lockdowns have seen anxiety and depression skyrocket and, in line with this, mental health has become a key focus. In China, for instance, 87% of consumers are focused on taking care of their mental health, according to research by PWC conducted after the onset of the pandemic.

This isn’t a short- term trend. Research we conducted to determine which of the behaviours adopted during the pandemic will persist in the long-term found that undertaking activities to support mental health is one of the areas with greatest sticking power. Businesses are increasingly prioritising mental health too. Recent research we conducted in partnership with Bloomberg found that 66% of companies are engaging an external vendor to provide healthcare / wellbeing training for their employees and half are looking to support employees with mental health and stress management.

In line with this growing recognition of the importance of mental health, we see the concept of mental fitness coming to the fore. What do we mean by this? This a move towards taking a more proactive and preventative approach to mental health, where consumers manage their mental health in the same way that they manage their physical health. The US is a market that’s really leading the way here. We’ve already seen a whole host of brands gaining traction but one of the most interesting is a company called Coa, which bills itself as the country’s first “mental health gym”. We profile Coa and other brands leading the way in our full report.

Free report

Health and wellness trends for 2021

The global health and wellness industry is going from strength to strength. Already important to consumers before the pandemic, health and wellness have come into even sharper focus, with the industry undergoing significant transformation in response to Covid.

To help brands navigate these changes, we’ve developed a new report exploring 4 key trends that will shape health and wellness in 2021, profiling the brands and innovations leading the way.

Download the reportThe science of sleep

Sleep is big business – with the industry set to be worth a massive $585 billion by 2024 according to Statistica. The impact of the pandemic is fuelling growth in this sector – with consumers placing an increasing emphasis on quality sleep against a backdrop of anxiety and stress.

This is leading to a more scientific approach to sleep. The Global Wellness Summit predicts that a new focus on circadian health will shape the products and services we see in the category. (A number of these – from a smart mattress to connected lighting – are profiled in our report.) Circadian health relates to aligning behaviors with our natural circadian rhythms – 24 hour cycles such as the sleep-wake cycle, which are influenced by external factors like natural light and temperature.

Shifting the way we think about sleep to place greater emphasis on circadian rhythms could have broader implications when it comes to other behaviours, for instance, disconnecting from devices before bed or the way we care for our skin, making this an interesting space to watch.

Function at the fore

The fourth and final big trend we see is a growing interest in functional food and beverages that support better physical and mental health. The most evident application of this is in the field of immunity boosting food and drink. According to research from Innova Market Insights, 60% of consumers globally are seeking out food and beverage products that support immune health and we’ve seen a seen a slew of product launches in this space as brands seek to capitalise on this trend. Increasingly, we’re seeing innovation extending beyond this to food and beverage products that support the mind. We feature the best of these in the full report. For brands looking to tap into this trend, this is a relatively nascent category so there’s real potential here, as well as for cross-over products to improve both physical and mental health.

To learn more, download the full report: Health and wellness trends for 2021

To learn more about how these trends, how they are evolving and the brands leading the way, download the full report. Alternatively if you’d like to speak to us to understand more about how these trends are playing out in your market, get in touch.

Trusted by

Trusted by

The arrival of Covid-19 has brought with it dramatic changes in food and drink purchase patterns. Shelf-stable food like pasta, rice and canned goods flew off the shelves. Immune system boosting ingredients were top of the shopping list. But which behaviours will stick and what are the longer term food industry trends to watch?

We spoke to consumers in 10 countries, as well as our own internal food and beverage experts to understand the global picture and the local nuances and trends in each market. We wanted to understand how people are eating and drinking in this new normal, and what implications this has for the future.

We’ve summarised the key global and local trends in this blog post but for the full findings, download the report: Understanding the Impact of Covid-19: Food Industry Trends for 2020 and Beyond.

Global food industry trends for 2020 and beyond

The pandemic has improved eating and drinking habits across the world

Over half (53%) of the consumers we spoke to told us that since the onset of the pandemic, what they eat and drink has changed for the better. Some countries like India and Vietnam have seen a big swing towards healthier diets, whereas others like the US, UK and Japan have been more consistent. Overall, very few people (just 6%) believe their diet has changed for the worse.

People are cooking more at home and they’re eating more fresh fruit and vegetables

With more time at home, and health high on the agenda, it’s unsurprising that half of consumers globally (51%) are now cooking more for themselves and their families. This trend is more prevalent in some Asian markets, such as India, China, Thailand and Vietnam, than it is in the US, UK or Japan. But even in this market, consumers have found an innovative workaround to sourcing home-cooked meals. Over the past few months, professional chef / dietician delivery services like Sharedine have boomed in Japan. This is where a personal chef will come to a customer’s house and cook a number of dishes from scratch that can be reheated over the coming days. The service even includes grocery delivery!

At a global level, people are also more conscious of what they eat, with a real focus on fresh produce. Half of consumers globally (51%) tell us they are eating more fresh fruit and vegetables. This is more significant than any other dietary changes, such as eating more grains and nuts (adopted by 29%) or eating more meat-free products or dairy and cheese (practiced by just 16% and 13% respectively).

Health-conscious consumers are looking to boost their immune systems and brands are responding

Even now long after the onset of the pandemic, immune-boosting solutions are still at the top of consumers’ shopping lists. Consumers in markets like India are looking to natural ingredients. But others, like those in Thailand and China are making use of a new range of RTD products that have sprung up to meet this need. The “water plus” category has boomed in Thailand, with brands such as Yanhee Vitamin Water, B’lue, VITADAY Vitamin Water and PH Plus 8.5 Alkaline Water coming to the fore. In China, product launches have included milk with immune globulin, Vitamin C fruit tea and Chinese jujube drinks.

Free report

Understanding the impact of Covid-19: Food industry trends for 2020 and beyond

The arrival of Covid-19 brought with it dramatic changes in food and drink purchase patterns. Shelf-stable food like pasta, rice and canned goods flew off the shelves. Immune system boosting ingredients were top of the shopping list. But which behaviours will stick and what are the longer term trends to watch in food and drink?

Download nowWorries about the origin of food are one of the key food industry trends for 2020 and beyond

When asked which of the behaviours they’d adopted in the pandemic that they’d continue in future, being conscious of where the produce I consume originates from for safety / health reasons came out top. We see this reflected in consumer behaviour. Some people in countries like Vietnam and Indonesia have moved away from visiting wet markets, opting instead for mini supermarkets or online solutions. In some markets, there are also significant groups of consumers that are opting to eat more meat-free products, perceived to be less prone to infection. This amounts to 32% of consumers in Vietnam, 28% in India and 23% in China. With these concerns top of mind for many consumers, it’s the brands that prioritise hygiene and safety that will come out on top. We’re already seeing some great examples of this happening, with the help of technology. One example is Haidilao. This hotpot restaurant in Beijing has installed smart robotic arms to prepare and deliver raw meat and fresh vegetables. It’s also introduced technology to track and dispose of food that has passed its expiry date.

Supporting local is a key consideration for many consumers

Across the world people are doing their bit to keep local food and beverage brands afloat. This looks set to continue in future. When asked which of the behaviours they’d adopted in the pandemic that they’d continue, supporting local produce and food and beverage brands came out second highest.

In Japan, this trend has manifested itself in the 応援消費 (Consume To Support) movement. This initiative that went viral, ranking first amongst the top 10 consumer trends in the first half of 2020 according to Rakuten, an online retail giant and Nikkei, a flagship financial newspaper. The term was first created and gained popularity in 2011 when a 3.11 earthquake shook the eastern part of Japan and people showed their support through making purchases from the damaged areas. In the pandemic, we saw a resurgence of this. Consumers purchased from the food and beverage brands hardest hit – farms, manufacturers and restaurants with excess stock – thanks to innovative apps like Pocket Marche and TABETE.

We’ve seen similar movements in other markets. In Indonesia #belidariteman (buy from a friend) was promoted by the Association of Indonesian Young Entrepreneurs (HIPMI) encouraging people to support local. In the Philippines, the traditional value of “Bayanihan” which translates as “spirit of communal unity” has seen Filipinos shopping from local food and beverage brands in these difficult times.

With local being an important purchase consideration for consumers both now and in the future, brands will do well to emphasize their heritage and role in the community going forwards.

Consumers are looking to food and drink as escapism to create occasions at home

As people spend more time at home, there’s a real opportunity for brands to help consumers create special occasions with their loved ones through the power of food and drink. This could be through providing inspiration for at-home events and special recipes for consumers to cook themselves. It could also be achieved by creating products, services and experiences that can be delivered at home. There are some great examples of this emerging around the world. In Singapore, bar and restaurant, Tippling Club, is offering virtual cook-along sessions with its in-house chef. In Hong Kong, Café Earl Grey is delivering restaurant signatures with simple instructions to cook and assemble at home. These dishes are accompanied by an extensive selection of curated wines and bottled cocktails. And in the Philippines, restaurants are delivering uncooked ingredients so that people can cook their favourite dishes at home.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Online shopping is on the rise but this is playing out differently in different markets

Food and beverage brands have had to innovate to survive in the wake of local restrictions. Online has played a critical role in this transformation. Consumers across markets have experienced the benefits of online shopping first hand, accelerating its growth. But this has played out differently in different markets. In Vietnam, ghost kitchens have been set up to meet the growing demand for meal delivery. In Indonesia, a jastip service allows consumers to make and receive orders from local wet markets via WhatsApp. And in the UK, where online grocery is more well established, growing numbers of older customers are moving their grocery shopping online. In 2019, just 8% of over 55s in the UK had bought food and essentials online. This figure has now soared to 25% according to the How Britain Shops Online report.

Country specific food industry trends

Food industry trends in the UK

One of the key global trends we see in the UK is the shift towards supporting local. Office workers in the UK have been encouraged to work from home for the majority of 2020, meaning that food and drink spend has been concentrated closer to home – and we expect to see this continue as working patterns shift as a result of the pandemic. According to Mastercard data, it’s been people shopping and eating out locally, rather than spending money in Central London, that has driven the economic recovery in London. Other key trends in this market include the growing number of silver surfers that are embracing to online grocery shopping as mentioned above and rise of at-home food and drink occasions. As in other markets, brands are anticipating consumers will spend more time at home, and catering to this with services such as online cooking classes and delivery collaborations.

Food industry trends in the US

We expect to see consumers continuing to eat and drink more at home in the US too, as many office workers continue to remotely, and city dwellers flee to the suburbs. Whilst consumers are enjoying cooking at home and planning to do more of it in future, they’re are also ordering more takeout, and looking to meal kit companies for ease and convenience. Attitudes towards health in the US depart from the global trend. Whilst 53% of consumers globally tell us that what they eat or drink has changed for the better, in America only 25% think this is the case. In the US, consumers are viewing health more holistically. Whilst some are looking to food and drink to support physical health, others are using food as a tool to support their mental health, with two thirds of Americans eating more comfort food than before.

Food industry trends in Singapore

Global trends such as the rise of online shopping and a growing focus on health and wellness are reflected in Singapore. In fact, an AIA survey conducted prior to Phase Two of safe reopening found that Singaporeans are allocating the highest portion of their expenses on healthier meal choices. One trend that is more specific to Singapore is the growing importance of sustainability. When it comes to sustainability efforts, Singapore falls behind many other nations in terms of recycling, plastic-use reduction, and food wastage reduction, and this has come into sharper focus as a result of the pandemic, alongside more recent government efforts to achieve a Zero Waste Singapore. In response, we’re starting to see the rise of more sustainable packaging, “ugly” produce and bulk food stores.

Food industry trends in Vietnam

Vietnam has seen big changes in the channels people use for shopping. Online meal delivery has boomed as restaurants have pivoted, and ever more Vietnamese consumers are turning to the mini supermarket, as worries about food safety and origin come to the fore. In line with this, organic food is also growing in popularity, although high prices mean that at present this trend is confined to the middle class.

Food industry trends in China

In China and Hong Kong, global trends around health and eating at home are particularly important, with 86% of Chinese respondents acknowledging their desire to eat at home even after the pandemic ends according to Nielsen. Concerns about food safety are also front of mind, and in response we’re seeing a growing trend towards automation and contactless processes in manufacturing and distribution.

Food industry trends in Thailand

As in Vietnam, meal delivery in Thailand has boomed, accelerating the adoption of online and mobile banking and contactless payment methods. The global trend towards an increasing emphasis on health is evident in Thailand, too with 71% cooking more for themselves and their families and 62% consuming more fresh fruit and vegetables. Many Thai consumers are also looking towards beverages as a way of looking after their health. Drinks containing Vitamin C have seen 47% growth compared

to last year.

Food industry trends in India

Like their counterparts in Thailand, Indian consumers are looking for immune boosting products, but many of the specific trends we see playing out in this market are driven by food safety concerns. As mentioned previously, a significant number of Indian consumers are eating more meat-free food due to worries about infection, and they’re also buying more packaged food. Against this backdrop, street food vendors have had to pivot, elevating their offering, leading to the emergence of gourmet street food.

Food industry trends in Japan

As mentioned above Japanese consumers have been quick to support local brands through the 応援消費 (Consume To Support) movement. This is a trend that we believe will persist in Japan, albeit not as prominently as it does on a global scale. Our research shows that 1 in 4 consumers in the country say they will be more conscious of supporting local produce and food and beverage brands in future, compared to 4 in 10 globally. One emerging trend that is quite specific to Japan is the move towards stocking up on food. In most countries this behaviour peaked at the height of the pandemic and has since subsided but in Japan 41% of consumers plan to ‘stock up’ on essentials rather than buying day-to-day in future and 35% are intending to buy more frozen or tinned produce. This can be explained by looking at the specific experience of the Japanese people. In response to natural disasters like earthquakes, typhoons, flooding and landslides, Japanese consumers are used to having to stock up.

Food industry trends in the Philippines

We see this trend towards bulk buying emerging in the Philippines too, where 48% of consumers say they plan to ‘stock up’ on essentials instead of buying day-to-day. Global trends around eating more healthily are also important in the Philippines, which is significant given that the traditional Filipino diet is higher in total fat, saturated fat, and cholesterol than most Asian diets.

Food industry trends in Indonesia

Trends in Indonesia closely mirror those seen globally. There’s been an uptick in online grocery shopping, with a large proportion of Indonesian grocery shoppers (59%) having used e-commerce sites for this purpose according to a Snapcart survey carried out in May. People have also started to adopt online shopping in new categories, such as OTC, multivitamins / supplements, herbal products, and even RX drugs. Cooking more at home, and supporting local food and drink businesses are also key trends in this market.

To learn more about the food industry trends in each market, download the full report – it’s packed full of facts, stats and examples from each country. Alternatively, if you need further support in understanding changing consumer behaviour in your market, please get in touch with us. We have a wealth of experience in food and beverage, having worked with the likes of Mars, Unilever and Arla, and would be happy to share our expertise.

Trusted by

Trusted by

As a result of the COVID-19 lockdowns, education institutions across the globe have faced a myriad of challenges, including the move to distance learning and finding new ways to support pupils. Students have also had to adapt with the support of an in-person learning environment

Now that some educational institutions are emerging from the pandemic, it will be important not just to address short term needs but also to identify innovations that can be adopted to improve student learning in the long run.

This piece explores three key challenges to address in the short term but also considers the long-term implications of what these new changes may bring. The 3 themes we’ll be looking at are:

- The role of a “classroom” and going beyond physical spaces

- Rethinking the way we share knowledge

- Addressing current inequalities and what educators can do to ensure the future success of students

Where is the classroom?

Short-term trends

As governments and educational institutions make decisions on when and how to reopen schools, health and safety is naturally front of mind. Some schools have opened with strict checking procedures in place. In Shanghai, for instance, students are required to enter the school building via a thermal scanner and there are multiple posters in place highlighting the measures in place to tackle coronavirus. In other schools, remote learning is still continuing as only limited numbers of pupils return. Schools in New South Wales, Australia, for example, have re-opened but are only allowing students to attend one day a week on a staggered basis. Whatever the approach, the priority continues to be safeguarding people’s wellbeing and schools will observe and learn from countries that are practicing safe re-opening procedures.

Long-term trends

However, the COVID crisis has also demonstrated that classrooms are not the only places where education can take place. The pandemic has highlighted that learning can take place at any time, anywhere and in any way. It’s clear that the opportunities offered by digital capabilities will go well beyond its temporarily use during the crisis.

Technology can enable teachers and students to access massive amounts of digital resources, most of which are free to use. Examples from other countries have also shown that the delivery of information through various means – TV, online, mobile – can work to help engage students. What’s more, AI and digital technology are now able to capture data to measure students’ progress so that learning can be adjusted based on ongoing assessments rather than through high stakes exams.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

Rethinking Knowledge Sharing

Short-term trends

Just as students are adjusting to distance learning, most teachers are also new to teaching online and have had to quickly adapt their lessons to an online format that keeps pupils engaged.

But teachers don’t just need the technological tools to facilitate online learning. They need resources to help enhance their teaching practice. A number of initiatives have sprung up around the world to facilitate this. In South Korea, the Education and Research Information Service offers an online platform to facilitate the sharing of materials created by teachers and in the United Arab Emirates, the Ministry of Education invited over 40,000 teachers to take part in a ‘Be an online tutor in 24 hours’ course. Global organizations such as the Khan Academy, TEDed, Google Arts & Culture are also continually providing relevant education resources for students and teachers.

Long-term trends

In the long-term, we may see a new form of teaching emerging. In a world where students can access to knowledge through a few clicks, educators will need to review and potentially redefine their role in the classroom.

The emphasis should be not only on the delivery of content but also on generating engagement. Educators need to learn to create a positive experience within a digital context – one that is more interactive and engaging. One organisation leading the way on this is Singapore’s SIT University, which has created training materials for lecturers to provide online learning. The topics covered how to create narrated slides, how to run effective live streaming classes, how to design alternative assessments, and the use of online proctoring tools for assessments.

Addressing current inequalities and what educators can do to ensure the future success of students

Short-term trends

While technology has helped many students continue their education at home, data from UNESCO has found that in other ways, it has exacerbated the digital divide. Half of all students do not have access to a computer and more than 40% have no internet access at home.

Students living in rural areas, low-income households, students with special needs and those living in less developed areas face issues with a lack of resources including not having the technology needed for remote learning.

Governments, private companies, and educational institutions need to be able to work in partnership to ensure that needs of all students are met. Success stories from around the world can provide inspiration. In France, the University of Strasbourg identified students whose lack of resources jeopardised their ability to continue their education, setting up an Emergency Fund and distributing more than a hundred computers to students in need. China offered mobile data packages, telecom subsidies and repurposed some of the state-run television channel to air lesson plans for K–12 education in remote regions. Italy put together an €85 million Euro package to support distance learning for 8.5 million students and improve connectivity in isolated areas.

Long-term trends

While COVID-19 has fast-tracked the need to acquire digital skills, we also cannot forget the education students will need to prepare them for the workplace of the future.

As a result of the pandemic, the demand for certain jobs and specialities will decline, whilst otherareas come to the fore. Educational institutions need to be flexible enough to adapt their curriculum and resources to meet students’ and workforces’ changing needs.

There will continue to be a need to train people in emerging digital skills but learners will also need “non-automatable” skills. According to the World Economic Forum’s Future of Jobs Survey, “a wide range of occupations will require a higher degree of cognitive abilities — such as creativity, logical reasoning and problem sensitivity — as part of their core skill set.” Institutions who more readily recognise and adapt their curriculum and resources to meet these needs are more likely to thrive moving forwards.

The automotive industry has been one of the hardest hit by the pandemic. Cars have lain dormant in driveways for months as a result of lockdowns across the world, and economic shutdowns hit supply chains, with reports of some manufacturers even resorting to flying parts across the world in suitcases.

But as consumers emerge into a ‘new normal’, what does this mean for the automotive industry? What are the trends to watch – both in the short and the long-term?

In this article, our auto experts across the UK, Thailand and Indonesia, Bianca Abulafia, Digo Alanda and Kajornkiat Kiatsunthorn explore 3 key areas:

- Changing purchase patterns

- The future of electric

- The digital path to purchase

Changing purchase patterns

Short term

In the short-term, we expect to see growth in the second hand and luxury end of the market especially.

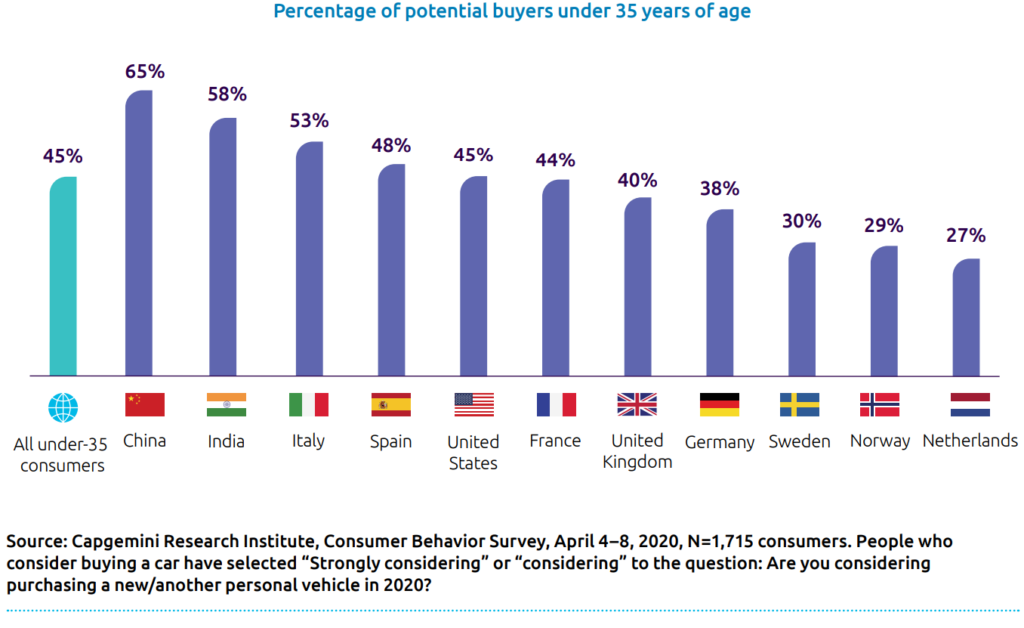

The pandemic has resulted in a renewed focus on the car as hygiene concerns have come to the fore. This has resulted in those that have previously shunned car ownership such as urbanites and young people re-evaluating their stance. In the US, a cars.com study showed that 20% of people who don’t own a car are thinking of buying one, and this figure rises when we hone in on young people. A recent global Capgemini survey of under 35s shows that 45% are considering buying a car and this is highest in countries that have been hardest hit by the pandemic.

We have talked about the emergence of “revenge buying” in other sectors, and we expect this to manifest in the automotive industry within the second-hand market as a more affordable option for younger buyers. “Revenge buying” is also relevant at the luxury end of the market. As a result of being able to save, the budget of some affluent buyers has increased, meaning that they’re now able to trade up. Volvo’s Chief Executive notes this has happened in China, where the company has seen a 20% increase in sales compared to 2019. “People are really tired of sitting at home locked and they really want to go out and buy.” Outside of this, we expect sales to suffer, with existing car owners putting off purchases in the midst of economic instability.

Long-term

Looking at the long-term impact, it will take some time until car sales return to pre-COVID levels. An ING report, looks back to the 2008 financial crisis for indicators, highlighting that it took 11 months for vehicle sales to recover in this instance. But if we consider that this pandemic has brought lifestyle and behavioural changes, in addition to economic instability, it’s much harder to predict.

In the long-term, will we see a permanent shift towards home working that encourages people to move out of urban centres, necessitating the need for a car? Will increased domestic tourism result in a desire to have access to a car for longer trips – ushering in an opportunity for shared ownership of vehicles? The automotive industry doesn’t exist in a vacuum and it will be vital for auto manufacturers to observe the broad trends to understand where they can play a role.

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

The digital path to purchase

Short-term

Car manufacturers have had to rapidly adapt to a new sales environment, as they seek to comply with social distancing measures and meet the needs of the more cautious shopper. Capgemini’s COVID-19 and The Automotive Consumer report indicates that 46% of consumers want to minimise visits to dealerships to compare offers, instead preferring to do this online. We’ve seen lots of innovative responses to this. In China, for instance, Volkswagen has trained 70,000 employees to communicate with customers online, even livestreaming from dealerships via TikTok and Kuaishou.

Long-term

In the long-term, we only expect this to continue. The impact of coronavirus has acted as a catalyst for the digital transformation of many industries, sparking changes in consumer behaviour that were thought to take years. Automotive will be no exception as people seek the convenience that they’re experiencing in their interactions with other brands and industries. This will be particularly important in the research phase but we believe it will also extend to online purchase and home delivery, with a recent Think with Google survey finding that 18% of people would buy a vehicle sooner if there was an online purchase option. The desire for convenience could also impact the after sales experience with servicing being carried out at home.

The future of electric

Short-term

In the immediate term, economic instability, plus the appeal of lower oil prices, could dissuade car buyers from making the move to electric. However, we don’t expect this to last long, with any savings from oil prices likely to be temporary, and not significant enough in the long-term to fundamentally influence decisions.

One area to watch is other electric transportation options beyond the car – such as scooters and bikes. As people avoid public transport and seek other routes around the city, governments are having to radically rethink how they can support this. The UK has announced that improvements in cycling infrastructure and trials to allow rented e-scooters on the streets have been fast-tracked, which could encourage people to start exploring electric bikes and scooters as alternative options for commuting. Increased familiarity with electric powered means of transportation could result in a greater adoption of motorbikes or cars.

Long-term

When we look at the long-term view, we don’t expect the shift towards electric to be significantly impacted. From the canals in Venice being clear enough to see the fish to Nasa satellite images showing the dramatic drop into pollution levels in China, the upsides of the lockdown on the environment have been well documented – with many consumers acknowledging benefits of this on their quality of life.

This could influence purchase behaviours in the longer term, with consumers wanting to do their bit for the environment at the point at which economic conditions become more favourable for them to do so. But more significantly, changing consumer sentiment towards the environment is also likely to increase pressure on governments to bolster schemes to incentivise electric car ownership, making them a more financially attractive proposition to car buyers. In fact, this is something that has already happened in China in the wake of the pandemic, with some cities announcing subsidies for new electric vehicles, and others upping their investment in the associated infrastructure.

We also shouldn’t forget the status symbol factor, particularly in the luxury segment. Our research has shown that owning an electric car represents a new way to demonstrate wealth and status, and we don’t see this diminishing any time soon.

This week marks a change in the focus for many news outlets and governments. From protection to productivity – as leaders grapple with the challenge of getting economies moving again. There is more confidence in some countries’ approach and communication (New Zealand) than in others (UK, US – looking at you!). However, in all situations, there is an agreement that the world we are returning to is not the same as we left.

The workplace is no different. The Straits Times last week carried a story from Singapore’s Minister for Trade and Industry about how ‘working from home will continue to be the norm for the majority even after restrictions are lifted. Forbes has taken this further and stated that “The Covid-19 coronavirus is becoming the accelerator for one of the greatest workplace transformations of our lifetime. How we work, exercise, shop, learn, communicate, and of course, where we work, will be changed forever!”

However, for those of us that have been able to continue our working life from the safety of our home, will the adjustment back to the office be harder than the adjustment to work at home? US Tech website BuiltIn quote a CEO who states that it takes “6 to 12 weeks for a smooth transition from on-site to remote working”. For many, this timeframe has already been met. People are working at home, people are productive, and…are people are starting to realise the benefits: lack of travel, more flexible hours, ability to help with childcare … With many positives to working from home, what does this mean for the future of work?

Certainly, in the short term, offices will be sparse locations. Governments are still advising those who can work from home to work from home. If you do return, social distancing measures will have to be evident. Here in Singapore – if you are do not implement safe management of your workplace, the government can fine you or even shut down operations for errant employers. The Economist offers up an opinion piece on how that distancing may look. A 2m gap between desks could reduce the capacity of workspaces to 30-35% of the pre-Covid lockdown. The piece also details a high-tech solution before the lockdown in UAE, with contactless pathways from door to desk, relying on motion sensors and facial coding to open doors. Having a reduced workforce onsite, or investing in tech are expensive options for most firms – but what about the office itself. What role will it play?

Stay ahead

Get regular insights

Keep up to date with the latest insights from our research as well as all our company news in our free monthly newsletter.

At Kadence, we have managed to retain productivity. Completing projects to time, and collaborating using video calls, Slack, online whiteboards, and Google Docs. What we really miss is the unintended interaction with others. Overhearing conversations and adding some extra insights, hearing the chatter of voices and the energy in the room. At Kadence, we also have some onsite resources that are hard to replicate offsite. Focus group viewing facilities, a call center, and workshop facilities will all be utilized in the future. However, the floor space may change. We might be more open to a higher proportion of staff working from offsite at any one time. Rather than whole team meetings and designated desks, perhaps our floor space will have more meeting areas. So that project teams can come together in an environment to bounce off each other, then return home to execute the required tasks. Vice talk of new rituals being formed to bring meaning to home working and The Atlantic talk about dress codes changing in life after COVID.

However, perhaps the most important change will be in HR, not in the physical use of space. If people are going to work from offsite more often, how does team bonding work? How will you help teams to prioritize their workloads? How will you manage line reports? These skills will require even more attuned social skills and people managers.

I would foresee offices being more flexible environments. Bringing people together when it matters, but keeping people apart for safety….and for their own personal preference. As a result, team dynamics will change. Managers will need to juggle a wider array of pastoral matters. The corporate cultures that thrive will be flatter, more candid, and more collaborative.

Perhaps the new normal is still being discovered, but the ‘now normal’ is all about flexibility and creativity.

Senior Marketing Executive

Senior Marketing Executive Sales & Marketing

Sales & Marketing